Tech Superstars Should Pay a High Price for Keeping Secrets

Tech Superstars Should Pay a High Price for Keeping Secrets

(Bloomberg Opinion) -- Lately, there’s been frustration about holes in big technology companies’ financial disclosures. Personally, I always want more disclosure. Give me all the numbers.

But while journalists like me only have the power of the (digital) pen, investors have the power of the purse. They can and should flex their considerable muscle to press for more information. I acknowledge that Big Tech holds the most power in this relationship, but there is a history of investor discontent helping pry financial secrets out of the industry’s superstars.

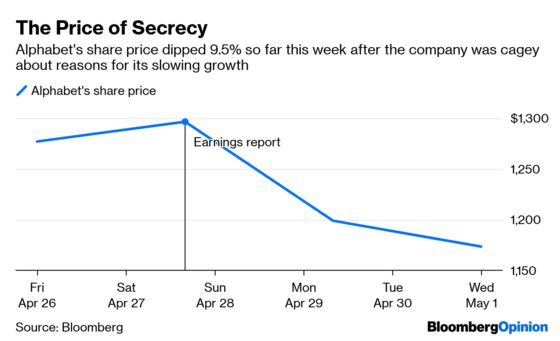

This week, it was hard to ignore the gripes about Google parent company Alphabet Inc., which posted relatively meek advertising revenue growth, for which executives offered vague explanations. (My Bloomberg News colleagues have theories about causes for the slowdown.)

Executives’ caginess fanned a longstanding question: Shouldn’t Alphabet detail the advertising sales and other financials of its big businesses, particularly YouTube? Alphabet really only reports revenue for its Google unit, which generates 99 percent of total company sales, and some of its constituent parts. Not helpful.

Bill Gurley, the prominent technology investor, weighed in on Tuesday by asking how large companies “get away with a lack of segment disclosure.” Not separating financial results for web search and YouTube doesn’t help investors trying to understand the company, Gurley tweeted.

I agree. And Google isn’t alone. Some investors want Facebook Inc. to report Instagram’s revenue. Twitter Inc. this year started divulging a number for daily users after long refusing to give it. There was grumbling when Apple Inc. recently stopped disclosing the number of iPhones it sells.

It does feel that as America’s technology giants grow even bigger and more sprawling, it’s getting increasingly tough to truly understand their businesses without different disclosures. Of course, there’s a natural tug-of-war between companies that prefer to reveal as little as possible and investors, journalists or other outsiders who want as much information as possible to understand a company’s performance and potential.

But it’s more complicated than that. Sometimes companies do volunteer more about their financials — and it tends to be when things are going badly and they want to show the world something good.

Amazon.com Inc.’s disclosure of revenue and operating profit from its Amazon Web Services division only started after a terrible stretch. In 2014, revenue growth slowed significantly, losses hit a record, its stock tanked and investors started to lose faith that the company was on the right track. Amazon needed to change investor feelings about the company, and revealing the profit goldmine of AWS was one of its tricks.

Stock owners didn’t hold a sit-in at Jeff Bezos’s office. Selling the stock in 2014 was their protest, and Amazon responded in part by divulging more. Amazon also has spilled some financial information, including revenue for its Prime membership club and other subscription services, after prodding by the Securities and Exchange Commission.

And one reason Google created the Alphabet conglomerate structure in 2015 was to mollify investors who wanted more insight into Google’s advertising businesses, and wished to keep a closer watch on the company’s spending for speculative ventures such as robots and computer-driven cars. This, too, was during a period in which Google’s financial results were wobbly and investors were unhappy.

Michael Pachter, a Wedbush Securities analyst, said successful companies and their executives generally believe they’re doing the right thing and don’t want to invite meddling from stock holders. "I largely agree with this attitude," Pachter emailed, "with a single exception: When things stop working, investors have a right to know why."

That’s perfect. (That’s what I said about Amazon a couple years ago, and Google makes Amazon look like an open book.)

But who gets to decide when things have stopped working for a company? Do Apple’s recent revenue declines count? What about Amazon’s e-commerce growth shifting into a slower gear? Does it count for Google’s stock to drop 9.5 percent this week in response to what might be just a blip in consistently strong growth? Does Facebook’s slow fade in revenue growth and profit margins count?

Maybe not yet. But without robust disclosures, outsiders can’t accurately gauge whether companies have stopped working. And that makes it tougher for investors to make informed protests with their wallets.

A version of this column originally appeared in Bloomberg’s Fully Charged technology newsletter. You can sign up here.

According to correspondence between Alphabet and the Securities and Exchange Commission, the agency's officials prodded the company in 2017 to justify its lack of financial disclosure for various segments including YouTube. In a vigorous back-and-forth by letter, Alphabet essentially said the most important segment disclosures are its Google unit and advertising sales by Google. It appears the SEC correspondence ended without further action.

The SEC examiners who review corporate financial disclosures regularly ask Amazon for more details on its costs or results from individual products and businesses, including over the years pressing for Amazon to disclose sales figures for its Kindle e-readers and Echo home speakers.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shira Ovide is a Bloomberg Opinion columnist covering technology. She previously was a reporter for the Wall Street Journal.

©2019 Bloomberg L.P.