Greatest Sell-Side Call Momentum Hits Risk Ceiling: Taking Stock

Greatest Sell-Side Call Momentum Hits Risk Ceiling: Taking Stock

(Bloomberg) -- The morning appears to be an extension of Monday afternoon that saw weakness leak into the tape. This may not be a surprise given the kinds of catalysts ahead, with the potential to complicate the upward melt over the past weeks. Also, Nomura strategists indicated that many "fickle market participants" may have moved to profit taking given the trade extension deadline discussed yesterday had been mostly priced in, together with a sense the market was a bit overbought.

FOMC Chairman’s Senate testimony, due in just a couple hours (crucial for color on the "Fed Pivot" responsible for the months long rally), Trump’s arrival in Vietnam ahead of his meeting with North Korea’s Kim Jong Un (the last time there was a meeting many foreign policy analysts were left scratching their heads), and the President’s ex-lawyer Cohen begins his testimony behind closed doors with the Senate intelligence Committee (his public testimony begins Wednesday) which the WSJ reported may indicate Trump engaged in criminal conduct while in office.

Flipped a Switch

A lot of things went right Monday, between the mega merger Monday in healthcare (and GE) and a lessening of trade tensions. It was as straight-forward a risk-on day as one could ask for, with the usual cyclicals rebounding while defensives lagged following the boundless optimism from the White House. But as forewarned, the S&P came up against some serious resistance once it tested its day’s lows, and gave way almost immediately.

Janney technical analysts ahead of the open Monday expected resistance "in the low 2800 range," while Stifel’s institutional equity strategist Barry B. Bannister wrote that they saw the S&P 500 "soon fading" along with GDP and EPS after they spotted “trouble” in the U.S. economy and equity market. The skepticism is not too surprising given his 2750 target is among the lowest on the street.

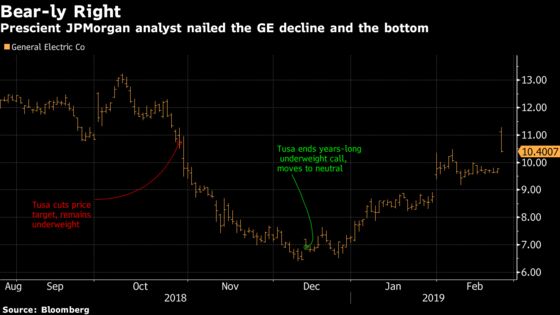

Greatest Sell Side Call in History Isn’t Over

GE’s resurgence wasn’t enough for the S&P, as its near 20% gains in the pre-market slowly evaporated as the day wore on. Deutsche Bank called the initial positive reaction "surprising," given the industrial conglomerate would now be left with less attractive components of its healthcare business that is lower growth and margin. Much of the Street chimed in throughout the day, but there’s one voice the Street is waiting for with bated breath -- the very soul who nailed the troubles at GE, and even called the bottom (though notably didn’t call for clients to buy, either), JPMorgan’s Steve Tusa.

Retailpocalypse, Take Two

Small taste of retail is on the way with Macy’s results due shortly, and if the bulls want to avoid a worsening in the S&P futures, which are down about a quarter percent as of writing, we’ll need to avoid a mini retailpocalpse that was nearly triggered in January. Macy’s gave up 16% with results in August, 7% with results in November, and 18% in a pre-announcement last month. And had it not been for the strongest bounce in equity markets that we’ve seen in decades, the S&P 500 500 Multiline Retail Index (S5MRET) may have suffered more than the 5% it did in mid January, an index that includes Kohl’s Nordstrom, and Target.

Department stores suffered during the latest holiday season, Credit Suisse analysts write, and struggled to clear inventory in January. Macy’s itself in mid January commented that they would continue to take the necessary steps to ensure a clean inventory position. We’ll see if that comes to fruition in less than an hour from now. Peers will be in focus, especially after Home Depot failed to impress earlier this morning, though not a department store perse.

Hope Is Not a Strategy

That is, unless your in the real estate segment, known for the infamous "hope trade." Today will be rife with housing-related data, from housing starts and permits to a variety of home price gauges for December that may show the extent to which falling treasury yields have translated to a stronger mortgage market and future demand. But those figures may not be enough for housing exposed stocks, now that the "Hope Trade" timeline has neared its conclusion -- a period from late fall through to late winter/early spring where investors attempt to get ahead of the selling season. That fact, together with the segment’s recent performance (S15HOME +18% YTD vs the S&P 500’s 12%) may give bulls pause.

Raymond James Monday added another homebuilder to its list of downgrades (KB Home this time, following recent cuts of DHI, PHM), citing recent valuations and the need to "step back" and evaluate the coming data. Though the analysts expect a strong season, odds may be stacked against outperformance.

Deutsche Bank analysts also discussed housing indicators, though flawed, that may indicate a strong season, if attendance at the IBS and KBIS shows were any guide. Citing attendance up 18% y/y for the combined shows (close to the all time record) that feature Kitchen and Bath industries and homebuilding, it is the "common view" that this bodes well for the segment. Analysts caution however that the figures tilt toward remodeling and new construction, while potentially being a lagging indicator.

That remodeling tendency was echoed at Credit Suisse following the IBS, where analysts discussed channel checks that indicated consumers continued their projects in conjunction with improved new home traffic through early February. They did cite however a "more cautious tone" from the home builders.

Armstrong World Industries beat expectations Monday, as the floors and ceiling manufacturer raised forecasts. Foundation Materials reported post market and beat on EBITDA, the top and bottom line, while its 2019 earnings forecast midpoint slightly missed. Home Depot results missed on comp. sales EPS while approving a 32% boost in the dividend and a $15 billion buyback program. Masco and Whirlpool, some of the most exposed suppliers to Home Depot, according to data compiled by Bloomberg, may respond as the mass retailer’s results provide slightly fresher detail as to the health of the segment in January. Homebuilder Tri Pointe group earlier reported a beat on the top and bottom line. Lowe’s results are due Wednesday.

Sectors in Focus Today

- Gene therapy names after the stellar day for the NBI index Monday, reaching levels not seen since October

- Retailers and department stores JWN, KSS, TGT after Macy’s results

- Hospital operators after Tenet’s forecasts beat expectations, following CYH last week

- Off price retailers ahead of a slew of reports, Dillard’s results post-market led shares to rise more than 5%

- Restaurants and fast casual names after PBPB soared and SHAK both initially rose after results, only to give back some gains

- Rental cars (again), after Hertz (with 37% short interest, according to financial analytics firm S3 Partners), surprised with its fourth quarter results and outlook; CAR also rose

Notes From the Sell Side

Caterpillar was double downgraded, with its rating going to sell at UBS from buy, after analyst Steven Fisher discussed the expectation that more than half of the construction and mining machinery manufacturer’s end markets may peak this year. He expects margins and revenue to be pressured in 2020 and demand to decline. Shares are down more than 3% pre-market as the analysts write that consensus, which implies 8% growth in EPS in 2020, is 16% too high.

In other downgrades, Old Dominion Freight Line was cut to neutral (from buy) at BofAML, mostly on valuation, but analysts led by Ariel Rosa write that the LTL shipper faces difficult y/y comparisons. The cut comes as the stock has rallied 23% this year, and the company is coming off what the industry has seen as the best freight market executives have seen in their careers. Rosa is cautious further appreciation is likely, and shares are responding, indicated to open lower by nearly 2%.

Tick-by-Tick Guide to Today’s Actionable Events

- Today: Senate Panel to Vote on Calabria FHFA Nomination

- JMP Securities Tech Conference

- BMO Global Metals and Mining conference

- Morgan Stanley TMT Conference

- Oncologic Drugs Advisory Committee of the FDA to review KPTI’s selinexor

- Pharmaceutical co. executives to testify to Senate over drug pricing

- 8:00am -- M earnings; JPM, GTES investor day; NTR CN at BMO Global Metals and Mining conference

- 8:30am -- Dec. Housing starts, building permits

- 8:30am -- HTZ, DISCA earnings call

- 9:00am -- Dec. S&P corelogic house prices

- 9:00am -- HD earnings call, AGR investor meeting; RGLD at BMO Global Metals and Mining conference

- 9:30am -- M earnings call

- 10:00am -- Feb. Richmond Fed manufacturing index; Feb consumer confidence

- 10:00am -- FOMC Chair Powell to testify before the Senate

- 11:00am -- NVDA at Morgan Stanley TMT Conference; AA at BMO Global Metals and Mining conference

- 1:00pm -- SYMC, PLAN at JMP Securities Tech Conference

- 2:00pm -- TROW Investor day

- 2:30pm -- TWLO at JMP Securities Tech Conference

- 4:00pm -- EAF at BMO Global Metals and Mining conference

- 4:05pm -- ELF earnings

- 4:15pm -- PZZA, WTW, PANW earnings

- 4:30pm -- ELF, PANW earnings call; TXN at Morgan Stanley TMT Conference

- 5:00pm -- PZZA, WTW earnings call

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.