Here’s How KKR Might Just Pull Off the Biggest LBO in History

Here’s How KKR Might Just Pull Off the Biggest LBO in History

(Bloomberg) -- One of the private equity industry’s titans called it a “stretch,” and it’s been dismissed as a pipe dream by a bevy of analysts.

Yet interviews in recent days with debt-market specialists suggest that KKR & Co. could find a narrow path to finance what would be the biggest leveraged buyout in history: a potential take-private deal for pharmacy chain Walgreens Boots Alliance Inc. that analysts have estimated would need to be funded with at least $50 billion of debt.

The challenge for any Walgreens suitor will be raising the necessary money via the markets of choice for private equity firms -- junk-rated loans and bonds -- which have become fragile after an unprecedented borrowing binge left investors with a hangover. Debt funds that financed more than $3.5 trillion of leveraged buyouts in the past decade have become pickier, leaving banks stuck holding more than $2 billion of unsold loans on their balance sheets as recently as last month.

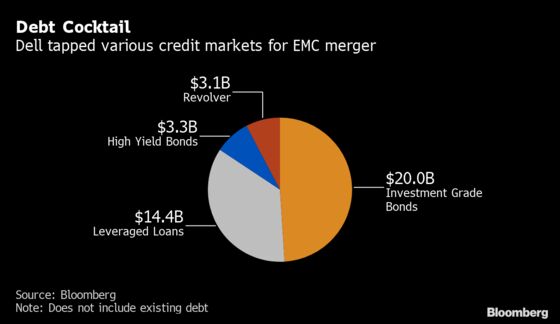

But a road map may be hidden in two other recent debt-fueled takeovers: Dell Technologies Inc.’s $67 billion takeover of EMC Corp. in 2016 and Charter Communications Inc.’s $78.7 billion acquisition of Time Warner Cable Inc. that same year.

Representatives for KKR and Walgreens declined to comment.

Buyout Blueprint

Junk-rated Dell and Charter both borrowed heavily in the investment-grade bond market by issuing secured debt. T-Mobile US Inc. is going down a similar route to help pay for its purchase of Sprint Corp.

In Charter’s case, it pledged security to new and existing bonds issued by higher-rated Time Warner to ensure the debt remained investment-grade. Dell used a similar strategy when it bought investment-grade rated EMC. Walgreens’s debt could be segregated into two borrowing structures at a holding company level and an operating company portion, with investment-grade debt placed on the latter.

In doing so, Dell and Charter won access to the most stable part of the corporate debt market, where investors are still buying heavily as an alternative to low or negative-yielding assets elsewhere. At the same time, they limited their reliance on leveraged finance markets, where sentiment can shift quickly and prove costly.

Both companies did tap those markets, but with more manageable offerings. Bankers who asked not to be identified estimated that Walgreens would be able to raise between $10 billion and $20 billion of junk-rated debt to fund a buyout.

Other market participants, who asked not to be named because they weren’t authorized to speak publicly, said KKR still might need to find a deep-pocketed third-party investor to help put more equity into the deal.

Or it may seek to spin off a portion of Walgreens to lessen its financing needs. The company’s European operations could potentially bring in $18 billion to $20 billion, CreditSights analyst James Goldstein said in a phone interview.

--With assistance from Nabila Ahmed and Robert Langreth.

To contact the reporters on this story: Natalie Harrison in New York at nharrison73@bloomberg.net;Lisa Lee in New York at llee299@bloomberg.net;Davide Scigliuzzo in New York at dscigliuzzo2@bloomberg.net

To contact the editors responsible for this story: Shannon D. Harrington at sharrington6@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.