Glassman’s Gateway Deal Offers Little Windfall for Catalyst Fund

Glassman’s Gateway Deal Offers Little Windfall for Catalyst Fund

(Bloomberg) -- At first blush, it looks like Newton Glassman, Canada’s distressed debt king, capped a forgettable 2019 with two massive wins.

Just two days after Christmas, Glassman’s Catalyst Capital Group Inc. sold its Canadian casino company, almost eight years after it first tried to exit its investment. A week later, Catalyst persuaded an investment group to sweeten its offer a second time for Hudson’s Bay Co., likely ending a six-month battle over the Saks Fifth Avenue owner.

A closer look shows that while the HBC transaction may yield double-digit gains for Catalyst, the Gateway deal won’t result in any significant windfall for its backers. Some of these investors had already been reluctant to invest fresh cash into the private equity firm, according to people familiar with the matter, including four who were sounded out starting in 2017 on plans for a potential new fund.

Catalyst has owned Gateway Casinos & Entertainment Ltd., one of Canada’s biggest gaming companies with 25 properties, since 2009. After at least two looks at going public, it filed for an initial public offering in November 2018, targeting a total valuation of as much as C$2.5 billion ($1.9 billion), a person familiar with the matter said at the time.

That’s a far cry from the sale announced this month with Leisure Acquisition Co., known as a special purpose acquisition company. It values the combined entity at C$1.46 billion, with debt. Looking at it another way, Catalyst’s 30% equity stake in the new firm is worth about $132 million, according to the deal metrics released this month. As recently as the third quarter of 2019, Catalyst said its 74% stake was worth more than $750 million, according to a report sent to investors.

A representative for Toronto-based Catalyst said these numbers “are wrong and don’t reflect important aspects of the transaction in terms of the structure, equity, cash, non-participating assets and the value delivered to Catalyst LPs over the last six years through refinancings and other transactions.” The firm is under restrictions to comment given the marketing of the Gateway transaction.

Sweeter Bid

On the proposed Hudson’s Bay deal, Glassman scored a major win for minority shareholders by prompting a higher bid from a group led by Chairman Richard Baker. Catalyst accumulated shares over the summer, amassing a 17.5% stake to fight for a better price, while appealing to the Ontario Securities Commission for a delay in the shareholder vote.

Based on the sweetened Baker offer of C$11 a share, Catalyst would post a return of 8.8% on the shares it bought in August. Catalyst also snapped up stock sold by the Ontario Teachers’ Pension Plan in June for C$9.45 a piece, resulting in a potential 16% gain.

Still, Catalyst missed much of the upside in the stock by buying the bulk of its shares after Baker’s first bid in June at C$9.45 each. Before that offer, the stock traded as low as C$6.22 on June 7.

The Catalyst representative said that “should the transaction be completed, the return will be materially higher than what Bloomberg’s calculation attempts to show.” He said the calculation is missing several key data points.

Tough Year

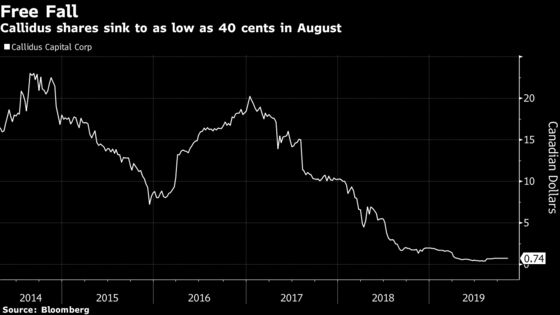

The potential deals follow a tough year for Catalyst, which specializes in buying the debt of troubled companies -- a world Glassman once described as a “blood sport.” His publicly traded debt unit -- Callidus Capital Corp. -- was taken private for just 75 cents a share in October after mounting losses from bad loans pushed it to the brink of insolvency. Catalyst, which owns 70% of Callidus, took the lender public in 2014 at C$14 a share.

“It’s clear it is a sad story and nobody is trying to put a different spin on it,” David Sutin, chair of the special committee of Callidus’s board, said after shareholders approved the bid from U.K. billionaire Joe Lewis to buy out minority shareholders for about C$5 million.

In numerous court filings over the years, Catalyst has blamed Callidus’s woes on a systematic attack by dozens of Bay Street short-sellers, dubbing them the “Wolfpack conspirators.” Callidus said in a recent regulatory filing that the shorts sought to “materially impair” its business, which hurt its ability to originate new loans and raise financing.

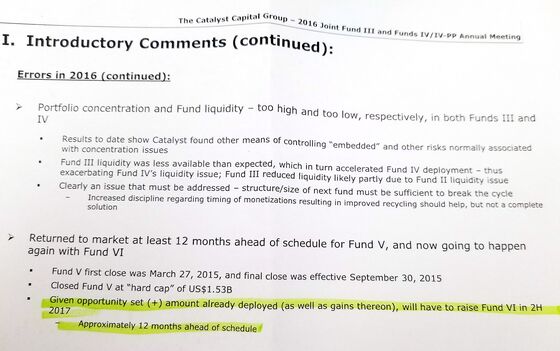

Some Catalyst investors have since grown cautious, worried that the troubles at Callidus Capital could spill over to the private equity firm, according to people familiar with the situation. They showed little appetite to put more money into a potential new fund -- what would have been the firm’s sixth -- that Glassman had planned to raise in 2017, according to several people familiar with the plan, including those who were sounded out on the fund. Plans for the so-called Fund VI were referenced in a report for a fund annual meeting on April 4, 2017. The fund was never put in place, and no papers were filed.

The Catalyst representative said the firm never attempted to raise money for a new fund, calling it “completely false.” The terms of its previous fund, Fund V, restricted it from initiating fundraising.

“This is an attempt to express a failure in something that has never occurred,” the official said.

Investors in the earlier Fund III are now being asked to wait another year to get their money back, giving Catalyst more time to sell assets including Advantage Rent A Car, according to a fund update sent to backers last month. The $1 billion fund is now targeting the end of 2020 for a return of money, rather than the end of 2019, according to the update. The fund was started in 2009. Catalysts’ backers include a long list of blue-chip investors including the Rockefeller Foundation, which declined to comment for this article, and the Arizona State Retirement System, which didn’t respond to requests for comment.

The Catalyst representative objected to this “misinformed characterization. The automatic one-year extension is not a delay, it is a contemplated aspect of our LP agreement as a means to allow for the maximization of returns, which has been agreed to, and supported by, our LPs.” LPs refer to limited partners in the funds.

Ira Gluskin, a Canadian money manager and a former director of the University of Toronto’s asset management arm that invests with Catalyst, expressed his frustration at a conference last year, saying he is an “unhappy investor” who wants his money back, according to a Globe and Mail report at the time. Gluskin declined to comment for this story.

To contact the reporter on this story: Paula Sambo in Toronto at psambo@bloomberg.net

To contact the editors responsible for this story: Shannon D. Harrington at sharrington6@bloomberg.net, David Scanlan, Larry Reibstein

©2020 Bloomberg L.P.