Guaido Pays Maduro's Debt to Keep Citgo Venezuelan

Guaido Pays Maduro's Debt to Keep Citgo Venezuelan

(Bloomberg) -- Juan Guaido just paid debt incurred by political rival Nicolas Maduro, the latest milestone in the battle between Venezuela’s dueling leaders.

Holders of the bonds due in 2020 from state-run oil company Petroleos de Venezuela SA received the interest payment Wednesday, according to two investors who own the notes and asked not to be identified. Alejandro Grisanti, a member of an ad hoc PDVSA board set up by Guaido, confirmed the payment and said the money came from accounts receivable at the oil company. It marks the “first financial transaction of the Guaido government,” he added.

Typically, a $71 million interest payment would receive little fanfare. Yet this is no ordinary debt disbursement. The bonds, which are the only notes Venezuela hasn’t defaulted on, are backed by a stake in Houston-based Citgo -- meaning that if the money wasn’t sent, creditors could seize the refining company. And while Maduro’s government remains in operational control of Venezuela, the payment shows Guaido’s power as the president of the National Assembly as he fights to overthrow the socialist leader as head of state.

“I cannot recall any other instance like this,” said Russ Dallen, managing partner at the brokerage Caracas Capital in Miami. “It’s a unique case in sovereign bond history.”

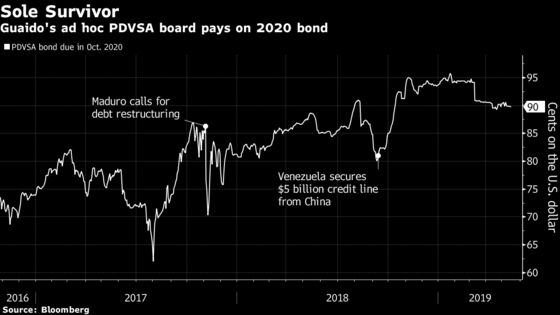

The bonds date back to a debt swap in October 2016 when cash-strapped PDVSA was seeking to ease its near-term payment burden. A portion of bondholders agreed to roll back maturities on debt they held in exchange for a lien on Citgo, the Houston-based refiner owned by PDVSA.

The notes currently trade at about 90 cents on the dollar, compared with around 30 cents for the nation’s defaulted bonds. Still, prices for the debt had dropped from a high of 95 cents in mid-January amid concern there could be a missed payment.

PDVSA will face an even tougher test in October when it must pay nearly $1 billion on the notes. The National Assembly probably won’t authorize the payment if the opposition hasn’t ousted Maduro from power, Torino Capital chief economist Francisco Rodriguez wrote in a report this week.

Another option would be for PDVSA to refinance the debt.

With the right incentive, investors could probably raise enough money to help PDVSA make the payment, said Mike Conelius, a Baltimore-based portfolio manager at T. Rowe Price, which holds the bonds.

“It would be short-sighted to see PDVSA default and then go through a fire sale,” he said.

To contact the reporters on this story: Ben Bartenstein in New York at bbartenstei3@bloomberg.net;Fabiola Zerpa in Caracas Office at fzerpa@bloomberg.net

To contact the editors responsible for this story: Julia Leite at jleite3@bloomberg.net, Brendan Walsh, Rita Nazareth

©2019 Bloomberg L.P.