Lagarde Stares at German Budget Surplus With Sights on Stimulus

Lagarde Stares at German Budget Surplus With Sights on Stimulus

(Bloomberg) -- In the year the European Central Bank doubled down on calls for more fiscal stimulus, the euro area’s biggest economy managed the feat of a record budget surplus instead.

Germany’s federal government amassed an excess of 13.5 billion euros ($15 billion) last year -- helped by low interest rates and a benign outcome to Brexit talks.

For ECB President Christine Lagarde, the surplus underscores a key imbalance of the currency area she leads, where longstanding fiscal rectitude in its largest constituent contrasts with more persistent deficits in its next three-largest economies. With much of her monetary ammunition already spent, Germany’s stash of money may be the region’s best hope to potentially cushion the blow in a future crisis.

“Sadly, I think that we won’t get necessary shifts in fiscal policy unless we are staring into the abyss,” Rupert Harrison, chief macro strategist at BlackRock International, told Bloomberg Television last week. “We will need a little bit of instability first.”

The German outcome marks the sixth year in a row where the government managed to at least balance the budget. The last record was in 2015, with a surplus of 12.1 billion euros.

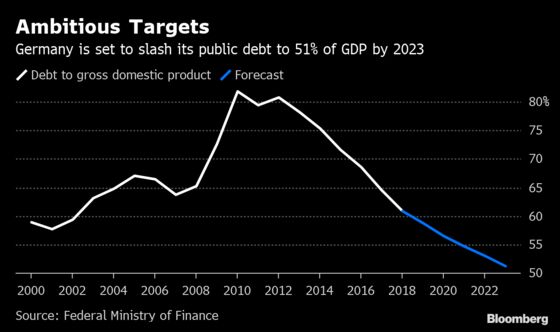

The bulk of the excess was a result of lower-than-expected interest rates making it cheaper for the country to service its debt. Tax revenue was also higher than anticipated, while the possibility that the U.K. would leave the European Union in a disruptive exit at the end of October was averted by a last-minute deal -- meaning Germany’s public finances could stay on track without the need for emergency spending.

The surplus shows that the ECB’s calls last year for fiscal stimulus from countries that can afford it went largely unheard in the country with the greatest ability to do so.

Former ECB President Mario Draghi intensified that plea before he left at the end of October, while Lagarde has kept up the pressure. Just last week, she told French magazine Challenges that “a concerted fiscal stimulus at the euro-area level would help speed up growth.”

“Greater cooperation between competent authorities, without infringing on the independence of their roles, would make it possible to optimize the multiplier effects of their decisions,” she said, apparently in vain for now.

Germany’s outstanding public finance health -- the result of rigid fiscal discipline in Berlin -- was achieved at a time of relative deterioration in the economy itself. Growth last year is expected to have slowed to 0.5% from 2.5% in 2017, due largely to weaker exports.

The surplus is still likely to prompt renewed calls for increased investments or tax cuts with Germany. Economy Minister Peter Altmaier has been pushing for a reduction in corporate taxes and a complete phaseout of the so-called Solidarity tax used to finance reunification, a proposal Finance Minister Olaf Scholz has thus far opposed.

Scholz said on Monday that he wants to use the surplus, which totals 19 billion euros if unused money from last year is taken into account, to spend more on schools and measures to combat climate change.

“We had a bit of luck and good management,” he told reporters.

Scholz and Chancellor Angela Merkel have stuck to their balanced budget policy, arguing that public investments are already growing steadily. The government faces increasing spending to implement measures to combat climate change, including possible compensation for energy utilities to exit from coal-fired power generation.

“In Germany’s case, they’ve got loads of fiscal power if they need it,” John Roe, Legal & General Investment Management head of multi asset funds, said last week. “But the reality is, they consistently say, ‘we don’t think it’s necessary.’”

Read More:

- Germany Debuts Green Bonds in 2020 to Support Climate Action

- Germany Ready to Counter Crisis If Needed, Merkel and Scholz Say

- Germany Needs $500 Billion Public Investment After Lost Decade

- Germany Sticks to Balanced Budget But Ready With ‘Many Billions’

--With assistance from Tom Keene, Anna Edwards and Matthew Miller.

To contact the reporters on this story: Birgit Jennen in Berlin at bjennen1@bloomberg.net;Craig Stirling in Frankfurt at cstirling1@bloomberg.net

To contact the editors responsible for this story: Ben Sills at bsills@bloomberg.net;Simon Kennedy at skennedy4@bloomberg.net

©2020 Bloomberg L.P.