(Bloomberg Opinion) -- The appetite for major consolidation sweeping the global food delivery industry has finally reached the U.S. Now the big question is, which combination would be easier to stomach? The fly in the soup may, as ever, be SoftBank Group Corp.

Waves of dealmaking have reduced the number of online food delivery players in markets such as the U.K. and South Korea to just two or three. In Germany, there’s only one — Takeaway.com NV. Yet the U.S. still has four major rivals: Grubhub Inc., SoftBank-backed DoorDash Inc., Uber Technologies Inc., another company in SoftBank’s stable, and the smaller Postmates Inc.

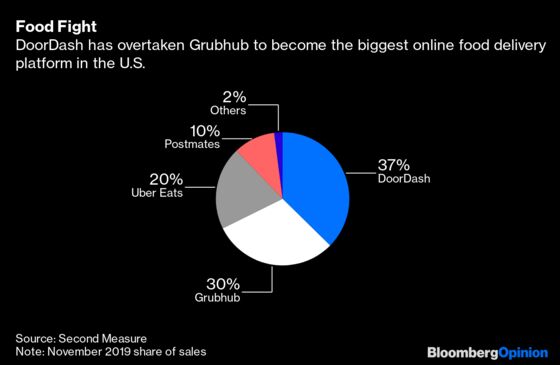

Grubhub is “considering strategic options including a possible sale,” the Wall Street Journal reported on Wednesday. The biggest U.S. player until 2018, it has lost market share to its venture capital-backed peers, and the stock had fallen 63% from its peak before the news hit.

The Chicago-based firm’s business model differs from its rivals. While the likes of Uber Eats provide a network of couriers to deliver food from their network of restaurants, Grubhub has operated largely as a digital platform since its founding in 2004. It simply connected restaurants to customers, leaving the eateries responsible for actually delivering the food. Under CEO and co-founder Matt Maloney, it became the dominant destination to order food online in the U.S.

His platform approach was a lot more profitable. Because Grubhub didn’t have to shoulder the costs of couriers, and just took a cut of each meal ordered, it was able to enjoy Ebitda representing more than 20% of sales between 2013 and 2017, when competition started to ramp up. Its rivals have always been loss-making.

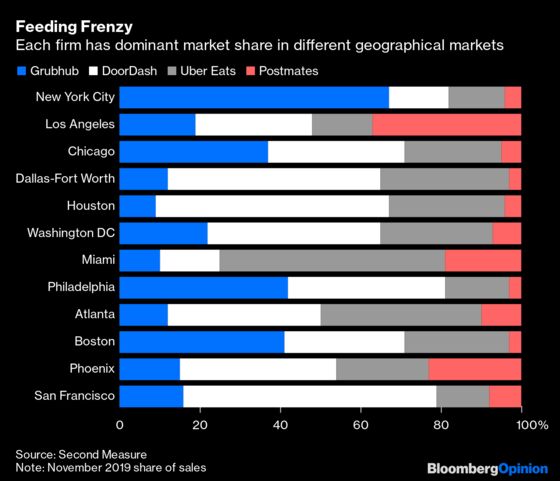

But that model also made it harder to attract major fast-food chains such as McDonald’s Corp., which don’t want to have to take on the fixed cost of maintaining a network of couriers themselves. So Grubhub has belatedly started building out that capability in an effort to defend its market share. However, that’s hurt profitability. Still, despite those headwinds, Grubhub remains an attractive business, not least because of its dominant position in New York, where credit-card data analysis firm Second Measure estimates it has 67% market share.

The difficulty lies in the deal price. Based on Grubhub’s cost of capital and anticipated 2022 earnings, a buyer would probably need to find annual savings exceeding $500 million by the end of that period to justify paying a 30% premium — even to the share price the day before the Wall Street Journal report, which would value the firm at about $6 billion including debt. Such savings would be a near impossible ask: Grubhub’s operating expenses over the past 12 months totaled just $1.2 billion. It would instead be a risky gamble on increased pricing power allowing the new firm to improve profitability enough to service any new debt. And the path to profitability for firms with their own couriers remains unclear. That probably rules out an approach by Amsterdam-based tech investor Prosus NV, which has no local business, reducing the opportunity both to find synergies and to remove a market competitor.

A merger with one of Grubhub’s existing U.S. rivals therefore seems a more rational solution. An all-stock combination would reduce concerns about justifying a capital outlay on a firm with low returns, while offering greater opportunities for cost savings and increased pricing power. And combining Grubhub’s major network of restaurants with a rival’s couriers could prove attractive.

But there are problems here, too. San Francisco-based DoorDash, arguably the most logical candidate strategically, was valued at nearly $13 billion in its most recent funding round. That sky-high figure would be a problem for Grubhub shareholders. Their firm may not be growing as quickly as DoorDash, but it is similarly sized and a lot more profitable. It’s hard to see them accepting a merger where DoorDash investors ended up with more than two-thirds of the combined entity.

Yet giving Grubhub shareholders a bigger stake could require DoorDash’s investors to write down the value of their holdings in the company. And that’s the last thing that SoftBank needs, fresh as it is from a year where underperforming investments such as Uber and troubled coworking-space trailblazer WeWork already prompted a $4.9 billion writedown. SoftBank is one of DoorDash’s biggest investors.

A combination with Uber Eats is the best alternative to DoorDash. But SoftBank again might create difficulties. If push came to shove, it’s more likely to favor an Uber Eats-DoorDash tie-up, rather than continuing to back two companies fighting each other for customers and restaurants.

Which leaves Postmates, the San Francisco-based firm which delivers everything from groceries to pizza and just expanded beyond food with an alliance with retailer Old Navy. It’s the less attractive solution for Grubhub, which would have to be the acquirer, and would be unlikely to add the scale needed to compete effectively. But such a combination does have some industrial logic — adding Postmates’s network of couriers to Grubhub’s restaurants — and is less likely to raise the hackles of antitrust regulators.

Were SoftBank not at the table, a combination with DoorDash or Uber Eats would make the most sense. But as it stands, Grubhub could be left fighting for the scraps.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2020 Bloomberg L.P.