(Bloomberg Opinion) -- Hitachi Ltd. is turning away from its burdensome atomic business. Investors are right to be relieved.

The Japanese conglomerate finally made a decision to suspend construction of its once-ambitious nuclear power station on the U.K.’s Welsh coast, after months of uncertainty. It expects to take an impairment charge of 300 billion yen ($2.7 billion) in the year ending March 2019.

It isn’t clear whether Hitachi will fully exit the Wylfa project or just leave it offline. Getting rid of it is probably the best way forward, much as Toshiba Corp. found in the case of Westinghouse Electric Co., the bankrupt U.S. nuclear unit that was sold last year. There are no obvious ways to fix Hitachi’s U.K. nuclear business without sinking in more cash, which would mean taking on more debt and risk. As Hitachi attempts to restructure and modernize, the last thing it needs is this millstone hanging over its operating margin target of 8 percent, as we noted when the company bought ABB Ltd.’s power-grids business last year.

There will be no cash outflow from the impairment charge, but there won’t be any tax benefit either. Selling or liquidating the business would result in a tax-deductible loss, as analysts at Goldman Sachs Group Inc. pointed out. The 300 billion yen estimate reflects the decline in value as of June last year plus another 20 billion yen or so of termination costs; it doesn’t include operating expenses over the past five years.

The impairment charge is more than three times the 90 billion yen that Hitachi paid just over five years ago to buy Horizon Nuclear Power Ltd., the unit that holds the project, from two German power companies. At the time Hitachi justified the purchase by saying it would contribute to the U.K. government’s energy policy and support that of Japan. Despite government backing, it couldn't figure out how to make the project viable.

The struggles of the Wylfa plant demonstrate a broader problem for nuclear energy. While it has the advantage of being emissions-free at a time when the world's grids badly need to decarbonize, on every other front it falls down.

Even the cheapest new nuclear generators in the U.S. would cost three times the price of equivalent solar and wind facilities, according to an analysis by Lazard. Indeed, new wind turbines can deliver energy so cheaply that they're on the verge of undercutting even existing and fully depreciated nuclear plants on price.

Then there’s the issue of time. As the travails of Wylfa and the Vogtle and V.C. Summer generators in the U.S. have demonstrated, building a new nuclear plant takes at least a decade. The plunging costs of renewables mean each year that goes by makes nuclear less and less competitive, compared with other zero-carbon sources.

Having talked about a 10-year horizon for nuclear, Hitachi’s management is cutting its losses early. The purchase looks to have been hasty, especially considering the absence of a financial ring-fence for the project. Two years after the purchase, management started talking about risk and lack of stability. Regardless of what arrangements the U.K. or Japanese governments could have offered, the construction costs were Hitachi’s to bear.

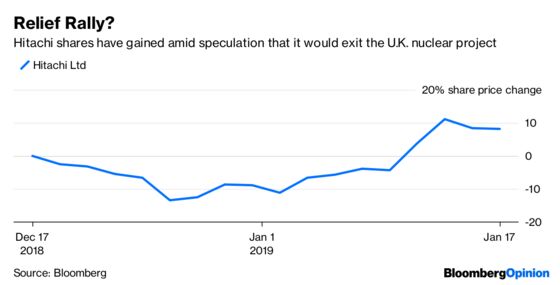

Investors have sent Hitachi stock up 25 percent in Tokyo since Dec. 25, when speculation started that a decision on Wylfa was nearing. It retreated on Friday, though, even as the Japanese market rallied. Hitachi can’t sever its nuclear bonds soon enough.

In the decade or so it would take to build a single 2.9-gigawatt generating plant like Wylfa, a single solar panel manufacturer such as Canadian Solar Inc. could produce modules that would generate 20 times as much electricity. Next to the nimbleness of renewables, nuclear struggles to compete.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.