Holding Pattern May Break as Stocks Buzz the Tower: Taking Stock

Holding Pattern May Break as Stocks Buzz the Tower: Taking Stock

(Bloomberg) -- We’re in a fitting holding pattern, if you will, in the S&P ahead of a slew of airlines earnings this morning that include AAL, LUV, JBLU (a mini hedge fund hotel with 12% ownership). These key economic harbingers also happen to have a window seat to the impacts of the Government shutdown and how that may be affecting the industry. Southwest, for its part, just said that they are seeing negative revenue impacts thus far in January, already estimated at up to $15 million.

This echoes comments from hotels like Marriott, for example, which cited double-digit declines in its business in the D.C. area, according to their global chief commercial officer in an interview with Yahoo finance earlier this week.

Earnings again will be the key driver today of action as headlines concerning trade have died down. It feels as though there may finally be a bit of exhaustion sinking into this rally that brought us superlatives like the “fastest start since 1987” -- and that may be just fine as the broad based buying can shift to more stock specific factors.

There wasn’t any real reason to buy the tape yesterday knowing that a major catalyst in the twin Senate votes to reopen the Government was due today, and as a result, the only real positive action was in the big earnings reports. Outside of those, there were two buckets of cold water (the Richmond Fed data, which came in in-line while citing "soft" manufacturing activity in January; and White House Council of Economic Advisers Chairman Kevin Hassett saying that if the partial government shutdown extends through March, there’s a chance of zero economic expansion this quarter).

The caution in the market is palpable, as Wednesday felt more defensive than it looked on the face of it. For most of the day, had you stripped IBM’s performance from the S5INFT, the sector in the aggregate would have been one of the worst performers, along with materials and energy. You also had the defensive-focused utility index up on the day (all 27 members) and consumer staples leading the market (razor and household product maker PG’s results didn’t hurt there).

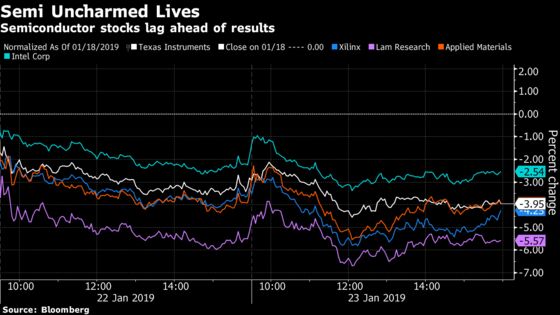

Popped Chips

But the big news will likely be semiconductor (chips). A flood of earnings last night are poised to set the tone for some of electronics demand going forward -- and if you were to casually look at the tape, you’d see a variety of positive signals. Xilinx up 10%, Lam Research +7% (while its peer Applied Materials rose 4% in sympathy) and Texas Instruments (the biggest barometer with a diverse client base) up another percent.

But had you owned those stocks coming in to this week, you’d be struggling to be just even. The macro story has just weighed too powerfully on the space for the individual companies to overcome.

Even taking the largest positive outlier, Xilinx, which beat the highest estimate and is up more than 10 percent in early trading, one would be sitting on slightly more than a 5% gain from Friday’s close (Morgan Stanley’s Joseph Moore wrote that company is "defying gravity" with exceptional growth while outshining its peers).

Lam Research’s positive result has an investor flat from Friday. Korean semiconductor powerhouse SK Hynix’s operating profit, which was reported shortly thereafter, missed analyst estimates. We’ve written that the semiconductor industry is among the most exposed to China and the trade war, and that the Philadelphia semiconductor index has fallen nearly 20 percent from its March record. Intel Corp. has a chance to right to ship with its results due post market Thursday.

But if there is any consolation in the space, its that there may signs of a bottom forming. Stifel analysts write that Lam Research’s 2019 outlook for wafer fab equipment (WFE) spending was below what they believed to be a bottom and risks are geared more now toward the upside for its future outlook.

Another sign the end isn’t nigh came when iPhone supplier STMicro earlier Thursday forecast a return to growth. The company discussed weakness in their outlook for 1Q, but ultimately saw a return in growth in 2Q and the rest of the year. Many analysts were expecting the weak smartphone outlook to hamper results.

Sectors in Focus Today

- Airlines day with LUV already in the books with a beat, but citing some impacts from the Government shutdown. AAL still to come

- Restaurant names ahead of Starbucks results post market and the consolidation speculation that surfaced Wednesday that suggested QSR may be interested in Papa John’s. The results follow the coffee shop’s investor day last month

- Defense contractors like Honeywell, Hexcel and General Dynamics after UTX’s results led to its best day in 10 years Wednesday. Textron’s results just hit the tape and appear mixed with beats on the bottom line and a miss on revenue

- Industrial rental supply firms HEES, HRI and Ashtead after United Rentals results beat

- Casinos (like WYNN, CZR) (in Macau and otherwise) after Las Vegas Sands missed expectations

- Industrial distributors MSM, HDS and WCC as we await WW Grainger results

- Lighting stocks Acuity Brands, Hubbell, SemiLEDs, Veeco after German peer Osram Licht issued caution over its results seen in December

Notes From the Sell Side

Piper analyst Michael S. Lavery is out removing his buy rating on Post Holdings, citing eroding retail sales trends at its Active Nutrition and Refrigerated Foods segments, which had formed the basis for the original bullishness. Sees risks that the declining sales in the active nutrition unit could impact its planned IPO and affect the cash proceeds. Lavery still sees the prospects for deal activity to provide a catalyst, but goes to neutral from overweight.

Network security name Palo Alto Networks is indicated higher after Wedbush analyst Dan Ives boosts his rating to outperform with a PT of $265 (from $225). He cites "incremental confidence" in the growth story over the next 12-18 months after prior worries for the stock appear to be in the rear view mirror. Numbers on the Street appear "conservative," as Ives expects the firewall refresh will be a major tailwind for the company.

Tick-by-Tick Guide to Today’s Actionable Events

Senate will vote on two measures to reopen the Government. TBA

- 7:30am -- AAL earnings

- 7:45am -- ECB rate decision

- 8:00am -- UNP, FCX earnings

- 8:00am -- Morgan Stanley CEO James Gorman on Bloomberg TV

- 8:30am -- Commerce Sec. Wilbur Ross on CNBC

- 8:30am -- Weekly Initial Jobless Claims

- 8:30am -- AAL earnings call

- 8:45am -- UNP earnings call

- 9:15am -- Goldman Sachs CEO David Solomon on Bloomberg TV

- 9:45am -- Jan. US Markit PMI

- 10:00am -- JBLU, FCX earnings call

- 10:30am -- BMY earnings call

- 10:30am -- EIA natgas storage change

- 11:00am -- Jan. Kansas City Fed manufacturing

- 11:00am -- EIA weekly U.S. oil inventory report

- 12:30pm -- LUV earnings call

- 2:00pm -- SLG earnings call

- 4:00pm -- INTC, NSC, SBUX earnings (roughly)

- 4:30pm -- NSC earnings call

- 5:00pm -- INTC earnings call

- 5:00pm -- SBUX earnings call

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.