In a Sated Oil Market, Saudi Arabia Attack Sinks Without Trace

In a Sated Oil Market, Saudi Arabia Attack Sinks Without Trace

(Bloomberg) -- It was the nightmare scenario dreaded by oil markets for decades: a direct strike right at the heart of Saudi Arabia’s energy production network. But when it finally came last month, crude traders almost immediately lost interest.

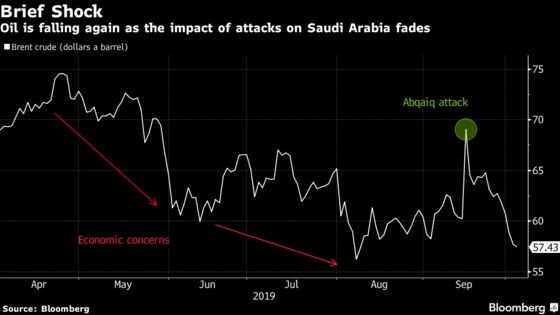

Although oil prices surged the most on record after a barrage of missiles and drones blasted the Abqaiq processing facility and Khurais oilfield on Sept. 14 -- instantly disabling half of Saudi output -- the gains have since evaporated. Crude is back below $60 a barrel, partly because Saudi Aramco has restored production so swiftly, but also reflecting deeper challenges afflicting the market.

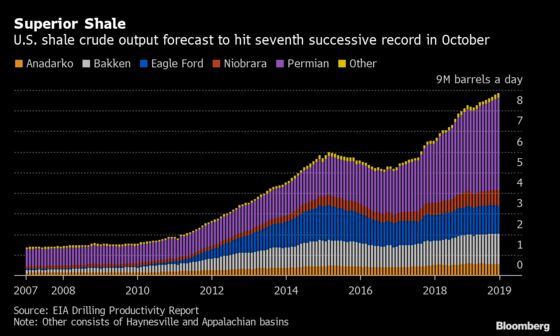

With a faltering global economy and fears of recession eroding oil demand, combined with a relentless tide of American shale-oil offering alternative supply, the kind of shock that would once have sent prices rocketing has barely left a ripple.

“The psychology has changed,” Daniel Yergin, vice chairman of consultants IHS Markit Ltd. and historian of the oil industry, said at a conference in Moscow. “People said ‘Oh my gosh, the price went up so much.’ And my reaction was the price didn’t go up that much, given what had just happened.”

The bombardment turned vital crude-stabilization towers into charred ruins and suddenly halted 5.7 million barrels a day of capacity, equivalent to 5% of global supply. Houthi rebels in Yemen claimed responsibility, though the U.S. government blamed Iran, which backs the group. Tehran denied any involvement.

In the first few frenzied minutes after markets reopened on Sept. 16, Brent crude soared as much as $11.73, or almost 20%, to $71.95 a barrel.

That rally promptly subsided as Saudi Aramco announced it was repairing facilities faster than many had anticipated, resuming full output levels of 9.9 million barrels a day on Sept. 25. Brent is now about 4% lower than before the attack at $57.36 a barrel as of 12:54 p.m. in London. West Texas Intermediate crude has also erased its gains, trading at $52.37.

Industry figures gathered for a conference in Moscow this week largely agreed the market had weathered the disruption. Russian Energy Minister Alexander Novak said there was no “crisis,” and Gazprom Neft Chief Executive Officer Alexander Dyukov said the impact has been limited.

Market Psychology

An ever-darker economic picture helps explain the price response. This week has seen increasingly clear warning signs about the danger of recession as the trade dispute between Washington and Beijing takes its toll on an already-fragile growth outlook. A measure of U.S. manufacturing hit a 10-year low, while the specter of deflation resurfaced in South Korea.

Meanwhile, although the U.S. shale-oil boom has slowed somewhat, the nation’s production remains at near-record levels of more than 12 million barrels a day.

“The growth of U.S. shale has reconfigured not only the global market, but the global psychology, and that was a factor in the relatively calm reaction” to the Saudi crisis, Yergin said. “The other change is the psychology about the global economy. That is affecting the market.”

The market’s indifference is nonetheless striking. A decade ago, mere rumors of disruptions in less significant producers could send prices soaring.

In the wake of the attack, traders predicted that the sudden realization of the vulnerability of Saudi Arabia’s facilities -- once presumed to be securely protected -- would renew the “geopolitical risk premium” in prices, which has faded in recent years.

Instead, the longer-term oil contracts that would reflect such a premium have weakened. Prices of Brent futures from next month through to early 2023 have all fallen since the eve of the Abqaiq assault.

Complacent Investors

Traders and investors are assuming there won’t be further violence, or that Riyadh could again quickly repair any new damage, said Helima Croft, chief commodities strategist at RBC Capital Markets. They may be in for a shock, she said.

“Many market participants believe that Sept. 14 marks the peak of Iran’s disruptive capabilities, and Saudi Arabia’s ability to bring back the barrels so quickly means that any further outages will be very transitory,” Croft said. “I do not share this complacency. We will likely see further escalations before we get an off-ramp.”

For now, though, the investment community remains apathetic. Over the past two weeks, hedge funds and other speculators have pared bets on rising prices by about 5%, data from the ICE Futures Europe exchange shows.

Forecasts from the International Energy Agency, which advises major economies, suggests they may have reason to be cautious. Even if the Saudis hadn’t been able to restore output lost in the attack, there still wouldn’t have been a supply deficit in the first half of 2020, based on the agency’s projections of demand and supply estimates by Bloomberg.

“Any concerns that there were about supply tightening have evaporated,” said Carsten Fritsch, an analyst at Commerzbank AG in Frankfurt. “Looking ahead to the coming year, there is more risk of another oversupply.”

As a result, when Saudi Energy Minister Prince Abdulaziz bin Salman meets with fellow members of the OPEC cartel in December, the minister will face a surprising dilemma: after recovering production from its biggest disruption ever, does the kingdom need to shut some of it down again?

--With assistance from Annmarie Hordern.

To contact the reporters on this story: Grant Smith in London at gsmith52@bloomberg.net;Olga Tanas in Moscow at otanas@bloomberg.net;Dina Khrennikova in Moscow at dkhrennikova@bloomberg.net

To contact the editors responsible for this story: James Herron at jherron9@bloomberg.net, Christopher Sell

©2019 Bloomberg L.P.