A Junk Bond’s Divergence in Two Markets Shows Climate of Fear

A Junk Bond’s Divergence in Two Markets Shows Climate of Fear

(Bloomberg) -- As fear about the fallout from the coronavirus raced through the corporate junk-bond market this week, debt issued by U.S. Steel Corp. tumbled 7% on speculation the company could be stung if the economy grinds to a halt.

Back in the municipal-securities market, where the steelmaker has also sold bonds, there was no such alarm: tax-exempt debt that the company borrowed through a local agency in Pennsylvania rose 1.2%.

The trading illustrates the broader disconnect that was on display in America’s fixed-income markets as stocks tumbled on speculation that the spreading epidemic could drag the world economy into the steepest slowdown since the credit crisis over a decade ago. On Friday, economists from Goldman Sachs Group Inc. predicted it will trigger a brief economic contraction.

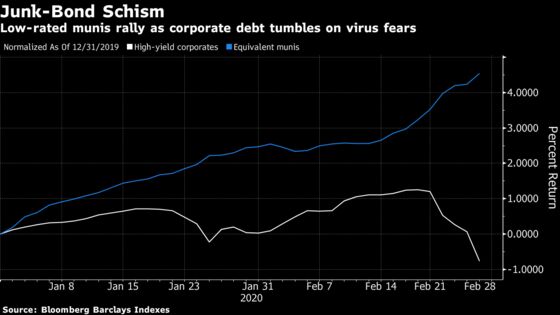

Such worries prompted a major retreat from debt sold by companies most at risk if growth falters. But the flood into havens was so strong that even the riskiest municipal bonds joined in the rally as investors poured about $2.3 billion into state and local government debt mutual funds in the week through Wednesday, leaving managers flush with money they needed to spend.

“Maybe high yield corporates will come back, or eventually the muni market will figure out if we do head into a recession you need to be concerned about high-yield credit,” said Lyle Fitterer, co-head of municipal investments at Baird Advisors. “As long as flows stay positive, guys aren’t going to sell, bonds won’t trade and the price isn’t going to move.”

The high-yield municipal bond market returned about 1% this week, driving yields to the lowest since at least the mid-1990s, according to the Bloomberg Barclays index. By contrast, corporate junk bonds had their worst week since late 2018 with a loss of nearly 2%.

The virus outbreak has the potential to become a pandemic and is at a decisive stage, the head of the World Health Organization said Thursday. With efforts to contain it prompting major shutdowns, bank economists have started estimating that global growth will slow sharply or lapse into a recession.

The dire predictions rattled investors, who pulled $4.2 billion from U.S. high yield corporate-bonds funds during the week ended Wednesday in the biggest pullout since 2018, according to Refinitiv Lipper. Energy and travel companies were the hardest hit. In contrast, investors poured almost $600 million into high-yield municipal funds.

Strong Demand

The strong demand for high-yield municipal securities was reflected in Ohio’s $5.4 billion refinancing this week of debt backed by the state’s share of the 1998 national settlement with cigarette companies. The securities were heavily in demand, with an unrated portion of the bonds maturing in 2055 surging as much as 6% after the sale.

On Friday, U.S. Steel corporate bonds rated B by S&P Global Ratings Inc. and maturing in 2026 traded at 81 cents on the dollar to yield 10.6%, down from 87.25 cents at the end of last week. Tax-exempt muni bonds issued by the the Allegheny County Industrial Development Authority on behalf of the steelmaker maturing in 2030 traded at 120 cents on the dollar Wednesday to yield 2.84%, or 4.7% on a tax-equivalent basis.

“Fundamentally they shouldn’t trade that far apart,” said Fitterer. “There shouldn’t be that much disparity between prices on the two or yields on the two.”

U.S. Steel’s muni bonds trade infrequently, so when bonds come on the secondary market there’s plenty of demand, said Dan Solender, head of municipal debt at Lord, Abbett & Co., which owned U.S. Steel muni bonds as of October.

“In the muni market there just aren’t that many opportunities,” said Solender. “It’s a good diversifier and the supply demand imbalance keep it trading better.”

“Money flows in and out of that market much more rapidly than it does out of our market,” he said. “There’s an issue on our side of the market, too, that if you sell it today you might never be able to buy it back. Sometimes you just have to deal with the volatility if you want to own the credit because just might not be able to accumulate the position again.”

To contact the reporter on this story: Martin Z. Braun in New York at mbraun6@bloomberg.net

To contact the editors responsible for this story: Elizabeth Campbell at ecampbell14@bloomberg.net, William Selway, Michael B. Marois

©2020 Bloomberg L.P.