Juan Guaido’s Team Signals It May Default on PDVSA Bond Backed by Citgo

Juan Guaido’s Team Signals It May Default on PDVSA Bond Backed by Citgo

(Bloomberg) -- The team advising Venezuelan National Assembly President Juan Guaido signaled Tuesday that it may stop making payments on the nation’s only bond not currently in default.

Advisers to Guaido, recognized by the U.S. and more than 50 countries as Venezuela’s interim president, say a Trump administration executive order Monday protects Venezuelan assets in the U.S., including Citgo Holding. That would prevent holders of Petroleos de Venezuela’s 2020 notes from foreclosing on their collateral -- 50.1% of Citgo Holding shares -- in the event of a default, according to Jose Ignacio Hernandez, Guaido’s attorney general.

While Guaido’s team isn’t seeking to use U.S. sanctions as an excuse to avoid its debt responsibilities, it has more pressing concerns than the $913 million payment on the PDVSA 2020 bond due in late October, according to Hernandez. He said PDVSA’s ad hoc board and the National Assembly will make the final decision.

“Venezuela faces a unique economic crisis and complex humanitarian emergency,” he said in an interview. “It doesn’t make much sense for a country in crisis to make that big of a payment.”

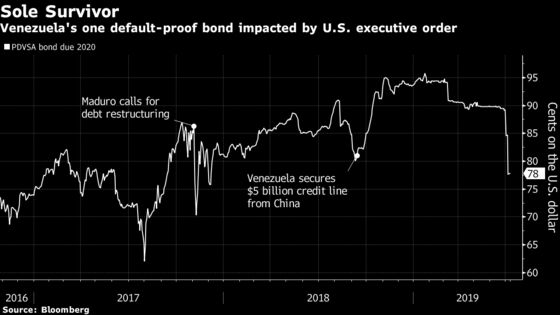

Since Venezuelan President Nicolas Maduro called for a debt restructuring in November 2017, the nation has defaulted on every bond except the PDVSA 2020 notes. That’s because of the strong desire -- both from Maduro’s and Guaido’s advisers -- to prevent Houston-based Citgo from falling under creditor control. But the executive order gave Guaido’s team what it had been privately requesting for months: a mechanism to shield Citgo from lenders and focus on funding humanitarian aid.

“This executive order is a very clear signal that the U.S. administration won’t allow Venezuelan assets in the U.S. to be subject to attachment,” Alejandro Grisanti, a member of the ad hoc PDVSA board set up by Guaido, said in an interview.

Grisanti said that he plans to meet with Guaido’s legal advisers, including debt-restructuring veteran Lee Buchheit, Wednesday in New York to discuss the scope of the new measures from the Trump administration. In a subsequent conversation, he said the ad hoc board wasn’t considering missing the payment: “I never talk about a default.”

Meanwhile, a Venezuela creditor group advised by Cleary Gottlieb Steen & Hamilton and Guggenheim Securities convened its own call Tuesday to discuss the executive order, according to two people familiar with the matter. Several members of the group have contacted the U.S. Treasury Department in the hopes of lobbying for an amendment allowing them to seize the Citgo collateral, the people said.

A spokesman for the Treasury declined to comment, citing department policy.

Even if Guaido’s team chose to make the PDVSA 2020 payment in October, it would need the approval of the U.S. Treasury and Venezuela’s National Assembly. It received the sign-off for a $71 million interest payment in April. Yet there had been a growing contingent in the opposition-led legislature advocating for a default in order to devote more money to humanitarian relief, according to three people familiar with the matter.

To contact the reporter on this story: Ben Bartenstein in New York at bbartenstei3@bloomberg.net

To contact the editors responsible for this story: Julia Leite at jleite3@bloomberg.net, Boris Korby, Brendan Walsh

©2019 Bloomberg L.P.