Hedge Fund With Three-Decade Winning Streak Bets on U.K. Deals

Hedge Fund With Three-Decade Winning Streak Bets on U.K. Deals

(Bloomberg) --

For Tiedemann Investment Group, whose deals-focused hedge fund has never lost money, the U.K. is proving a hotbed of opportunity.

The New York-based firm has built a 550 million-pound ($761 million) wager on companies engaged in U.K. deals this year, according to Drew Figdor, who runs TIG’s $3.2 billion investment strategy.

“One of the themes running in this market is overbidding and shareholder activism and we see that has created optionality at a very reasonable cost,” Figdor said in an interview. “In the U.K. it’s even better because the risk of deal breaking is substantially less.”

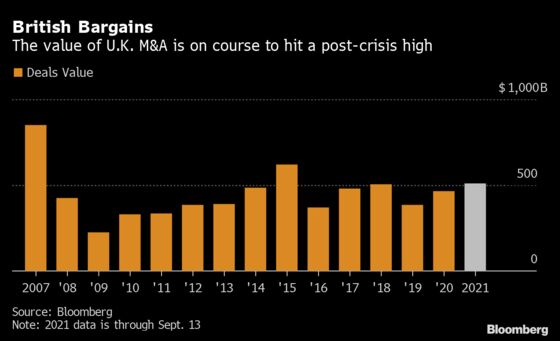

Depressed valuations in the U.K. as the country’s businesses grapple with the effects of Brexit, as well as the global pandemic, have led to the highest level of dealmaking in 14 years. TIG, which seeks to profit by taking so-called merger arbitrage trades, has built bets on merger and acquisition targets such as Wm Morrison Supermarkets Plc, engineering group Meggitt Plc, cyber-security software company Avast Plc and developer John Laing Group Plc, according to regulatory filings.

The trades involve taking positions that capture the spread between a target’s stock and the price of the buyer’s offer. While hedge fund firms reap a profit if the deals complete, they run the risk of a precipitous decline if they fall apart.

Figdor said the U.K.’s regulatory regime and takeover code ensures that companies don’t often walk away from announced deals, making the country a relatively safer bet. Of the roughly 130 deals targeting a listed company that have collapsed this year, less than 5% involved a U.K.-listed name, according to data compiled by Bloomberg. Among those U.K. deals were transactions only scrapped after a higher bid won out, meaning merger arbitrage funds would still have been able to profit.

Buyout firms flush with cash have been particularly active in the U.K. this year, prompting takeover battles that have pushed up company valuations and led to deals valued at $512 billion in the country.

The heated fight for Morrison, for example, will result in an auction to settle whether it will be Fortress Investment Group or Clayton Dubilier & Rice LLC that will acquire the U.K.’s fourth-biggest grocer. The trend makes M&A bets even more attractive to hedge funds.

“We think the opportunity set is underestimated by the market, you are effectively owning that upside optionality for free,” Figdor said. “Of course it doesn’t happen every time but when it does, you are making 5%-20% more.”

His TIG Arbitrage Strategy hasn’t lost money in any year since it started trading in 1993 and has produced an annualized return of just under 7%, according to an investor document seen by Bloomberg. The fund, which bets on corporate events such as tender offers, mergers, liquidations and proxy contests, gained as much as 7.8% during the first six months of the year, trailing an 8.4% rise in the HFRI ED Merger Arbitrage Index.

TIG’s commitment to the U.K. market is in sharp contrast to some of its peers who are cashing out some of their bets on U.K. acquisition targets. Money managers such as J O Hambro Capital Management, Silchester International Investors and Franklin Resources Inc. are among firms that have cut some of their positions.

“We are in a fairly attractive period for dealmaking,” Figdor said. “There’s a need to do deals and there’s an ability to fund those deals at attractively priced debt, which creates an obvious opportunity.”

©2021 Bloomberg L.P.