Glaxo Surges as Street Takes Latest Deal Better Than Last One

Glaxo Surges as Street Takes Latest Deal Better Than Last One

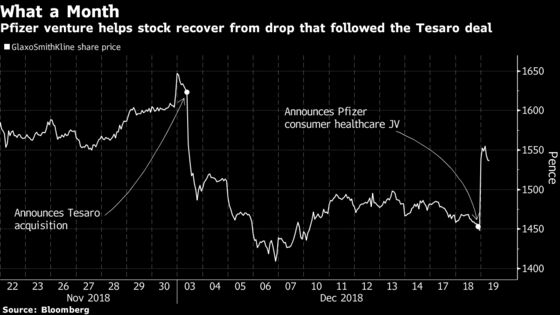

(Bloomberg) -- GlaxoSmithKline Plc shares had their biggest intraday jump in 10 years after the U.K. pharmaceutical giant announced a consumer-healthcare joint venture with Pfizer Inc. that will put brands like Nicorette nicotine gum and ChapStick lip balm under one roof. The venture will be listed separately in London within three years, GSK said.

Analysts applauded a target for the joint venture to generate annual cost savings of 500 million pounds ($632 million) by 2022, while Glaxo’s commitment to its dividend policy was also well received.

Wednesday’s gain of as much as 7.8 percent helped the stock claw back some of the drop that followed this month’s news that Glaxo was to buy U.S. cancer treatment maintenance firm Tesaro Inc., a deal that was viewed as expensive by many analysts.

Here’s a summary of what analysts had to say on the latest transaction:

Liberum, Graham Doyle

(Hold, price target 1,700p)

- Joint venture “makes significant sense” as it’s a capital-light way of achieving the synergy benefits of an acquisition. Potential for an acquisition as opposed to a joint venture caused much concern over the past 12 months.

- However, should Glaxo de-merge its consumer-health business that leaves the rest of the group increasingly reliant on a research & development turnaround, which is now itself more reliant on the Tesaro deal -- “a transaction that we are skeptical of.”

Shore Capital, Adam Barker and Tara Raveendran

(Buy)

- “Delivery of the synergies will be important in ensuring an acceptable return on capital.”

- Estimates that, prior to synergies, the partners will earn about 4 percent return on gross assets contributed to the joint venture. This rises to about 6 percent if annual cost savings of half a billion pounds are realized.

Bloomberg Intelligence, Sam Fazeli and Cinney Zhang

- Joint venture will pad Glaxo’s top line optically without deploying cash, while synergies will help cash flow in the near term where its pharma business is facing headwinds.

- “This may give Glaxo time to build out its pipeline, so its pharma unit looks its best when the sector-leading consumer unit is spun off.”

Jefferies, Peter Welford

(Buy, PT 1,750p)

- There is strategic rationale in the combination, given cost savings, while the separation of the group will crystallize value.

- Confirmation of dividend policy target for 2018 2019 is important.

Credit Suisse, Trung Huynh

(Neutral, PT 1,600p)

- In the event of a consumer initial public offering, GSK shareholders will need faith in management’s ability to deploy the proceeds to build a sustainable pharma business.

- Profitability of consumer-health unit should give comfort on supporting the “high” dividend payout.

RBC, James Edwardes Jones

(Underperform on Reckitt Benckiser, PT 5,100p)

- Says the margin target is “interesting” when looking at rival Reckitt Benckiser, as it’s lower than that targeted by Reckitt’s health business (excluding Mead Johnson), despite being a significantly larger business.

- “We think it supports our view that Reckitt is over-earning and margins need to come down.”

--With assistance from Albertina Torsoli and Celeste Perri.

To contact the reporter on this story: Joe Easton in London at jeaston7@bloomberg.net

To contact the editors responsible for this story: Beth Mellor at bmellor@bloomberg.net, Paul Jarvis

©2018 Bloomberg L.P.