Wells Fargo Wants a Bigger Down Payment on That House in Greenwich

Down payment for homebuyers in Connecticut’s Fairfield County raised to 25% from 20% after being categorizing as distressed.

(Bloomberg) -- Wells Fargo & Co. raised its required down payment for homebuyers in Connecticut’s Fairfield County to 25 percent from the standard 20 percent after it categorized the area as distressed.

The new standard, applying to loans above $601,450, would affect a healthy share of buyers in the county, where the median home price in some towns easily tops $1 million.

Wells Fargo, the biggest U.S. mortgage lender, has singled out Fairfield for the added cushion, which is effective for loans made after Sept. 15, mortgage and real estate brokers in the area say. The bank hasn’t changed the down-payment requirements for any other Connecticut county, nor any other county in the New York City metropolitan area, a spokesman for the lender confirmed.

The new underwriting rules “threw all of us off” because they came suddenly and without further explanation, said Jennifer Leahy, a sales broker at Douglas Elliman Real Estate in Fairfield County, which includes the tony suburbs of Greenwich and Darien. “The brokerage community was not pleased because that really affects deals.”

The bank gives a numeric risk rating to each county where it issues mortgages, and Fairfield is rated Class 3, indicating distress, according to a person with knowledge of the matter. A Wells Fargo spokesman, Tom Goyda, confirmed the classification but declined to elaborate on it or to define what it means.

“While we can’t share specifically why we elected to change the market classification for Fairfield County, we review a wide range of local housing and economic indicators as part of our assessment process,” Goyda said in an email.

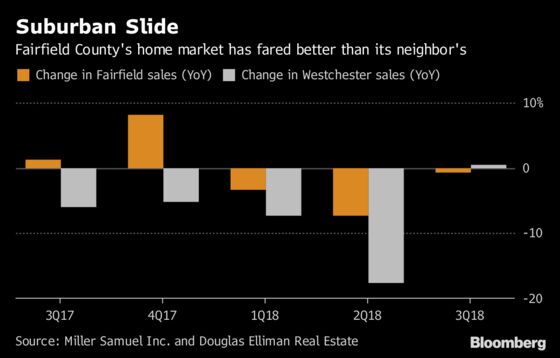

The county’s homebuying market has fared well compared with other New York suburbs. While sales in the third quarter slipped 0.7 percent -- the third consecutive decline -- the median price of homes that changed hands climbed 3.7 percent to $425,000, according to a report by Douglas Elliman and appraiser Miller Samuel Inc. Contracts, a more timely measure of demand, jumped 28 percent. Sales in Greenwich, home to many Wall Street executives, surged 26 percent, the best summer for that market since 2012.

In neighboring Westchester County, single-family home sales declined for a fifth straight quarter, and prices there fell, too. Purchases in Manhattan, Brooklyn, northwest Queens and Long Island also decreased in the third quarter, according to the firms.

State’s Woes

“There’s no rhyme or reason for underwriting standards to be different in Fairfield,” said Jonathan Miller, president of Miller Samuel. “The only thing I can think of is they’re worried about what’s happening in Hartford more than what’s happening at the specific property level.”

The U.S. recovery has largely bypassed Connecticut, where the economy has contracted in every year but one since the recession. The state added just 14,700 private-sector jobs since 2008, and the government, based in Hartford, is facing a $4.5 billion deficit in the next two-year budget cycle.

Fairfield County, thanks to its proximity to New York, has Connecticut’s highest housing costs, and the average mortgage there is $415,289 -- almost double that of other counties in the state, according to Attom Data Solutions. About 18 percent of this year’s purchase loans for condos or single-family homes were above Wells Fargo’s $601,450 jumbo threshold.

Government mortgage buyers Fannie Mae and Freddie Mac don’t purchase jumbo loans, which are riskier for lenders because they typically hold them on their books until maturity.

Wells Fargo “holds these loans in portfolio, it doesn’t sell them off, so they’re making darn sure that those loans don’t go bad down the road,” said Guy Cecala, publisher of Inside Mortgage Finance. “It’s far from arbitrary that they did this. Let’s face it -- hardly any lender would want to blacklist Greenwich.”

The new standards took one of Leahy’s clients by surprise -- a couple who were under contract to buy a home in Darien for $760,000 and had been preapproved for a Wells Fargo mortgage before rates started rising in September. Suddenly, they had to scramble to come up with an extra 5 percent for the down payment, which would allow them to keep the rate they had locked in, or start a new loan application with another lender at a higher interest rate.

They came up with the cash, but not everyone can, Leahy said. “This affects real buyers.”

To contact the reporter on this story: Oshrat Carmiel in New York at ocarmiel1@bloomberg.net

To contact the editors responsible for this story: Rob Urban at robprag@bloomberg.net, Christine Maurus

©2018 Bloomberg L.P.