(Bloomberg Opinion) -- Hyundai Mobis Co.’s latest plan brings to mind one image: a damp squib. Again.

The South Korean chaebol’s auto-parts unit released an outline Tuesday evening to “maximize” shareholder value. It’ll do anything but that.

The company also formally proposed family heir Euisun Chung as CEO of the unit, which has been under fire by Paul Singer’s Elliott Management Corp. So Chung had to put something on the table to appease investors. After all, he did promise increased engagement months ago, after moving closer to succeeding his father. The stock has plummeted almost 20 percent since April, when the activist investment fund started rattling at its door. It rose as much as 4.2 percent Wednesday. In response, Elliott on Wednesday urged shareholders to vote on its own set of shareholder resolutions.

Let’s take a look at Mobis’s latest plan, which addresses some of the issues Elliott raised in its initial “Accelerate Hyundai” proposal. To build “firm trust with shareholders,” the company said it will return 2.6 trillion won ($2.33 billion) over the course of three years. Of this, 1.1 trillion won will come in the form of dividends; 1 trillion from a share buyback; and another 500 billion from the cancellation of treasury shares.

The plan boosts the buyback amount from 188 billion won a year. Those shares won’t be canceled but used for various other things (it’s unclear precisely what). The treasury-share cancellation amount, meanwhile, is the same as previously announced. Basically, the unit is returning 1.1 trillion won of cash dividends over three years, which doesn't equate to much more than it hands out right now – 380 billion won annually. All in all, the returns are incremental at best.

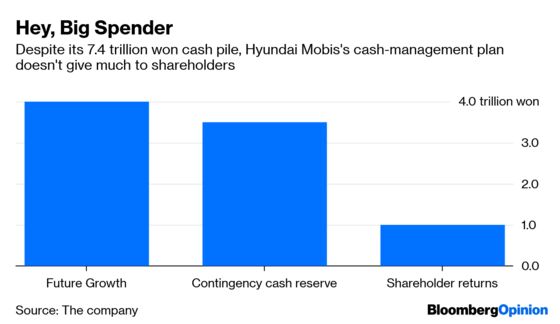

That still leaves a stash of cash on the table: The company had net cash of 7.4 trillion won at the end of 2018. Over the next three years, it plans to hold a “contingency cash reserve” of 3.5 trillion won and spend 4 trillion won on futuristic growth plans including 200 billion to 400 billion won of equity investments in new tech startups (read: 5G, sensors, biometrics, hydrogen fuel cell, etc.) and 3 trillion to 4 trillion won of M&A.

The capex plans are aggressive, too, especially in the auto industry’s current cost environment, as we’ve written. Mobis spent around 2.5 trillion won over the last three years, meaning the company is now planning to shell out almost 60 percent more to expand operations.

Then there’s the board structure. The company said it plans to appoint two new independent directors. Granted, both nominees bring international experience to the table: Karl-Thomas Neumann in autos and car parts, and Brian D. Jones in finance. But the remaining seven are all Korean with limited diversity in experience, and four are already company executives. The board’s ratio of independent directors, and its size, is below global peers’.

Elliott's resolutions, meanwhile, include a dividend of 2.5 trillion won for the common voting shares; expanding the board size; establishing compensation and governance committees at Mobis; and naming two other independent-director nominees with expertise in the global auto industry.

It also said that while its efforts to engage with the company hadn't produced "an acceptable, mutually supported path forward on all the relevant issues," it was pleased that the latest plan had "a number of small but incrementally positive proposals." Elliott concluded that the steps were in the right direction, but didn't "go far enough."

If the younger Chung really wants to show he’s heralding a new era, it’s worth making a bolder statement. Even if Mobis's latest resolutions get passed in March, investors shouldn't get too excited. Meeting shareholders like Elliott in the middle will be key to showing change is actually afoot. But what matters most is delivering on the group’s larger and more difficult restructuring. So far, it’s looking like more of the same.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.