Hedge Funds Ponder the Ethics of Shorting Unethical Companies

Hedge Funds Ponder the Ethics of Shorting Unethical Companies

(Bloomberg) -- Albourne Partners Ltd. has been around for a quarter-century and advises institutions who collectively invest more than $500 billion in alternative assets.

So when Albourne this month, for the first time, made it mandatory for the roughly 650 hedge funds one of its teams monitors to answer questions about their approach to environmental, social and governance issues, it highlighted a shift the industry is struggling to cope with but can’t afford to ignore.

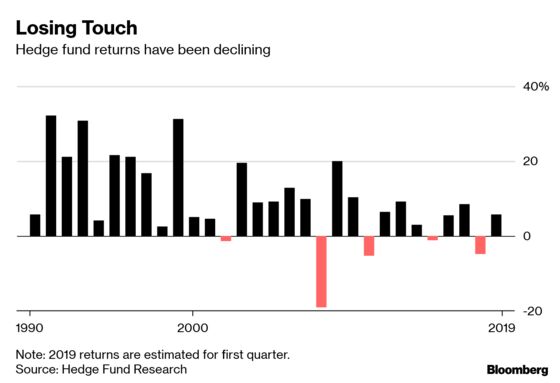

While the change also applies to other types of alternative-asset managers (like buyout firms) under Albourne’s purview, hedge funds by their very nature are somewhat ill equipped to handle the rising emphasis on ESG in investing. Some trade in and out of securities in as little as microseconds, and the ability to make unconstrained investment decisions -- including so-called short bets -- is essential. Taking ESG into account adds a layer of complexity for a $3.1 trillion industry that for years has grappled with sub-par returns.

It’s a simpler equation for long-only investors. Don’t like a company for its poor ESG practices? Don’t buy its shares. But are you allowed to sell short the same company -- and potentially profit -- from those same lax principles if the stock falls?

Whatever the merits of imposing additional ethical constraints on hedge funds, the pressure is building. And it’s coming from the pension and endowment funds that have become increasingly important sources of capital in the decade following the global financial crisis.

“In the last 12 to 18 months, I’ve started to feel we’ve reached a sort of a tipping point of alternative managers really taking ESG seriously," said Edward Mason, the head of responsible investment at Church Commissioners for England, the entity tasked with managing the Church of England’s 8.3 billion pound ($10.9 billion) endowment fund. “If a manager isn’t doing this, they’re in danger of being left behind.”

Church Commissioners for England has what it terms an “exclusion list.” It’s been in place since 1948 and now spans weapons, pornography, tobacco and gambling, along with high-interest rate lending and thermal coal extraction. Just under 10 percent of the endowment fund is allocated to hedge funds, and the Church won’t consider putting money into any fund or strategy that can’t meet its requirements. Its “sin list” applies to both bullish and bearish investments, and even index-related derivatives.

Tobacco, Stem Cell Research

Brad Lindenbaum, the chief investment officer of New York-based hedge fund Stone Forest Capital LLC, has fielded questions from investors touching on weapons, abortion, stem cell research and tobacco-related investments. Stone Forest manages about $175 million across two funds, one of which uses a long-short equities strategy.

Lindenbaum says it is more difficult to invest when there are ESG constraints, but he reckons the challenges are manageable. A bigger issue, at a time of fund outflows and relentless pressure on fees, is the additional costs it imposes.

“The problem is hedge funds tend to be much smaller in scale,” he said. “Because of that, the cost burden to the firm is proportionally higher. If a firm has multiple clients with different exclusion lists, it could add significantly to its legal, administrative costs and operational complexity.”

Steve Kennedy, the partner who leads Albourne’s ESG initiatives, said hedge funds can tackle the issue “from a lot of angles.”

“You can try not to own those companies, or you can only own the ones that are better on ESG factors and short the ones that are less so,” he said. “A great one is also to buy the cheap ones that aren’t as good but are on an improvement path. There’s no one size fits all.”

Albourne still has an optional questionnaire that hedge funds can choose whether to answer. The mandatory part comes when the firm is hired by an endowment or pension fund to conduct due diligence on a fund’s operational risks. This typically happens when a money manager is close to making an initial investment. A hedge fund can answer that it doesn’t have an ESG policy, but that will be reported back to the prospective investor.

Switzerland’s LGT Capital Partners AG is also dialing up the pressure. The almost $60 billion asset manager strongly encourages every hedge fund that wants its money to sign up to its managed-account platform, a sort of portal that allows it to monitor their positions daily.

The Big Short Question

It now has about 40 hedge funds on the platform, according to Managing Partner Werner von Baum. LGT assigns an ESG rating of 1 through 4 for each manager (with 1 being the best) and they’re required to adopt an exclusion list created by stewardship and risk-engagement specialist Sustainalytics, he said.

Where things break down somewhat, according to von Baum, is when it comes to short selling, or betting that a security will lose value.

“It’s fair to say a lot remains to be done,” he said. “There’s not yet a common understanding on how to interpret hedge funds’ short positions in terms of ESG.”

The Church of England is against both long and short bets on industries on its exclusion list because it believes that either way, it’s wrong to profit from those activities, Mason said. But Lindenbaum pointed out that by shorting a stock, you can help increase a company’s cost of capital.

An overly prescriptive approach isn’t necessarily the best way, and hedge funds dread exclusion lists, said Jarkko Matilainen, the former director of hedge funds at Finland’s Varma Mutual Pension Insurance Co. He said ESG isn’t that relevant for short-term investors who trade in and out of positions in hours and weeks. Rather than an outright ban on certain sectors, Matilainen prefers encouraging hedge funds to incorporate ESG risk assessment in evaluating potential investments.

Albourne decided to make answering ESG questions compulsory in its operational due diligence phase after the percentage of its clients considering such factors in allocation decisions doubled to 35 percent between 2016 and 2018. Albourne has been collecting such data since 2012.

“We’d never seen such a sharp increase between the two surveys,” Kennedy said.

To contact the reporter on this story: Bei Hu in Hong Kong at bhu5@bloomberg.net

To contact the editors responsible for this story: Katrina Nicholas at knicholas2@bloomberg.net, Philip Lagerkranser

©2019 Bloomberg L.P.