In Tax-Heavy Westchester, Homebuyers Shift to Condos, Co-Ops

In Tax-Heavy Westchester, Homebuyers Shift to Condos, Co-Ops

(Bloomberg) -- Homebuyers in New York’s Westchester found a less-costly way to live in the county where residents pay the highest property taxes in the country: They scooped up apartments.

In the fourth quarter, sales of co-ops climbed 16 percent from a year earlier and condo transactions rose 8 percent, according to a report Thursday by appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate. Purchases of single-family homes in the tony suburbs, meanwhile, fell for a sixth straight quarter.

Sky-high property levies, and federal tax law changes that reduced homeowners’ ability to write them off, have been scaring buyers away from large homes in Westchester, traditionally a refuge for families seeking more space and relief from Manhattan’s high costs. Suburban buyers now are seeking city-style living at attractive price points, with less upkeep and lower property-tax burdens, said Scott Elwell, Douglas Elliman’s senior executive regional manager for Westchester and New England.

“People want to live a little closer to town, a little closer to the train station,” Elwell said by phone. “We’ve seen a movement toward doing less work. They want a product that’s done, and I think that type of buyer sees value and benefits from condos and co-ops where it’s a very easy ownership structure.”

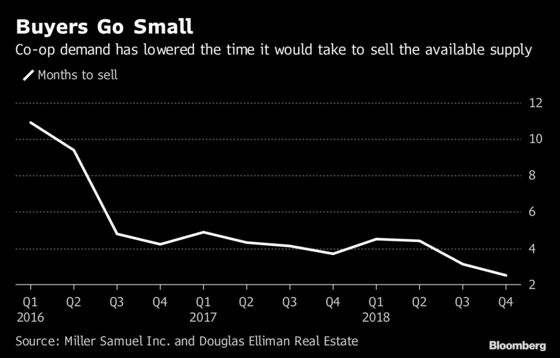

Demand for co-ops was so strong that it would take just 2.5 months to sell all the available units at the current pace of deals. That’s down from 3.7 months a year earlier and 76 percent faster than the average over 24 years of record-keeping, said Jonathan Miller, chief executive officer of Miller Samuel.

The jump in sales of apartments, generally smaller and cheaper than houses and the land they sit on, pushed the median price for all Westchester home sales in the quarter down 1.1 percent from a year earlier to $470,000. The median for the 520 co-op units that changed hands in the quarter was $166,000. For the 310 condo sales, it was $384,000.

Tax Hit

Single-family homes were a harder sell. That’s at least partly thanks to the federal tax overhaul that limits write-offs for mortgage interest and caps deductions for state and local taxes at $10,000 -- well below Westchester’s average property-tax bill of $17,179 in 2017.

Closed purchases of single-family homes dropped 0.8 percent from a year earlier, according to the report. Contracts fell for a ninth quarter and inventory climbed. The median single-family price was unchanged at $600,000.

The tax changes “probably put a little bit of a damper on that market,” said Steven James, CEO of Douglas Elliman’s New York City division. “By the second quarter, when people start paying their taxes and really see what the outcome of the change in the tax law is, I think you’ll continue seeing a decline in sales.”

The last three months of 2018 were especially tough for those looking to sell luxury homes. Just 49 properties priced at $2 million or more were purchased in the quarter, down from 73 a year earlier, according to a report by Houlihan Lawrence.

Bargaining Power

Today’s buyers have superior bargaining power and an eye for value, according to Chris Meyers, president of the brokerage. Sellers -- especially downsizing baby-boomers with dreams of making money on a deal -- will have to reduce their expectations if they want to reach a younger generation with different lifestyle preferences, he said.

“The big question is at what prices are they going to be able to sell those homes, given that there’s a smaller pool of millennial buyers,” Meyers said. “We tend to see sellers are always slower to make adjustments down in prices when market sentiment shifts.”

To contact the reporter on this story: Sydney Maki in New York at smaki8@bloomberg.net

To contact the editors responsible for this story: Debarati Roy at droy5@bloomberg.net, Christine Maurus, Daniel Taub

©2019 Bloomberg L.P.