General Electric Is Flashing Caution Signs in Credit Markets

General Electric Caution Signs Are Flashing in Credit Markets

(Bloomberg) -- General Electric Co. may still have a relatively solid investment-grade rating, but investors aren’t taking their chances. They’re snapping up derivatives that protect against losses on the company’s debt.

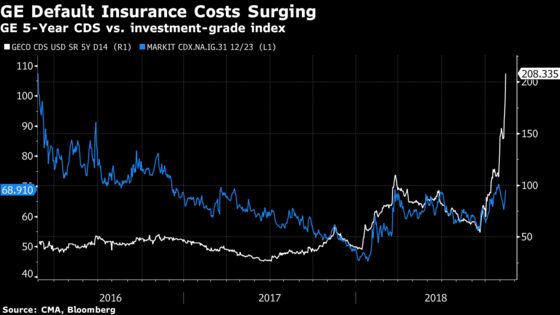

The annual cost to insure against a default by GE for five years climbed above 200 basis points for the first time in years, credit-default swap prices from CMA show. That’s almost double what it cost just two weeks ago, and it’s the kind of level that hasn’t been seen for the company since the waning days of the global financial crisis.

That’s still well below the peak crisis levels for GE’s finance unit back then (GE Capital CDS surged to more than 1,000 basis points in March 2009). But the pace of the increase has been rapid, particularly when compared with the broader investment-grade market. Yields on some of GE’s bonds have also reached levels that are in line with junk-rated bonds, Bloomberg Barclays index data show.

Chief Executive Officer Larry Culp tried to reassure investors that the company is prioritizing debt reduction in its effort to combat a multiple-front crisis in a televised interview on Monday, when the bond market was closed. GE is facing weak demand for gas turbines, high debt levels and a federal accounting probe. Its shares have fallen more than 25 percent since Culp’s surprise appointment as CEO was announced Oct. 1, extending a sell-off that has wiped out more than $200 billion in market value since the end of 2016.

Representatives for Boston-based GE didn’t immediately provide comment.

‘Escalating’ Concerns

In his first earnings announcement as CEO, Culp said the company was cutting the quarterly dividend to just a penny a share from 12 cents in an effort to conserve cash and strengthen its balance sheet. Still, credit and equity analysts remain cautious. If GE’s credit ratings were further downgraded, the company could face rising borrowing costs and other expenses that would further pressure its liquidity, Gordon Haskett analyst John Inch wrote in a note.

GE may not be alone in facing these risks, some money managers fear. U.S. investment-grade bonds have been one of the worst-performing U.S. asset classes this year, as rising interest rates have lifted companies’ funding costs and sapped investors’ returns. More pain may be coming for investors, and it could be severe, distressed-debt money manager Marc Lasry warned late last month. Scott Minerd, global chief investment officer of Guggenheim Partners, said on Tuesday that more investment-grade credits will suffer.

“The selloff in GE is not an isolated event,” he wrote in a Twitter post. “More investment grade credits to follow. The slide and collapse in investment grade debt has begun.”

There are around $2.5 trillion of bonds rated in the lowest tier of the investment-grade universe, more than triple the level at the end of 2008. Some of those securities, including issues from GE and Ford Motor Co., trade like they are already rated junk.

Yields Climbing

Despite being cut to the lowest investment-grade tier, GE is still three notches above junk, with a Baa1 rating from Moody’s Investors Service, and an equivalent BBB+ from S&P Global Ratings and Fitch Ratings. All carry a stable outlook.

Yields on the company’s $1.95 billion of 3.37 percent bonds due in 2025 have climbed above 5.6 percent. That’s higher than the yield on a Bloomberg Barclays index of debt rated in the highest speculative-grade tier.

Meanwhile, GE’s only actively traded perpetual preferred stock now yields more than 15 percent, higher than some distressed credits. If the company chooses not to call the security in early 2021, it will convert into a floating-rate obligation that GE need never refinance.

--With assistance from Thomas Black.

To contact the reporter on this story: Molly Smith in New York at msmith604@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins, Dawn McCarty

©2018 Bloomberg L.P.