Hedge Funds Get It Wrong With Ill-Timed Dollar, Bond Bets

Hedge Funds Get It Wrong With Ill-Timed Dollar, Bond Bets

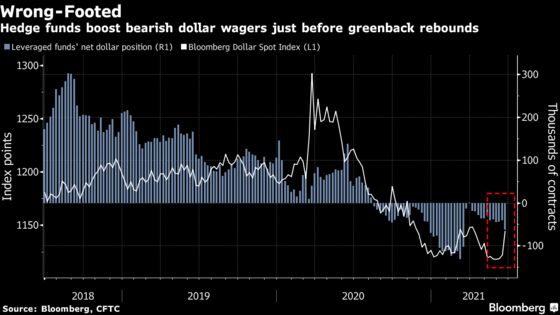

(Bloomberg) -- Hedge funds couldn’t have picked a worse time to be short the dollar while holding Treasury curve steepener positions.

Leveraged funds boosted net dollar shorts by 21,347 contracts in the week ended June 15, the most since mid-January, according to data from the Commodity Futures Trading Commission. A day later, Federal Reserve officials projected a faster-than-expected pace of tightening, propelling the Bloomberg Dollar Spot Index to its biggest weekly gain in over a year.

“Nothing that has happened in the last week, including the Fed’s revised messaging, alters our fundamentally bearish U.S. dollar view,” said Ray Attrill, head of foreign-exchange strategy at National Australia Bank Ltd. in Sydney. “But, we accept that there may still be some positioning pain to unravel and that the technical picture for the U.S. dollar is more constructive given last week’s price action.”

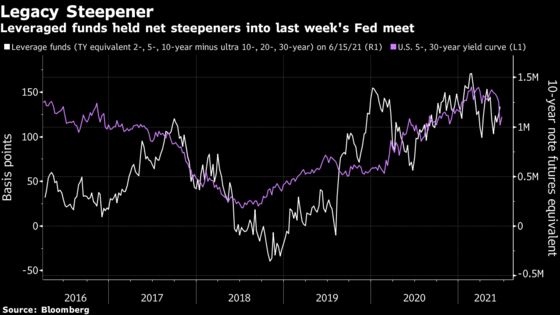

In Treasury bond futures, CFTC data shows leveraged funds held aggregate curve steepener positions ahead of last week’s FOMC meeting. The duration weighted net long positions of contracts below 10-year maturity minus longer ones shows a steepener position equivalent to around 1.2 million of 10-year note contracts, down from a recent peak in February, according to Bloomberg’s calculations.

The spread between the 5- and 30-year yield curve flattened by 26 basis points last week after the Fed decision -- the largest move in a decade -- leaving the gap at the tightest level for the year.

This spread widened again on Monday. In written remarks prepared for his congressional testimony, Fed Chair Jerome Powell said inflation should move back toward the central bank’s 2% target once supply imbalances resolve.

©2021 Bloomberg L.P.