High-Yield Borrowers Proceed With ‘Extreme Caution’ in Europe

High-Yield Borrowers Proceed With ‘Extreme Caution’ in Europe

(Bloomberg) -- It may be a new year, but high-yield bond issuance in Europe is off to a tentative start as the caution that plagued the market through the end of 2018 continues to linger.

Smurfit Kappa Group Plc became the third borrower this week to launch a tap or coterminous bond sale, which bankers say reflects nervous sentiment around selling bigger sized or longer dated bonds.

“Despite the January rally, the carnage of the fourth quarter last year is fresh in people’s minds, and so an air of extreme caution permeates the European high-yield market market right now,” said Thomas Hanson, a fund manager at Janus Henderson Global Investors, which manages $75 billion of fixed income assets.

The sensitivity is also impacting pricing with certain borrowers needing to pay premiums to access the market. U.K.-based Stonegate Pub Company is expected to pay well over 100 basis points more than its existing notes for a planned 150 million pound ($198 million) bond sale. The notes are currently guided at 625-650 basis points over Euribor with a discount to par, according to people familiar with the matter.

No Rush

Rates-sensitive borrowers who are not in imminent need of new financing may be deterred from raising new debt amid relatively high borrowing costs, which were triggered by a selloff in the latter stages of last year.

“As a higher quality issuer that has no need to issue, then this probably isn’t the right time to undertake an opportunistic refinancing,” Hanson said, adding that a lower-rated name may prefer loan financing rather than being the first to undertake price discovery in the bond market.

Prior to this week, only one high-yield deal had priced in 2019 via Telecom Italia SpA. The Italian carrier paid a hefty premium to get its 1.25 billion euro bond sale over the line, but the offering failed to boost confidence owing to a profit warning just a week after the notes priced.

“The smaller deals or taps that we are seeing may yet develop some positive momentum for our market but the signs so far aren’t great,” Hanson said.

Softly Does It

Signs of caution are not confined to the high-yield market. Leveraged loan borrowers are also treading softly into the start of the year with issuance so far mainly limited to add-on deals, or mid-sized borrowers. The market is still waiting for a large LBO financing to set a benchmark for the primary market.

But some of this month’s loan add-ons have been devoured by hungry investors, hinting at keen appetite for more issuance. This week, Nets A/S was able to upsize its new debt and price tighter than originally talked after more than 40 accounts were said to have piled in.

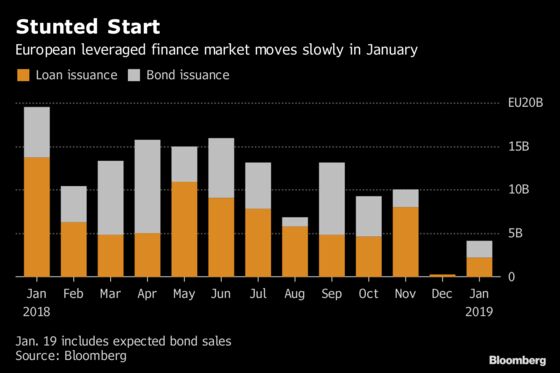

So far, just 1.9 billion of euros of bonds have priced in January, compared to 5.8 billion euros in the same month last year. Leveraged loan volumes amount to 2.3 billion euros this month, versus 13.7 billion euros in January 2018.

To contact the reporters on this story: Laura Benitez in London at lbenitez1@bloomberg.net;Ruth McGavin in London at rmcgavin1@bloomberg.net

To contact the editors responsible for this story: Sarah Husband at shusband@bloomberg.net, Charles Daly

©2019 Bloomberg L.P.