General Electric’s Split Marks End of a Bond Market Behemoth

General Electric’s Split Marks End of a Bond Market Behemoth

(Bloomberg) -- General Electric Co.’s split into three separate companies marks the final stage of a great deleveraging for what was once among the most highly rated and heavily indebted U.S. corporations.

GE is on target to cut its debt burden by more than $75 billion in the three years through next month thanks to operational changes designed to boost cash flow and profit margins, the company said Tuesday. There are opportunities for more progress after that, the company said in an investor presentation.

The once-sprawling industrial conglomerate has been slashing its debt since Chief Executive Officer Larry Culp took the helm in 2018. Large asset sales, including the $30 billion sale of its aircraft leasing unit to AerCap Holdings NV earlier this year, are helping GE achieve that goal.

| For more coverage |

|---|

|

GE reported $65.8 billion of debt as of Sept. 30, down from $134.6 billion at the end of 2017.

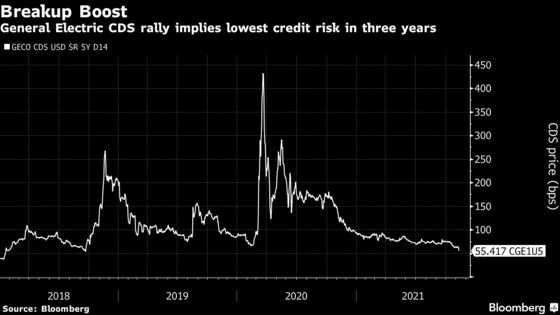

Credit default swaps tied to GE rallied to their best levels in more than three years Tuesday morning in New York, implying that investors see less risk for owning the company’s debt in the years ahead. While the split is likely to “cause near-term bond volatility without defined capital structures for the three units,” it could be “favorable for the aerospace unit,” wrote Bloomberg Intelligence credit analyst Joel Levington.

GE once ranked among the credit world’s elite issuers, holding triple-A ratings from 1956 until 2009 when the financial crisis and recession cast doubt on the stability of the conglomerate’s financial arm, GE Capital. The parent company’s ratings have since descended toward the edge of junk over the past decade, with a BBB+ grade at S&P Global Ratings and Baa1 at Moody’s Investors Service.

The prospect of a split didn’t immediately improve GE’s ratings prospects, with S&P putting the company on CreditWatch for a possible downgrade and Moody’s affirming its rating Tuesday but keeping its negative outlook. S&P said it would make a decision “once we have more details on the impact of the health care separation on GE’s financial risk profile and potential for debt reduction.”

The breakup positions GE’s remaining aerospace unit to potentially reclaim an A level credit rating down the road with its more manageable balance sheet, Levington said. He’s looking for GE’s longer-dated bonds, which currently trade wide of peers, to outperform.

Read More: GE Pulls Out Tyco Playbook, May Cause Bond Bounce: Credit React

Fitch Ratings affirmed GE’s BBB rating Tuesday, writing that “operating performance at GE’s other industrial segments will improve further as a result of ongoing restructuring.”

©2021 Bloomberg L.P.