HSBC’s U.K. Unit Could Be Helping Fuel Mortgage Market Price War

HSBC’s U.K. Unit Could Be Helping Fuel Mortgage Market Price War

(Bloomberg) -- Want the lowdown on European markets? In your inbox before the open, every day. Sign up here.

Rules put in place to save U.K. taxpayers from bailing out major lenders again are having an unintended side effect. They’re encouraging HSBC Holdings Plc to wade into a market it long neglected: British mortgages.

Trading updates in recent weeks from Nationwide Building Society, Royal Bank of Scotland Group Plc and Metro Bank Plc said competition to lend to British home buyers was intensifying, even with Brexit looming. HSBC has been wooing first-time home buyers in London with loans up to 95 percent of the value of the property, leading other banks to follow suit.

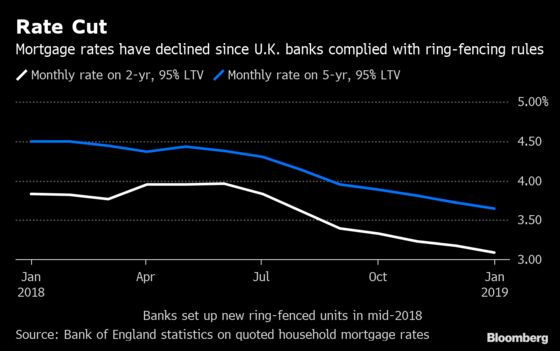

The seeds of this price war appear to have been sown by rules that came into force at the start of the year requiring banks with deposits of more than 25 billion pounds ($32 billion) to hive off their retail banking arms into legally separate companies. This “ring-fencing”, which seeks to protect retail deposits from risky investment banking, has sealed away capital in units where mortgages are one of the few avenues for growth.

HSBC Blamed

Since its creation in July, HSBC’s ring-fenced arm, HSBC UK Bank Plc, has pushed into the home lending market with the help of 12 billion pounds of capital injected by its parent company.

HSBC’s latest results Tuesday showed an $11 billion increase in U.K. mortgages in 2018, increasing its market share from 6.1 percent to 6.6 percent. The bank said that its new ring-fenced structure meant boosting its share of home loans was now one of its “key objectives.”

"We continue to think we have capacity to take share," said Ewen Stevenson, chief financial officer of HSBC, speaking to analysts on results day.

That’s a change for HSBC, which has been a marginal player in British home lending relative to its size. It ranked sixth by market share in mortgages in 2017, according to the industry body UK Finance. At the end of that year, the total value of HSBC’s outstanding U.K. mortgages was 82 billion pounds, less than a third of Lloyds Banking Group Plc’s loan book.

Challengers Challenged

In a trading update last month, Craig Donaldson, chief executive of Metro Bank, blamed “locked-in liquidity” at “HSBC and other banks” for softening mortgage margins. Lloyds, meanwhile, has responded to the pressure by offering mortgages that don’t require any deposit from borrowers.

“You now have this situation where these large ring-fenced banks have very significant capital resources and very cheap liquidity and only one place they can operate: the U.K,” said Paul Lynam, chief executive officer of Secure Trust Bank Plc, a Solihull-based smaller lender. “Previously the likes of HSBC would have allocated capital and liquidity to get the best marginal returns, but now they can’t do that, so all that funding has to be put to use in the domestic market."

Too Much Money

Some investors in the big banks fear they are moving further into the mortgage market because tightening U.K. regulations have shut them out of other lines of business. Complex derivatives and loans to other financial institutions are among the services that banks can no longer support with money deposited by retail customers.

“There is far too much money chasing a non-growing market, which is what you are seeing in mortgages,” said Steve Davies, a portfolio manager at Jupiter Asset Management in London, whose fund owns shares in most of the U.K.’s large banks.

“HSBC has continued its commitment to supporting the housing market by making our mortgages available to customers through their channel of choice, underpinning the process with excellent service and pricing and lending responsibly,” the bank said in an emailed statement.

To contact the reporters on this story: Harry Wilson in London at hwilson57@bloomberg.net;Silla Brush in London at sbrush@bloomberg.net

To contact the editors responsible for this story: Ambereen Choudhury at achoudhury@bloomberg.net, Marion Dakers, Keith Campbell

©2019 Bloomberg L.P.