Goldman Strikes Unusual Concession in Struggling $2 Billion Deal

Goldman Strikes Unusual Concession in Struggling $2 Billion Deal

(Bloomberg) -- With markets souring this month, Goldman Sachs Group Inc. found an unusual ally to help with a struggling buyout loan: hedge funds that had been betting against the target company.

The investment bank was lead underwriter for debt that financed United Natural Foods Inc.’s acquisition of grocery chain Supervalu, and as markets made investors increasingly skittish, Goldman faced potential losses if it struggled to place the debt. As bankers often do in such situations, they sweetened the pot.

But within the flurry of changes to the loan was one particular tweak that helped win over a select group: hedge funds and other investors who stood to reap a windfall on credit-default swaps linked to the grocery chain’s debt, according to people with knowledge of the matter.

It was yet another example of how the $10 trillion credit derivatives market, and the hedge funds who trade in it, can play pivotal roles in debt offerings. In just the last year, traders seeking to profit from derivatives bets have helped prop up distressed borrowers including homebuilder Hovnanian Enterprises Inc. and newspaper publisher McClatchy Co.

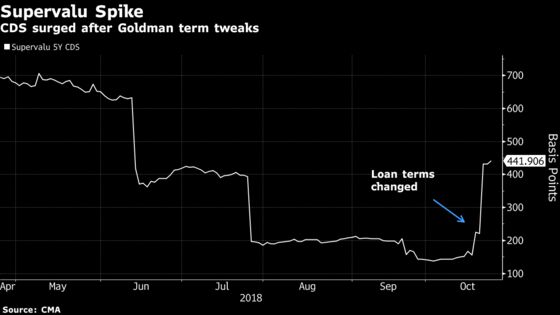

With the United Natural Foods deal, the key was in restoring the value of the roughly $470 million of net CDS wagers linked to Supervalu debt. The cost of those derivatives had plunged through this year on worry that the acquisition would eliminate the debt being insured.

Loan Sweeteners

By tweaking the loan documents to make Supervalu a co-borrower on the new debt, Goldman sparked a surge in the value of those swaps. That, along with several other concessions, helped the bank fill its order book for the loan, the people said. It also may have saved bankers from having to offer deeper concessions that would have increased United Natural Food’s borrowing costs or even put Goldman at risk of taking a loss.

Among the hedge funds that benefited from the CDS tweak was Anchorage Capital, according to the people, who asked not to be identified because the transactions are private.

Representatives for Goldman and Anchorage declined to comment.

Orphaned CDS

Behind the CDS trade is a situation commonly known in market parlance as an orphaned contract. Because new debt being issued to purchase Supervalu would’ve also paid down the grocer’s obligations, that risked leaving swaps linked to Supervalu effectively worthless because they would be linked to an entity with no significant borrowings.

As that possibility emerged, the cost to insure $10 million of Supervalu debt plunged from more than $630,000 annually in June to as little as $138,000 this month, according to prices from CMA. That’s far below the typical costs to insure junk-rated debt.

United Natural Foods, a supplier to Whole Foods, announced the $2.9 billion Supervalu acquisition in July. At the time, the buyer said Goldman Sachs had committed to providing financing for the transaction.

By the time Goldman started marketing the debt in early October, the markets had hit a turbulent patch, tumbling off all-time highs and sowing some doubt in the minds of those assessing the deal.

Leverage Concerns

One area they focused on was leverage, or the debt level relative to earnings, especially considering the combined business would throw off limited cash flow, according to one investor who passed on the deal.

United Natural Foods also relies on its contract with Whole Foods for more than a third of its revenue, and any change made to that contract could have a significant impact on the supplier.

Another factor weighing on investors was the presence of a large asset-backed loan, which would be more senior to the term loan they were agreeing to purchase. In the end, Goldman Sachs reduced the size of the term loan by $250 million to $1.8 billion. It also added a new $150 million one-year loan to win support from some securitized-loan buyers who were looking for short-dated paper, a person said.

The term loan was sold at 97 cents on the dollar, reducing the proceeds to the company. It also traded below its issue price on Tuesday, according to prices compiled by Bloomberg.

While the concessions offered to CDS investors were but one factor in Goldman’s ability to sell the debt, traders in the market pounced on the opportunity to boost the value of Supervalu swaps. By Tuesday, the CDS cost had jumped to 431 basis points, or $431,000 per $10 million insured, CMA prices show.

--With assistance from Claire Boston.

To contact the reporters on this story: Sridhar Natarajan in New York at snatarajan15@bloomberg.net;Katherine Doherty in New York at kdoherty23@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, ;Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Shannon D. Harrington, David Scheer

©2018 Bloomberg L.P.