Goldman Sees Another Weak Year After a Lousy 2018

The gloomy outlook matches the experience of what’s been a rough year for financial markets.

(Bloomberg) -- Slowing economic growth, shrinking central bank balance sheets and continued bouts of volatility will help make 2019 another poor year for risk-adjusted investment returns, with few obvious havens, according to Goldman Sachs Group Inc.

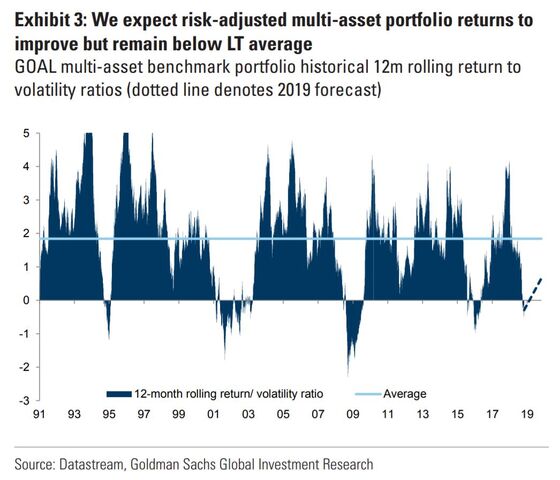

“Expect better but still low returns in 2019” for multi-asset global allocation portfolios, Goldman strategists including Christian Mueller-Glissmann wrote in a note Monday. While the decline in valuations across asset classes has improved the medium-term outlook, “we see a weaker expected macro backdrop in 2019 as likely to limit return potential,” they wrote.

The gloomy outlook matches the experience of what’s been a rough year for financial markets. Investors have been rattled by everything from monetary policy normalization to tariff threats to global trade, a slowdown in China and the prospect that corporate-earnings growth has peaked. In what some have called a regime change, bonds have also been poor hedges for equities, upending the classic 60-40 portfolio strategy.

For their part, the Goldman strategists still advise an overweight allocation to stocks with the S&P 500 posting positive returns this year, but recommend a bigger holding of cash than benchmarks suggest and have an underweight call on bonds. The team downgraded credit to underweight last week.

“We still see poor risk-adjusted returns in fixed income: we forecast negative total returns for bonds with more upward pressure on yields and credit spreads” in the first half of next year, they wrote. “There may be less reason to be bearish” on bonds by the latter part of 2019, as 10-year Treasuries “could reprice in the event of a more severe growth slowdown or deeper equity drawdown,” they said.

While far from catastrophic, this year is set to go down as one of the worst years for risk-adjusted cross-asset returns outside of crisis periods over the past quarter century, Goldman analysis indicates.

Though questions are emerging about the “strategic case” for commodities, Goldman has an overweight call on the asset class, with “significant near-term upside to oil” after the big tumble in crude the past two months. The team favors gold, with the dollar expected to weaken next year.

With the traditional bond hedge to equities unattractive, Goldman has also recommended that investors consider derivatives. With higher volatility, one tactic could involve selling calls on equities and buying puts after rallies, and buying calls and selling puts after “sharp corrections,” the strategists wrote separately last week.

To contact the reporter on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Cormac Mullen, Dave Liedtka

©2018 Bloomberg L.P.