Hedge Fund With 36% Gain Bets More on U.S. Corporate Debt

Hedge Fund With 36% Gain Bets More on U.S. Corporate Debt

(Bloomberg) -- In a low-yield world, there’s still good returns to be made from corporate debt.

Lower-rated, long-duration U.S. investment-grade bonds may gain as much as 30% if spreads narrow to pre-Covid levels, according to hedge fund manager Alp Ercil, who has made double-digit returns from the strategy this year.

While the extra yield over risk-free rates that investors demand for holding A-rated U.S. corporate debt has shrunk significantly in recent months, the same has yet to happen for long-duration BBB or BBB- rated paper, Ercil, the founder of Asia Research & Capital Management Ltd., told the 2020 Sohn Hong Kong investment conference on Wednesday.

The Covid-19 pandemic triggered a rout across asset markets in March, including indiscriminate dumping of investment-grade debt. Unprecedented stimulus by central banks to shore up their economies has since driven the compression of some spreads, as investors chase yield amid low and negative interest rates.

ARCM deployed about 80% of the $1.6 billion assets in its latest distressed-assets fund between March and April, picking up heavily sold-off, long-duration U.S. investment-grade credit with solid fundamentals. It returned 36% in the first eight months of the year, much of that from those trades, Bloomberg reported earlier this week.

After the March rout, the Federal Reserve pledged to buy $250 billion of U.S. investment-grade and “fallen-angel” credit -- bonds considered investment grade before the selloff -- as well as eligible exchange traded funds. So far, it has spent only $13 billion. Similar measures adopted by the Bank of Japan in 2012 and the European Central Bank in 2016 led to significant tightening of spreads, Ercil said.

The Fed’s commitment to hold rates near zero for years to come also eliminates a cost for foreign investors who hedge U.S. debt holdings with bearish dollar bets, making the trade even more attractive, Ercil said. Investors should still hedge interest rate risk with Treasury futures, he added.

Companies have this year raised a record $1.5 trillion from investment-grade bond sales through August. With no capital expenditure or takeover sprees on the horizon, new issuance should slow, turning investor attention back to existing paper.

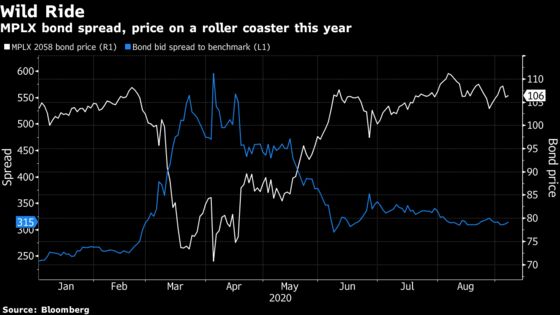

Ercil sees spreads continuing to tighten in the next 12-to-18 months. The firm has constructed a basket of bonds with an average remaining duration of 29 years, including Apache Corp., Energy Transfer LP, Hess Corp., MPLX LP and Plains All American Pipeline LP.

©2020 Bloomberg L.P.