Ghost Towns Still Haunt Spain in Property Rebound a Decade After

Ghost Towns Still Haunt Spain in Property Rebound a Decade After

(Bloomberg) -- Juan Velayos’s biggest headache these days is getting licenses fast enough to hand over new homes such as the upscale condos his company is building in the northern suburbs of Madrid.

Less than 60 miles away, Ricardo Alba’s neighborhood tells a different story about Spain’s property market. The fencing instructor is one of only two occupants at a block of apartments whose development was frozen in its tracks when banks pulled the plug on credit.

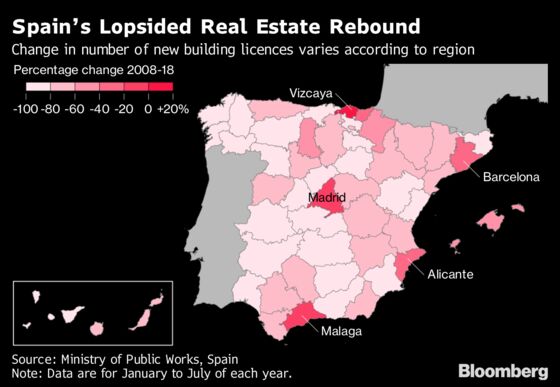

“The real estate sector’s recovery in Spain is developing at two clearly different speeds,” said Fernando Rodriguez de Acuna, director of Madrid-based real-estate consultancy R.R. de Acuna & Asociados. “While one part of the country is consolidating the recovery of the sector and even expanding, another part of the country is stagnating and is showing few signs of returning to pre-crisis levels in the medium- and long-term.”

A decade after the financial crisis hit, Spain’s real estate recovery is a tale of two markets. Key cities and tourism hot spots are enjoying a fresh boom, fueled by interest rates that are still near historic lows, an economic recovery and a banking system that’s finally cleaning up its act. Private equity firms such as Blackstone Group LP are picking up once-toxic assets worth tens of billions of dollars and parsing out what’s still of value, often using their playbook from the U.S. real estate recovery to convert properties into rentals.

But travel a little beyond the bustling centers, to the outskirts of smaller villages, and ghost towns still litter the landscape -- once ambitious developments, often started on agricultural land that was converted into building lots just before the crisis hit. They still stand half finished, unable to find a buyer.

Billboard Dreams

The “Bioclimatic City La Encina” where Alba began renting an apartment two months ago is such a development. Situated on the edge of the village of Bernuy de Porreros, about 10 kilometers (6 miles) from Segovia, it promised to be Spain’s first environmentally-friendly town, providing solar energy and recycled water for 267 homes, comprised of two-, three-, and four-bedroom chalets and apartments. A faded billboard speaks of the dreams that were sold, including communal swimming pools and gardens for residents who would “live... naturally.”

Today, only about a dozen of the homes are occupied. One street has finished homes but half have their windows bricked up to discourage break-ins, locals said. Alba does have solar panels heating his water, but his electricity comes from the local network. On the far side of the development, trees sprout out of the middle of a street that was never paved. Brightly-colored pipes and cables protrude from the ground. Bags of plaster on a pallet have long hardened.

Spain’s housing crash was fueled by a speculative frenzy combined with loose restrictions and corruption that allowed plots of farmland in rural villages to be converted to feed a demand for homes that never truly existed, said Velayos, who is chief executive officer of Neinor Homes. At the height of the boom in 2006, authorities approved 865,561 new home licenses when even in an economic boom demand is no greater than 250,000 homes, he says.

Banks were handing out loans to developers who had little to lose if a project didn’t find a buyer because the money wasn’t theirs. The result was an almost total collapse of the market and close to $200 billion of soured assets.

About half of them were bought in 2012 by Sareb, a bad bank set up by the government to help lenders. Sareb spent about 50 billion euros to acquire assets that were once valued at twice that amount, mostly loans to developers and real estate. Among the latter are also 97 of the 267 properties at La Encina. None of them are currently for sale as Sareb works through legal issues and construction of many isn’t finished.

Other assets were picked up by deep-pocketed investors such as Blackstone, which has 25 billion euros invested in Spain, according to Claudio Boada, a senior adviser at the firm. The New York-based company -- the world’s largest private markets investor -- is doing what it did at home after the financial crisis: renting out homes instead of selling them in a bid that fewer people can afford to own. Spain had a relatively high home ownership rate before the crisis but it has since come down.

Blackstone’s Bet

“We’re holding most of what we own and looking to rent it out for the foreseeable future,” said James Seppala, head of real estate for Europe at Blackstone. “There’s a meaningful increase in demand for rental residential around the world, including in Spain, driven by home ownership rates coming down.”

Private equity investors also backed a new breed of real estate developers that are bringing a different rigor to the industry. Companies such as Neinor and Aedas Homes S.A.U. are more tech-savvy when assessing markets, and emphasize industrial production techniques to improve efficiency. They’re behind a surge in licenses for new homes to 12,172 new homes in July, the highest monthly total in a decade.

But demand is uneven: Madrid is enjoying its most robust year of home construction since 2008 with an average of 2,151 licenses awarded per month in the first seven months of the year. In Segovia, just 27 minutes from Madrid on the state-run bullet train, an average of 25 homes licenses have been approved per month in 2018, compared with an average of 180 homes a decade earlier.

The volume of residential mortgages sold in Spain peaked in late 2005 before hitting a low in 2013. Since then they have gradually picked up, with 28,755 sold in August, a seven percent annual increase.

Velayos, chief executive officer at Neinor, said business is starting to pick up beyond Madrid and Barcelona to smaller cities and the coast. His company plans to hand over 4,000 homes by 2021, more than 12 times as many as in 2017. The biggest challenge has been getting licenses approved on time. Velayos had to cut his delivery target for 2019 by a third as often understaffed local councils cause bottlenecks in the production process.

More significantly, Spain’s real estate is now funded by investor’s equity and not credit, said Velayos. Neinor was bought by private equity firm Lonestar Capital Management LLC from Kutxabank SA in 2014 and went public in March 2017. Aedas is backed by Castlelake, another private equity investor, and was floated the same year. Metrovacesa SA, owned by Spain’s biggest banks, held an initial public offering earlier this year.

Shares of all three developers have declined this year at more than twice the rate of the local stock index, a reminder that the market’s recovery remains fragile, with higher interest rates and an economic slowdown on the horizon.

For the Bioclimatic City La Encina, that means it may take longer still until Alba gets new neighbors. Prices for half-finished chalets were slashed by half, according to residents. Some now sell for as little as 16,700 euros, half the cost of a mid-range car.

Alba doubts such cuts will lure buyers. Then again, that may not be a bad thing, he says in summing up the development’s advantages: “It’s very peaceful.”

--With assistance from Samuel Dodge.

To contact the reporter on this story: Charlie Devereux in Madrid at cdevereux3@bloomberg.net

To contact the editors responsible for this story: Dale Crofts at dcrofts@bloomberg.net, Christian Baumgaertel, Charles Penty

©2018 Bloomberg L.P.