Incyte Falls on Study Failure, Dermatology Pipeline Sparks Hope

Incyte Falls on Study Failure, Dermatology Pipeline Sparks Hope

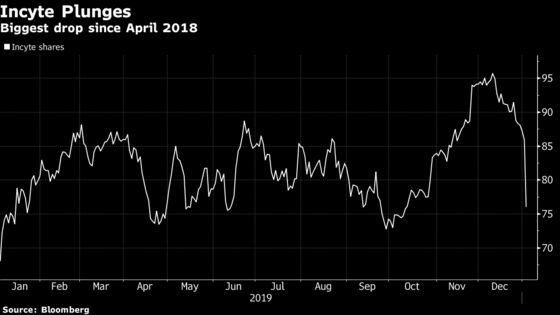

(Bloomberg) -- Incyte Corp. tumbled 12% Friday, the most since April 2018, after the biopharmaceutical company’s itacitinib failed a Phase 3 study for treatment of acute graft-versus-host disease.

Most analysts took a relatively upbeat view of the development, arguing that Incyte has a robust pipeline of other treatments, particularly in dermatology. Incyte’s management also expressed hope that itacitinib could work for the chronic version of the disease.

However, SVB Leerink took a dimmer view of the results, saying they’re part of a series of “high-profile pipeline disappointments” over the past four years that could lead investors to question Incyte’s R&D investments.

Here’s what analysts are saying:

Cantor Fitzgerald, Alethia Young

Young cut Incyte’s price target to a Street low of $65 from $75 and lowered her probability of overall success of itacitinib for chronic GVHD to 25% from 75%.

“With 301 failure, there is no near-term commercial opportunity for itacitinib,” resulting in a $10 cut to Young’s discounted cash flow (DCF) per share. If itacitinib were removed from Incyte’s pipeline entirely, it would lower DCF by another $3 per share, she said.

However, “the benefit of current INCY pipeline is that there is not one big product that is thesis changing per se, but many.” Young maintained her neutral rating.

Cowen, Marc Frahm

Cowen wasn’t modeling any itacitinib sales and is “skeptical of its future in other GvHD settings.” However, Frahm reiterates his outperform rating on the strength of Incyte’s dermatology pipeline.

Incyte management “remains hopeful for a positive outcome for itacitinib in the chronic setting,” but Frahm believes there is little scientific rationale for this.

Ultimately, the opportunity in GvHD is “relatively modest compared with its emerging pipeline programs in dermatology.” Frahm doesn’t have a price target but his sum-of-the-parts analysis is worth $80 per share prior to any contribution from Incyte’s dermatology pipeline.

JMP Securities, Reni Benjamin

JMP has removed itacitinib for both acute and chronic GvHD from its model and cut its price target to $99 from $110.

“Despite our belief that itacitinib will likely not be commercialized, we continue to recommend shares of Incyte since ruxolitinib remains well positioned to generate $1.66 billion in U.S. sales in 2019.”

Benjamin expects the stock to fall about 10% and would be a buyer on weakness based on upcoming value-creating milestones and Incyte’s pro-forma cash position of $2.1 billion. Maintains market outperform rating.

SVB Leerink, Andrew Berens

“The failure of Gravitas-301, which follows three prior high-profile pipeline disappointments in four years, may lead some investors to question the company’s ability to consistently generate value from R&D investment.”

Incyte’s pipeline has had several wins like pemigatinib and the reformulation of Jakafi for dermatology, but “we do not believe either of these programs offsets the fundamental or sentimental disappointments from the pipeline,” Berens said.

Berens removed itacitinib from his valuation and cut his price target to $85 from $90. Maintains market perform rating.

Bloomberg Intelligence, Michael Shah

The trial failure curbs intacitinib’s sales potential but “may have limited readthrough for its trial in the chronic setting, in our view, given they’re believed to be very different diseases.”

Incyte still has several near-term catalysts, but “the pressure is on its R&D efforts to deliver” with a looming 2028 patent expiration for Jakafi.

To contact the reporter on this story: Kristine Owram in New York at kowram@bloomberg.net

To contact the editors responsible for this story: Brad Olesen at bolesen3@bloomberg.net, Steven Fromm, Richard Richtmyer

©2020 Bloomberg L.P.