Gulf’s Holdout on Rates Is About to Jump on Fed Easing Bandwagon

Gulf’s Holdout on Rates Is About to Jump on Fed Easing Bandwagon

(Bloomberg) -- Explore what’s moving the global economy in the new season of the Stephanomics podcast. Subscribe via Pocket Cast or iTunes.

The only Gulf Arab central bank with an unpredictable monetary policy might finally fall in line this week.

In a region where most countries usually track the Federal Reserve to protect their currencies’ pegs to the dollar, Kuwait split from the likes of Saudi Arabia and the United Arab Emirates, standing pat when U.S. interest rates were lowered in July and September. But now that the Fed is widely expected to deliver another cut, Kuwait is likely to pull the trigger too, even as inflation accelerates.

As pressure builds on funding costs at Kuwaiti banks and with this year’s economic growth forecast at just above zero, the probability of its first monetary easing since 2012 is “very high,” according to Raghu Mandagolathur, head of research at Kuwait Financial Centre SAK. Unlike its neighbors’ pegs to the dollar, Kuwait controls the value of its dinar against an undisclosed basket of currencies, meaning it has more flexibility in setting rates.

“Maybe they weren’t too worried about growth, and managing liquidity can be a more important objective,” Mandagolathur said by phone. “But the priority will probably shift back to growth now.”

After missing out on two straight rounds of monetary easing, Kuwait’s interbank rate is about 60 to 70 basis points higher than those in Saudi Arabia and the U.A.E.

While the central bank raised its discount rate only once last year by a quarter-percentage point and then kept it steady since March, its repo rate -- the deposit-pricing benchmark -- was lifted by a cumulative 100 basis points in several steps since December 2017.

Exacerbated by deposit withdrawals made by government entities, the result is a higher cost of Kuwaiti banks’ funding, as well as declines to their net interest margin, a measure of loan profitability, according to Bloomberg Intelligence analyst Edmond Christou.

‘Added Pressure’

“This has added pressure to all Kuwaiti banks,” Christou said in a report. “If the central bank cuts the discount rate, but the repo rate remains unchanged, depositors are likely to be the biggest beneficiaries, at the cost of bank margin and shareholder returns.”

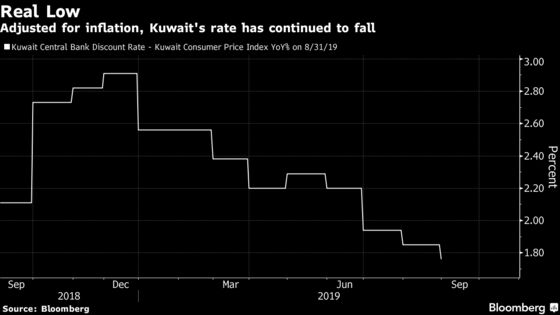

OPEC’s fourth biggest oil producer also broke with most of its neighbors and didn’t move in lockstep with the Fed when it raised borrowing costs nine times since 2015, hiking the discount rate only four times instead. Kuwait’s nominal policy rate has been at 3% -- a level Saudi Arabia never reached during its tightening cycle -- for longer than a year and a half.

But adjusted for inflation, Kuwait’s borrowing costs are actually lower than in Saudi Arabia, which has experienced annual declines in price growth every month this year. By contrast, inflation in Kuwait is at the fastest since November 2017.

An even bigger pickup may lie ahead, with the International Monetary Fund projecting inflation at 2.2% next year, up from 1.5% in 2019 and just 0.6% in 2018, according to its latest outlook.

When the central bank left Kuwait’s discount rate unchanged in September, policy makers said they wanted to “improve the growth-enabling environment” and “ensure the continued attractiveness of the national currency” for savings.

For an economy that contracted in 2017 and may only expand 0.6% this year, more relief could finally be on its way.

Fed officials have said little to take a third straight rate cut off the table when they meet this week. And traders have almost entirely priced in a quarter-percentage point cut at the coming meeting, which would match its moves in July and September. But there’s also uncertainty about what the Fed might do after October.

Kuwait’s interest rate can’t be “way off the mark” from other countries, according to Raghu.

“A lower repo rate would ease cost-of-funding pressure, given liquidity tightening is temporary,” Christou said.

To contact the reporter on this story: Arif Sharif in Dubai at asharif2@bloomberg.net

To contact the editors responsible for this story: Dana El Baltaji at delbaltaji@bloomberg.net, Paul Abelsky, Paul Wallace

©2019 Bloomberg L.P.