Human-Run Hedge Funds Trounce Quants in Covid Year

Market tumult upended some of the best-known quant behemoths.

(Bloomberg) -- Turns out, the hedge fund industry’s swashbucklers haven’t been made obsolete by the machines just yet.

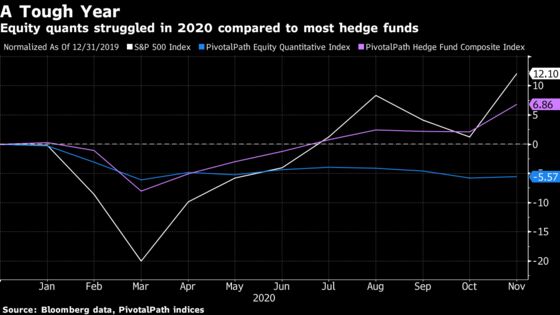

After years of being outgunned and outclassed by computer-driven quantitative strategies, human stock-pickers climbed back on top in 2020, helped by aggressive bets in technology and the flood of central bank money that buoyed markets. The dizzying gyrations of the pandemic-stricken year humbled even the most sophisticated of quants -- notably behemoths Renaissance Technologies and Two Sigma -- whose trading models were thrown off by swings their computers had never seen before.

Overall, human-run funds put up some their best numbers in a decade, with several boldfaced names, including Tiger, Coatue and D1, posting returns in excess of 35%. Whether by luck or by skill, they showed that in this most unusual of years, stock-pickers could still stand up to the seemingly inexorable rise of the machines.

“Stock-pickers had several years of self-inflicted under-performance in the past decade, and the narrative was that computers had defeated humans,” said John Thaler, a longtime equity manager who returned client money in 2015 and this year started a new firm, Hampton Road Capital Management. “Then, the quants hit an air pocket of tough relative performance and this year, long-short equity managers outperformed by an enormous amount.”

| Hedge Fund Winners | 2020 Performance* | Strategy |

|---|---|---|

| Saba ** | 74% | Credit |

| Pershing Square ** | 66% | Long-short equity |

| Whale Rock ** | 64% | Long-short equity |

| High-Flyer China Equity Fund | 60% | Quant |

| Coatue ** | 58% | Long-short equity |

| D1 Capital | 54% | Long-short equity |

| SQN Investors | 46% | Long-short equity |

| Hampton Road ** | 42% | Long-short equity |

| Tiger Global | 39% | Long-short equity |

| UBS O’Connor ** | 37% | Multistrategy |

| Caxton | 36% | Macro |

| Balyasny Atlas Enhanced | 30% | Multistrategy |

| Viking Global Equities ** | 25% | Long-short equity |

| Brevan Howard | 24% | Macro |

| Kepos | 23% | Quant |

* Through November

** Through mid-December

Sources: Fund performance according to documents and people familiar with the matter

Read more: Balyasny Posts 30% 2020 Gain as Some Big Hedge Funds Thrive

Big Winners

Many of the top-performing stock-pickers were helped by their investments in tech and private startups, allowing them to easily double the S&P 500 Total Return Index’s 14% gain through November. They included Coatue Management, Tiger Global Management and D1 Capital Partners, whose bets soared along with the Nasdaq and a sizzling market for initial public offerings.

At the same time, macro managers, many of whom have complained about years of low volatility, finally got what they wanted. The fallout from the Covid-19 pandemic triggered the biggest fluctuations in over a decade as the global economy ground to a halt and unleashed an unprecedented amount of monetary support from the world’s central banks. Andrew Law’s Caxton Associates, for example, took advantage and jumped 36% through November. Brevan Howard Asset Management’s main hedge fund was up 24% through November, on course to match or exceed its best annual return.

That same turbulence was the undoing of a whole host of quant funds, which were among the year’s biggest losers. Their computer models rely on finding patterns in historical data, and many had never encountered a once-in-a-century pandemic.

Renaissance, which oversees $60 billion and was founded by former codebreaker Jim Simons, said in a September letter to clients that its losses were due to being under-hedged during March’s collapse and then over-hedged in the rebound from April through June. That happened because its trading models “overcompensated” for the original trouble.

“This year should call into question some quant strategies,” said Andrew Beer, founder of Dynamic Beta. “Building strategies based on five decades of numbers that don’t matter today might well be a fool’s errand.”

| Hedge Fund Losers | 2020 Performance* | Strategy |

|---|---|---|

| Renaissance Institutional Diversified Alpha ** | -32% | Quant |

| Renaissance Institutional Diversified Global Equities ** | -31% | Quant |

| Odey European | -28% | Long-short equity |

| AQR Global Stock Selection | -22% | Quant |

| Renaissance Institutional Equities ** | -20% | Quant |

| Winton Fund *** | -20% | Quant |

| Bridgewater Pure Alpha II | -17% | Macro |

| Systematica Macro Relative Value | -16% | Quant |

| Two Sigma Absolute Return | -5% | Quant |

* Through November

** Through Dec. 18

*** Through October

Yet even before Covid-19 struck, quant funds were already starting to struggle under the weight of their own success. Several had amassed tens of billions of dollars in assets, meaning market inefficiencies detected by their high-speed computers tended to vanish before they could make much money from them.

“What’s gone under the radar is that most quant strategies haven’t made much money in several years,” said Jon Caplis, head of research firm PivotalPath. They make up 55% of funds that have posted losses since 2016, he said. “These strategies were supposed to revolutionize trading but they didn’t do that.”

There were exceptions of course. China was a rare bright spot for quant strategies in 2020. Unlike many of their counterparts in the U.S. and Europe, China’s top-performing quants returned between 20% and 30% above their equity benchmarks, according to Qiu Huiming, founder of Shanghai Minghong Investment Management Co., the country’s largest data-driven manager.

The flagship fund of the $7.6 billion High-Flyer Capital Management, for example, returned 60% through November, triple the benchmark index.

Qiu noted that because Chinese quants are smaller and operate in a less efficient, retail-dominated market, they have “much greater room for alpha.”

Missing Out

Some low-tech stock pickers also lost big after missing out on the meteoric rise that followed March’s swoon. London-based Odey Asset Management’s European fund declined almost 30%. Lansdowne Partners’ flagship hedge fund shuttered this year, after a 23% drop in the first half.

And this year, the difference between winners and losers has rarely been so stark. Since 2009, the range of hedge fund returns had been fairly narrow and the average result mediocre. In 2020, however, PivotalPath’s measure of fund dispersion -- a gauge of performance variability -- hit a record.

“We had every possible volatility scenario over the last five years: high vol, low vol, dislocated markets,” said Jay Raffaldini, global head of distribution for UBS O’Connor. Whatever the strategy, if a firm missed the opportunity to make money, it begs the question, “How viable is your business model?”

Launches

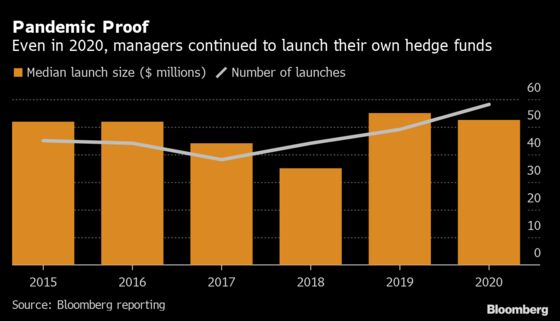

The topsy-turvy year may have even sparked the enthusiasm of traders looking to make a name for themselves.

While pitch meetings went virtual, due diligence became trickier and in-person gut checks were an impossibility, new hedge funds were launched at a surprisingly robust pace. Fifty-eight managers opened firms in 2020, the most in the past six years, with a median of about $55 million raised, according to one industry prime broker. A few traders coming out of the largest and most successful firms even exceeded the billion-dollar mark.

Three of the biggest launches were by stock-pickers.

The largest was Alua Capital Management, co-founded by Viking Global alumnus Tom Purcell and Marco Tablada, formerly of Lone Pine Capital. They started in November with almost $2 billion. Gaurav Kapadia’s XN debuted in July with more than $1 billion in commitments. Ben Jacobs’s Anomaly Capital Management started with $600 million in late October and is expected to amass an additional $1 billion by mid-2021.

Executives at some of the industry’s most influential firms are also looking forward to 2021. Point72 Asset Management’s global macro chief, Mohammed Grimeh, said recently that things will normalize by summer. He’s been beefing up his team in anticipation of several trading opportunities and weighing potential bets in emerging markets, currencies and commodities.

©2021 Bloomberg L.P.