Hedge Funds Went All In on Short Bonds at the Wrong Time

Hedge Funds Went All In on Short Bonds at Just the Wrong Time

(Bloomberg) -- Hedge funds look to have gotten their timing very wrong, piling into bullish short-term Treasury bets ahead of some of the steepest yield spikes in years.

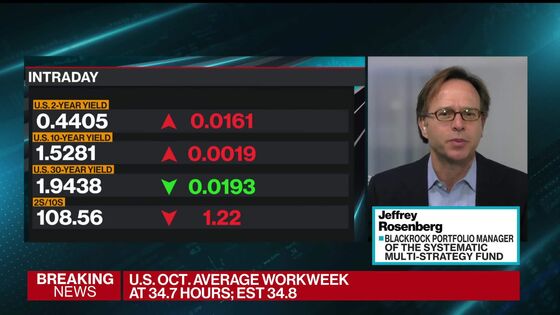

Leveraged funds built up bullish bets on two-year Treasury futures and Eurodollar contracts at the fastest pace on record over the last four weeks, based on a rolling average of the latest data from the Commodity Futures Trading Commission. The net long positions stood near the highest since 2015 last Tuesday and were likely loss-making given that two-year yields surged from 0.27% to as high as 0.56% over that four-week period.

The seemingly mistimed bets came amid convulsions in the bond market as investors brought forward wagers on global rate hikes, only to have central bankers seek to push them back. Yields swung wildly, particularly in the short-end, with several high-profile hedge funds experiencing significant losses or having to restrict trading.

Among the hard hit were Rokos Capital Management, Alphadyne Asset Management and Brevan Howard Asset Management. Rokos and Alphadyne are on track to post their worst annual loss on record, while October was the worst month ever for Brevan’s AS Macro fund.

“The sell-off was very futures driven and likely exacerbated by positioning given that a lot of front end and belly structures that are favored by hedge funds were at attractive levels,” said Su-Lin Ong, head of Australian economic and fixed-income strategy at Royal Bank of Canada. “The speed of the moves was also consistent with that cohort stopping out.”

Of course, the hedge fund wagers could be part of a larger positioning: the so-called basis trade, in which they wager on the difference between futures and the underlying bond. The trade makes sense because the increasing threat of Fed rate hikes in October caused a surge in two-year yields that disrupted the cash-futures relationship.

The bullish shift from hedge funds stood in contrast to their slower-moving institutional counterparts, who had flipped bearish on short-dated Treasuries around the same time. Treasuries fell on Monday following a rally last week, with the yield on two-year notes rising three basis points to 0.43%.

Investors are left reconsidering the timing of their rate-hike wagers and some have been critical of the communication coming from central banks. The positioning data doesn’t cover the aftermath of the Federal Reserve or Bank of England meetings, both of which conveyed a dovish message that stood in contrast to still sizeable bets on sooner-than expected hikes.

©2021 Bloomberg L.P.