Ghana Works to Show It Can Stick to Budget as IMF Deal Ends

Ghana Sets Out to Show It Can Stick to a Budget as IMF Deal Ends

(Bloomberg) -- Sign up for our new Stephanomics podcast.

For the 16th time since the 1960s, Ghana is wrapping up a financial bailout from the International Monetary Fund and stepping away from the lender’s oversight. Now, it’s up to one of Africa’s perennial overspenders to show that it can stick to a budget.

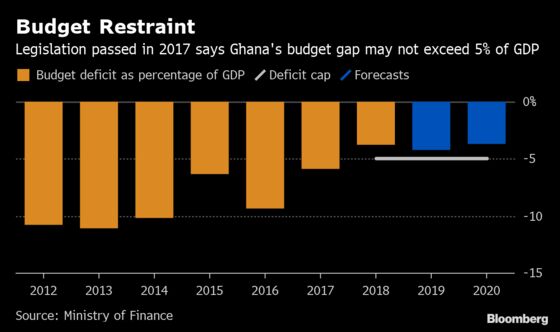

The previous time Ghana was in this position was in July 2012, five months before general elections, the country recorded the first of three consecutive annual fiscal deficits that exceeded 10 percent of gross domestic product. Its huge debt burden became even more difficult to service when erratic power supplies weighed on growth and sent the currency on a downward spiral, prompting it to turn to the IMF again in 2015.

Now, two years after the government of President Nana Akufo-Addo came to power on a pledge to take “Ghana Beyond Aid,” the deficit has narrowed, inflation has slowed, debt levels have stabilized and economic growth is accelerating, estimated at 5.6 percent for last year and 7.6 percent for 2019. Reforms that range from legislation that outlaws large deficits to the establishment of fiscal supervisory councils and an aggressive banking-sector overhaul will do away with the need to ask the IMF for a 17th bailout after it passed the final review of the current one on March 20, according to the government.

“It’s about a fundamental and basic matter all of us as Ghanaians have to bear in mind, and that is discipline in the management of our public finances,” Akufo-Addo, who is likely to run for a second term in a vote late next year, said in a televised speech on March 25. “You don’t spend money that you don’t have, that is always the road to chaos.”

Ghana’s sale of $3 billion in Eurobonds last month, the country’s biggest yet and oversubscribed more than six times, was proof that investors have faith in its financial management, Finance Minister Ken Ofori-Atta told lawmakers March 28.

Here is a round-up of where Ghana fell short and what to look out for after this week:

What Ghana Didn’t Do

- The government didn’t rein in the wage bill sufficiently, after overruns “by a little value” at the ministries of education and health, said IMF country representative Albert Touna Mama.

- Ghana missed a target level for net reserves at Dec. 31 after the central bank had to allow the repatriation of securities held by foreign investors.

- “There are structural reforms such as public-sector efficiency and a reduction in the huge wage bill that Ghana failed to implement,” said Godfred Bokpin, senior finance lecturer at the University of Ghana.

What to Watch

- “Post-IMF, the key issue would be maintaining the fiscal discipline and doing so across the elections cycle,” said Stuart Culverhouse, London-based chief economist at Exotix Partners LLP. Ghana needs to improve revenue collection to consistently meet its revenue targets, he said.

- “The political stakes are high,” Bokpin said. “The elections are already with us and it’s obvious that in the last two years, government hasn’t done any critical infrastructure. For the average Ghanaian seeing is believing.”

What the IMF Says

- “I think the country has everything it takes to do without an IMF program,” Managing Director Christine Lagarde said during a visit to Ghana in December. “I hope that there would not be these external shocks, whether it’s a sharp and durable drop in commodity prices or massive increases in tensions that could hamper any trade. If it did, then clearly not just Ghana but quite a few countries would need our help and we stand ready.”

What Bloomberg’s Economist Says

“Ghana entered the program because it needed to improve macro-economic stability, largely caused by chronically high budget deficits, and therefore on that score I’d say the program achieved its purpose as the fiscal situation improved dramatically.”

-- Mark Bohlund, economist

--With assistance from Andre Janse van Vuuren.

To contact the reporters on this story: Ekow Dontoh in Accra at edontoh@bloomberg.net;Moses Mozart Dzawu in Accra at mdzawu@bloomberg.net

To contact the editors responsible for this story: Andre Janse van Vuuren at ajansevanvuu@bloomberg.net, Rene Vollgraaff, Robert Brand

©2019 Bloomberg L.P.