In 2020, 2% Looks Like the New 3% for the World’s Benchmark Rate

In the year ahead, 2% is the number to watch for the world’s benchmark borrowing rate.

(Bloomberg) -- In the year ahead, 2% is the number to watch for the world’s benchmark borrowing rate, as the past 12 months have crushed investors’ expectations for how high yields can go.

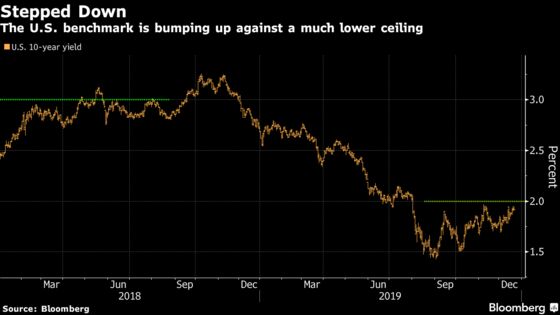

This time last year, the Street’s projections centered on the U.S. 10-year Treasury yield rising about half a percentage point to close out 2019 at around 3.29%. Barring anything extraordinary over this year’s final six business days, that guess will be an overshoot of more than 130 basis points. The Fed’s startling dovish turn early this year quickly settled the debate over whether the benchmark could get back above 3%. As traders head into 2020, the question is, is there life above 2%?

Not many investors seem to think so. Two major potential catalysts for higher yields are already behind us: A decisive U.K. election result this month that will clear the way for Brexit, and an apparent agreement on “phase one” of a U.S.-China trade deal. Even with all that, the 10-year is still stuck just above 1.9%.

“Global growth is elusive,” said Alexandra Wilson-Elizondo, a portfolio manager at MacKay Shields. “It’s not like it’s going to take off just because you have somewhat of a phase-one resolution”

Looking ahead, even if the global economy is on the mend, the likelihood of the Fed keeping rates steady next year is tethering yields on short-dated Treasuries. And those at the long end are capped so long as investors searching the globe for positive-yielding assets are willing to pounce on any cheapening in U.S. government debt.

That’s been the pattern in recent weeks. Since August, yields haven’t got higher than last month’s peak of 1.97%.

The counterpoint is that investors are finally contemplating one of the biggest risks to the bond market’s remarkable bull run. Inflation expectations have stirred off their lows: Ten-year breakevens -- which reflect the market’s outlook for consumer-price inflation over the next decade -- touched 1.8% Friday, the highest level since July.

The renewed interest in inflation risks has picked up in line with improved manufacturing data outside the U.S. and continued resilience in domestic consumption. And it’s steepened the yield curve over the past few months. In August, angst over the global economy herded buyers into longer maturities, pushing their yields below the two-year rate. That inversion has been a reliable signal of recession within the following couple of years.

Now the two- to 10-year curve is trading around 29 basis points, having touched its steepest point since October 2018 last week. Friday’s data showed the Fed’s preferred measure of price pressures rising to 1.5%. That’s the highest since April, though it’s still a long way from the other crucial 2% threshold: the central bank’s inflation target.

“You have seen the steepening in the Treasury curve, which I think is trying to reflect some pickup in inflation expectations,” said Wilson-Elizondo. “But coming into the new year this is the 11th year of the expansion, there’s a lot of risk out there.”

What to Watch

- Bond traders can look forward to an early 2 p.m. New York time close on the 24th, and shuttered markets on the 25th

- Among the visions of sugarplums, there’s a smattering of data:

- Dec. 23: Durable/capital goods orders; Chicago Fed activity index; new home sales

- Dec. 24: Richmond Fed manufacturing index

- Dec. 26: MBA mortgage applications; initial jobless claims; Bloomberg consumer comfort

- The Fedspeak calendar is empty until the new year

- But the Treasury’s prepared a spread:

- Dec. 23: $42 billion of 3-month bills; $36 billion of 6-month bills; $40 billion of 2-year notes

- Dec. 24: $41 billion of 5-year notes

- Dec. 26: 4-, 8-week bills; $32 billion of 7-year notes

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Mark Tannenbaum, Nick Baker

©2019 Bloomberg L.P.