Hedge Funds Agree With Mom and Pop on a Midterm Trade

Hedge Funds Agree With Mom and Pop on a Midterm Trade

(Bloomberg Opinion) -- It looks as if individual investors have little appetite for risk ahead of U.S. midterm elections. It turns out hedge funds and other large speculators might be thinking the same way.

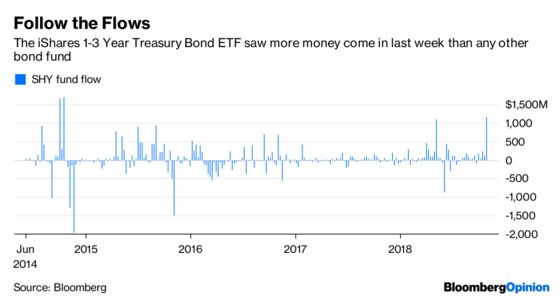

Short-term U.S. Treasury exchange-traded funds experienced by far the biggest inflows among fixed-income ETFs over the past week. The iShares 1-3 Year Treasury Bond ETF alone took in more than $1.1 billion, the most since 2014 and more than 20 percent of the aggregate flow across 380 funds. Two portfolios tracking U.S. bills drew the next largest sums, followed by the iShares 3-7 Year Treasury Bond ETF, which experienced the steepest gain since early 2016. This is a significant trend in and of itself, particularly considering that last week was hardly a risk-off market — the S&P 500 Index staged its largest weekly advance since March.

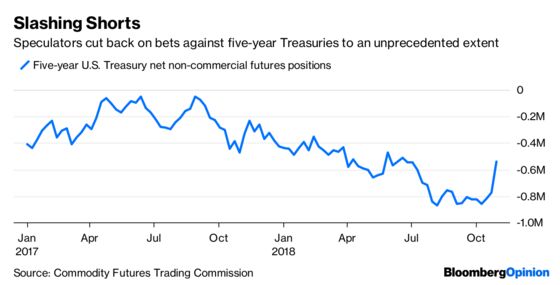

What makes it all the more notable is that big speculators, who are pretty much the exact opposite of individual investors, are taking a similar stance. They aggressively covered the short positions they’ve held for months in five-year Treasury futures, adding an unprecedented 235,388 contracts, according to data from the Commodity Futures Trading Commission that goes back to 1993. The group cut back its wager against longer-term Treasuries, too.

The U.S. midterms could provide any number of market reactions, particularly if the results differ from what’s viewed as the most likely outcome: Democrats take control of the House while Republicans keep a majority in the Senate. For that reason alone, the shift into havens makes sense. But on top of that, memories of the 2016 presidential election still linger. On that Tuesday evening, as results started coming in showing that Donald Trump was ahead in swing states, Treasuries led a global bond rally. By the end of Wednesday, the benchmark 10-year yield was up more than 20 basis points in a rapid reversal of sentiment.

Of course, with elections come the articles about how traders and strategists will be at their desks, burning the midnight oil, ready to respond at a moment’s notice. I like what Greg Staples, co-head of Americas fixed income at DWS Group, told Bloomberg News: “That first reaction at 2 a.m. tends to be the wrong reaction.” Investors might be better off getting some rest and waiting until morning before placing their bets. Or, at least, hopping on the short-term Treasury bandwagon and largely avoiding any market volatility.

George Goncalves at Nomura Securities observed that short-term Treasury funds tend to experience inflows before elections anyway, but what makes this time different is that U.S. fixed-income funds as a whole lost money, making the defensive stance even more striking. Those inflows will reverse if Republicans retain control of both chambers, he predicts, whereas the positions will prove profitable in the case of a Democratic sweep, which could thrust the federal government into gridlock and slow down the Federal Reserve’s interest-rate increases.

No one is really even sure what to expect come Wednesday morning. Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets, has even gone so far as to suggest that the consensus expectation might not be priced into the market because investors aren’t convinced they can trust polling data anymore. That means even if poll aggregator FiveThirtyEight’s forecasts are spot on, stocks and bonds could still experience wild swings as traders sort it all out.

I don’t know that I’d call speculators or mom-and-pop investors the “smart money” in the market. But given all the uncertainty, maybe they’re onto something by casting their ballots before the polls close, but leaving any big wagers for after the votes are tallied.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2018 Bloomberg L.P.