Hong Kong Will Relax Mortgage Rules to Help First-Time Home Buyers

Hong Kong Will Relax Mortgage Rules to Help First-Time Home Buyers

(Bloomberg) -- Hong Kong’s embattled chief executive Carrie Lam announced plans to help first-time home buyers break into the world’s least-affordable property market, as she seeks to quell protests fueled in part by the city’s rising inequality.

The government plans to allow purchasers to borrow up to 90% of a property’s value to a maximum of HK$8 million ($1 million), from HK$4 million previously. That means first-time home buyers will be able to buy more expensive homes with a down payment of just 10%.

Hong Kong has been rocked by months of often violent demonstrations. What started as concern about a bill to extradite suspects to mainland China has morphed into a general outcry against China’s increasing influence over the city. Some view growing inequality -- most starkly seen in stratospheric housing prices -- as the main cause of discontent.

The unrest “has more to do with the fundamental quality of life, or perceived opportunity for the youth,” Goodwin Gaw, chairman of Hong Kong-based private equity firm Gaw Capital, said in a Bloomberg Television interview Wednesday.

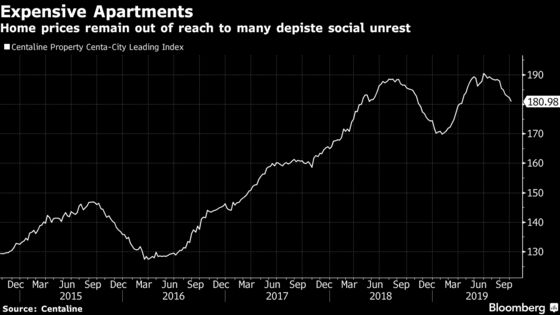

Median property prices in the city climbed to 20.9 times median household income in 2018, according to Demographia, an urban planning consulting firm. That compares with 12.6 times for Vancouver and 11.7 times for Sydney -- two other centers often cited as among the world’s costliest.

The city’s income inequality, as expressed in Gini coefficient, was the most for any developed economy in 2016 at a 45-year high. About one in five Hong Kong residents live below the poverty line.

Patrick Wong, a property analyst at Bloomberg Intelligence, said the change to the mortgage-limit ceiling may support home demand and the mass residential market. But not too many buyers will be able to benefit.

Under the new measures, to buy an HK$8 million apartment borrowing 90% via a 30-year mortgage would require a monthly salary of HK$57,838, according to mortgage broker mReferral Corporation (HK) Ltd. Hong Kong’s median monthly income is just HK$17,500, government data show.

Colonial-Era Law

The cap for those wanting to borrow 80% of a home’s value, meanwhile, will also be increased, to HK$10 million from HK$6 million, Lam said. The rules only apply to those covered by the Mortgage Insurance Programme, a government-backed plan designed to assist first-time home buyers. The Hong Kong Monetary Authority said in a statement that its mortgage rules haven’t changed.

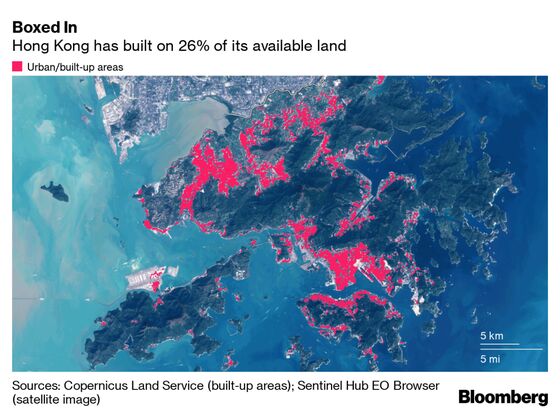

On the home-supply front, Lam said the government would invoke a colonial-era law for the compulsory purchase of 700 hectares of private land -- about twice the size of New York’s Central Park. Some 400 hectares of that will be used for additional housing in the New Territories, Lam said. By way of comparison, only 20 hectares of land has been acquired by the government over the past five years.

Much of it would presumably be purchased from Hong Kong’s biggest developers or private land owners. Henderson Land Development Co., Sun Hung Kai Proprieties Ltd., New World Development Co. and CK Asset Holdings Ltd. hold around 1,000 hectares of agricultural land in the New Territories.

The Hang Seng Property Index extended gains in the afternoon session Wednesday, rallying as much as 2.2%. New World jumped 5.2%, while Sun Hung Kai gained 3.1%.

“Developers are rallying, but shares aren’t going to the highs they reached when Lam announced the withdrawal of the extradition bill. That shows traders are still conservative,” said Steven Leung, executive director at Uob Kay Hian (Hong Kong) Ltd. “The mortgage-rule relaxation may help home buyers a little, but it’s not a big help. It’s the super high home prices that are hurting buyers.”

Hong Kong’s Land Resumption Ordinance dates from the 19th century. It allows the government to purchase land if authorities decide that’s what’s “required for a public purpose.” The law has been seldom used to avoid infringing on private property rights. But if evoked, it could be a boon for developers. They may benefit from the construction of residential projects for public housing, plus the addition of transport and public facilities by the government would help boost the value of land they own nearby.

Home-Price Support

Kenny Wen, a strategist at Everbright Sun Hung Kai Co., said the land purchase plan should “help revise up the value of the farmland held by developers, boosting their balance sheets.” The relaxation of mortgage rules is “an upside surprise,” he added.

“It’ll help boost home transactions, especially in the second-hand housing market,” Wen said. “That would support home prices in an economic downturn.”

There are published rates for purchasing farmland to use for public housing, and some developers’ current land banks have limited commercial value anyway, according to a Sept. 12 research note from Goldman Sachs Group Inc. Faster urbanization could be a positive for home builders, analysts Justin Kwok and Colin Yao said.

Some market watchers are more circumspect.

Ryan Ip, a researcher at think tank Our Hong Kong Foundation Ltd., said the government’s land resumption targets looked “quite aggressive,” particularly considering its previous acquisition speed.

Other housing measures outlined by Lam include:

- Increasing the supply of transitional housing for those waiting for public housing

- Speeding up the sale of units to eligible public-housing tenants

- Allowing higher development intensity for privately owned land under the Land Sharing Pilot Scheme, with the condition that at least 70% of the additional gross floor area is allocated for public or subsidized housing

--With assistance from Jeanny Yu.

To contact the reporter on this story: Shawna Kwan in Hong Kong at wkwan35@bloomberg.net

To contact the editors responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net, Peter Vercoe

©2019 Bloomberg L.P.