Hedge Funds Are Oddly Silent in Toshiba Buyout Drama

(Bloomberg Opinion) -- Where are the hedge funds when you need them?

Overseas investors bailed out Toshiba Corp. in 2017 by buying $5.4 billion of shares after accounting scandals and troubles with its nuclear business threatened the Japanese company’s survival. Now they’re standing aside as the conglomerate pursues a buyout program that doesn’t seem good for anyone.

Here’s a quick recap: As part of its Toshiba Next Plan, the company said in November that it planned to buy out shareholders in three subsidiaries for $1.8 billion, one of them being chip-equipment maker NuFlare Technology Inc. Tokyo-based Hoya Corp. put in a higher, unsolicited bid for NuFlare, seeking a minimum 66.7% stake. Toshiba Machine Co., which partly owns NuFlare, brushed off the hostile approach and went with the lower bid.

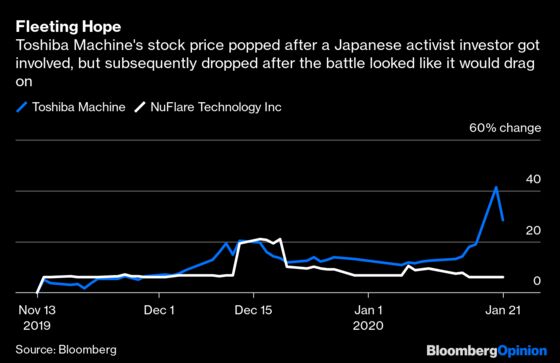

On Tuesday, a fund backed by activist investor Yoshiaki Murakami launched a tender offer for a 44% stake in Toshiba Machine, in an apparent effort to disrupt the consolidation. Toshiba Machine shares had surged as much as 19% Friday after the company said Murakami planned a bid. They fell Tuesday after the offer — a 12% premium to Thursday’s closing price — was lower than some investors expected.

So there you have it: activist hedge funds, buyouts and hostile bids all make for the trappings of change.

Yet shareholders at each of the companies — including the hedge funds that own Toshiba Corp. stock — seem to be the losers and no one is saying anything about it.

First, let’s look at the privatization. In consolidating NuFlare, it isn’t quite clear what the so-called synergies are for Toshiba Corp. besides the unit’s high operating margins and the cash it brings. Toshiba CEO Nobuaki Kurumatani has contended the conglomerate’s decisions are driven by issues of governance, saying the parent is “indispensable” to NuFlare and the unit cannot create value without Toshiba’s engineers and technology. He has also said he isn’t interested in selling the business.

But compare that to what Hoya and NuFlare could have done together. Hoya is a client of NuFlare, buying mask writers that are used for imprinting patterns on glass squares, which act as a stencil for semiconductor designs. The two companies also share customers. If acquired by Hoya, NuFlare would get a “richer R&D budget, greater knowledge about (extreme ultraviolet) EUV processes and wider client relationships than it would in a Toshiba acquisition,” as analysts at CLSA Ltd. note.

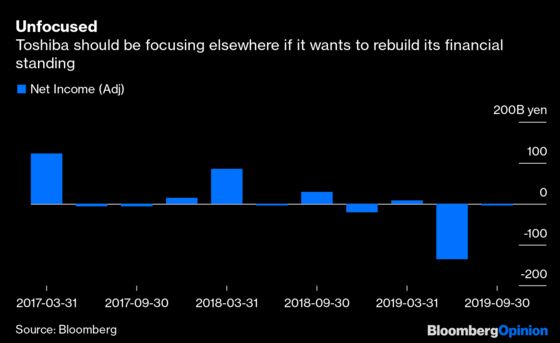

Fully owning all these subsidiaries will no doubt boost earnings for Toshiba Corp., but the parent isn’t in a financial position to plow cash into their businesses. Moody's Investors Service said last month that Toshiba's liquidity is weak and the company will have to get external funding to meet its short-term cash needs. Meanwhile, on Jan 18., Toshiba said it couldn't confirm the existence of “ suspicious transactions” of as much as 20 billion yen ($182 million) of sales at a subsidiary. Clearly, the conglomerate still has other issues requiring its attention.

Rather than investing in these units, Toshiba could focus on growing organically, shedding money-losing assets and finding a sturdier financial footing. That may be of more value to shareholders in the long term. But it’s surprising that hedge fund owners haven’t made much noise about the plan, seemingly content with Toshiba’s share price increase of about 30% since they came on board in the November 2017 fundraising.

Next, consider NuFlare. How did the company decide to go with Toshiba’s not-so-juicy bid versus Hoya? How did it determine that was a fair price? Did minorities get a look in? In rejecting Hoya, there was a clear conflict of interest, SmartKarma’s Travis Lundy says. The NuFlare board, put in place by majority owner Toshiba, was weighing a bid by the parent against a higher offer.

Toshiba Machine, meanwhile, seems all too keen to please Toshiba Corp, despite having heavyweight (albeit passive) investors such as Japan’s government pension fund on its shareholder roster. Its argument that the Murakami offer could hurt shareholders and corporate values is a poor look. The unit’s approach is like a time-slip to 30 years ago, before the introduction of Japan’s corporate governance code, Murakami’s daughter Aya Nomura told the Financial Times.

With their focus on returns, overseas hedge funds might be expected to share that sentiment. It’s time they gave this Japanese activist some more support.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2020 Bloomberg L.P.