Halliburton Writes the Script for Fracker Earnings

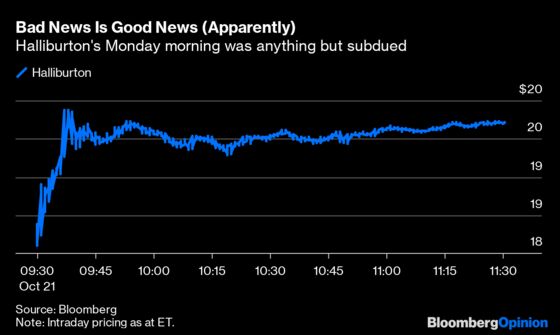

(Bloomberg Opinion) -- Poor Halliburton, kicking off Monday morning with news it missed revenue estimates in the third quarter — especially in its main North America business — and then informing Wall Street’s finest this quarter looks pretty dire, too. No wonder the stock … jumped 8%?

Put that down to two things. First, Halliburton Co. has lately been about as popular in the market as a fracker at an Elizabeth Warren rally. The stock had lagged the broader oilfield services sector so far this year (which is saying something), and short interest was at its highest level in almost four years. Earnings estimates, which Halliburton actually beat slightly, had collapsed already in January and stayed down. So anything short of catastrophe looked like a win. Second, Halliburton largely dispensed with the happy talk on its call. This is the bit to focus on.

It is telling that Halliburton made a point of talking up the prospects for its international business, which generates less than half its revenue. Halliburton typically defines itself by its higher exposure to North America (and thereby the shale boom) vis-a-vis its big rival Schlumberger Ltd. Signing off after questions, though, CEO Jeff Miller declared he was “excited” about the prospects for the international business, while merely expressing confidence that Halliburton’s strategy for dealing with a weaker domestic business was working.

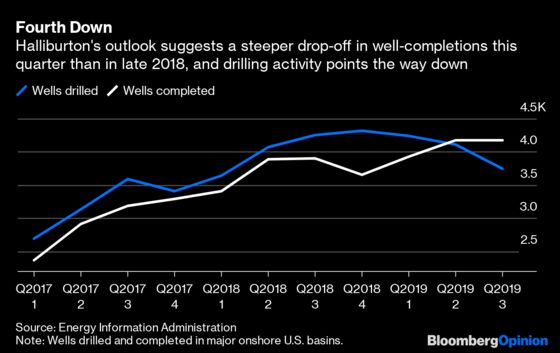

That strategy is (more) cost-cutting and outlasting weaker rivals as the downturn in shale drilling and completion intensifies. There will be no holiday season in frackland if Halliburton’s outlook is anything to go by. While the third quarter is typically the busiest, Halliburton noted stage counts — the sections of a horizontal well that get fracked — had declined each month. The company idled more equipment than it had through the entire first half of the year. The outlook for the fourth quarter: “More of the same.” In particular, the number of completed wells might drop below the level of the fourth quarter of 2018, implying a drop of 13% from the quarter just gone. The number of wells drilled certainly points that way:

This really shouldn’t come as a shock, given what’s been happening with the U.S. rig count and even the prices of hotel rooms in the Permian basin, where, like fracking equipment, spare capacity has piled up. The big question arising from Halliburton’s numbers and grim commentary — similar to Schlumberger’s — is what it portends for the rest of this earnings season as exploration and production companies report numbers.

The mildly hopeful interpretation of the reduced activity weighing on Halliburton is that E&P companies have heeded the call and are diverting more cash flow away from drilling and toward investors. This is what the industry sorely needs in terms of both recovering trust from the financial markets — which look all but closed right now — and moderating the growth in U.S. oil production that is weighing on prices. Halliburton cited its clients’ free cash flow targets as one challenge on Monday’s call.

On the other hand, notwithstanding Halliburton’s hopes for its international business, 2020 could be grim for oil and gas markets due to broader economic pressures, such as the trade war. That makes it even more imperative for frackers to show restraint, both to retain cash flow and rebalance supply with demand.

Every signal, from their cost of capital to the gloom enveloping contractors, is telling E&P companies to cool it. Even the emergence of securitized “shale bonds” just reported by the Wall Street Journal, while nominally a sign of new capital flowing in, is a signal of desperate measures in desperate times. Apart from its usual services, Halliburton has provided its E&P clients with a script. They should follow it.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.