Historic Oil Rout Breaks Shale, Trump’s Energy Dominance

It’s a swift and brutal end to the shale revolution

(Bloomberg) -- An historic crash in crude prices is driving U.S. shale into full-on retreat with operators halting new drilling and shutting in old wells, moves that could cut output by 20% for the world’s biggest producer of oil and leave thousands of workers unemployed.

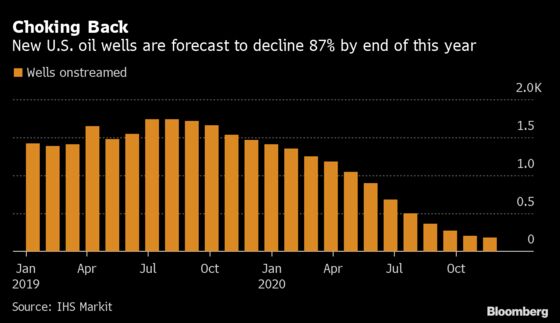

For shale companies, the price of West Texas Intermediate crude went from hunker-down-and-ride-it-out mode to crisis mode in just a few days, with many now unsure whether there will even be a market for their oil. Some 1.75 million barrels a day is at immediate risk of shutting down while the number of new wells being brought online is forecast to plunge almost 90% by the end of the year, according to IHS Markit Ltd.

In short, it’s a swift and brutal end to the shale revolution, which only last year had President Donald Trump proclaiming “American Energy Dominance.”

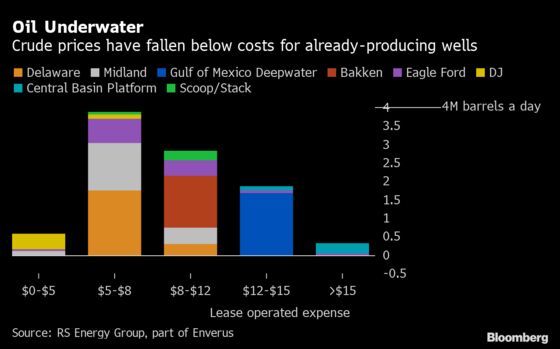

West Texas Intermediate crude prices turned negative for the first time in history on Monday, meaning at one point sellers had to pay buyers to take it away. Then, the financial squeeze on the May contract spilled over to June and into the wider market, with prices now trading around $14 a barrel, well below the daily pumping cost in large swaths of America’s oil industry.

Even at $15, “everything back in the field, except the newest and most productive wells, is losing money on a cash-cost basis,” said Raoul LeBlanc, a Houston-based analyst at IHS Markit. “At this price you’ll start shutting in large amounts of production.”

It’s a bloodbath whichever way you look.

Operators are switching off wells, retiring one in three drill rigs, abandoning fracking, laying off 51,000 workers, slashing salaries and even going bankrupt just six weeks after the latest price plunge began. Now, with the coronavirus pandemic destroying demand, storage is just weeks away from filling up, a further factor choking back output.

Publicly-traded companies have axed more than $31 billion from drilling budgets, while distressed debt in the U.S. energy sector has jumped to $190 billion, up more than $11 billion in less than a week. Oil companies made up five of the top 10 issuers with the most distressed debt as of Tuesday. Evercore ISI reckons 5 million barrels a day, or around 40% of U.S. production, could be temporarily shut in by the end of June to help balance the market.

The potential for next to no revenue in the second and third quarters this year may mean that large U.S. oil explorers burn through $7 billion in cash, according Evercore. By the end of it all, as many as 30% of publicly traded shale explorers could be forced to exit the market one way or another, the Evercore analysts said.

For Gene Ames, an 85-year-old, fourth-generation oilman who was born in the East Texas oil rush during the Great Depression, when crude traded for 5 cents a barrel, it’s the worst crash he’s ever seen. “I’ve been through about six major busts and so far this is going to be the worst,” he said by telephone. “It’s the most intense, quickest and deepest collapse.”

The Saudi-Russia price war, which accelerated the price drop due to Covid-19, “has succeeded in hammering the last nail in the coffin of U.S. shale production and posed a major threat to the national security of the United States,” he said. He’s pushing the Texas Railroad Commission to impose mandatory production cuts. The commission deferred a decision on whether to do so on Tuesday.

Houston Economy

In Houston, America’s oil capital, the pain is set to reverberate across the broader economy.

The industry is far and away the “best paid” in the city, said Patrick Jankowski, an economist at the Greater Houston Partnership. “Someone who works on the blue-collar side can make $100,000 a year, so when those jobs go away it has a disproportionate impact on the economy.”

Now, the region needs to find its next growth engine. “Energy will still be important, but it’s going to be less important than before,” Jankowski said.

There’s little chance of relief any time soon. Oil traders are on a desperate quest to find somewhere -- anywhere, really -- to store their crude as tanks from Texas to Siberia fill to capacity. Virtually all commercial onshore storage in the U.S. has been booked since the end of February, according to people with knowledge of the matter.

It will likely take months to clear the oversupply, with no clear end in sight for the pandemic’s effects.

Unforeseen Period

“We’re all having to anticipate revenues that are significantly cut or just completely cut for an unforeseen period of time,” said Kyle Armstrong, president of Armstrong Energy Inc., a closely held producer on the New Mexico side of the Permian Basin. “Whether it’s negative $37 or $5, to me it doesn’t matter,” he added. “It’s effectively zero because I can’t operate wells productively at those prices.”

The first taps to be turned off will likely be the 1.75 million barrels a day from older, conventional U.S. wells that produce just a few dozen barrels a day each, according to IHS Markit’s LeBlanc. Producers will seek to ride out the storm with more productive wells providing some cash flow, even if made at a loss, in part due to the costs associated with shut-ins.

“The U.S. oil market actually gets worse fundamentally over the next month,” said Paul Sankey, a veteran oil analyst, in a note to clients. Producers have “nowhere to go with the inexorable production that takes weeks and months to reduce to zero.”

But the bigger problem for the shale industry is the lack of new wells being drilled. Shale wells decline by more than 60% in the first year, meaning new ones are needed to replaced production from old ones.

With few new wells coming online, IHS sees U.S. oil production declining to 10.1 million barrels a day by the end of the year, from 12.8 million barrels a day at the start. That will likely drop further to somewhere around 8.5 million barrels a day in 2021 to 2022, according to Noah Barrett, a Denver-based energy analyst at Janus Henderson.

“A good portion of production, particularly areas of the Bakken and Oklahoma, will go away completely,” said Barrett, whose employer manages $356 billion. “Fresh capital will be needed to grow off that lower base. But there’s zero appetite for that in the foreseeable future.”

©2020 Bloomberg L.P.