GE Shares Still Don’t Sufficiently Reflect Facts, JPMorgan Says

GE Shares Still Don’t Sufficiently Reflect Facts, JPMorgan Says

(Bloomberg) -- General Electric Co. plunged toward its recession-era low and the company’s bonds fell sharply after an influential analyst slashed his price target.

JPMorgan Chase & Co. analyst Steve Tusa cut his view on the shares 40 percent to $6, the lowest on Wall Street, citing rising liabilities, a weakening cash-flow outlook and poor third-quarter results on “almost all fronts.” He also pointed to deteriorating results at GE’s troubled power division and financial business.

“While the stock is down about 70 percent from the peak of $30, this move still does not sufficiently reflect the fundamental facts,” Tusa said in a report to clients. The company’s latest regulatory filing suggested rising indebtedness, he added, noting about $100 billion in net liabilities.

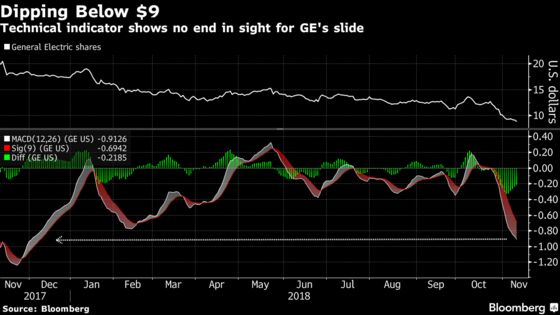

The pessimistic view from Tusa, who has been prescient in predicting GE’s collapse, fueled a steep share decline Friday for a company that has already shed $200 billion in market value since the end of 2016. GE is grappling with one of the deepest slumps in its 126-year history amid weak demand for gas turbines, federal accounting investigations and heavy debt.

The shares tumbled 7.9 percent to $8.38 at 2 p.m. in New York after declining to as little as $8.15, the lowest intraday price since March 2009. That was the same month GE fell to $6.66, the stock’s bottom during the global financial crisis.

GE notes with a 2.342 percent coupon maturing in 2020 and issued by GE Capital International Funding Co., sold off relative to benchmarks to the weakest level since the debt was issued in 2016. Risk premiums on the securities jumped 0.32 percentage point to 1.48 percentage points.

GE Response

The Boston-based manufacturer said it was taking steps to shore up its business. GE has been streamlining its portfolio to focus on power equipment, jet engines and renewable energy.

“GE is a fundamentally strong company with a sound liquidity position,” the company said by email. “We are taking aggressive action to strengthen our balance sheet through accelerated deleveraging and position our businesses for success.”

The company announced the surprise appointment of Larry Culp as chief executive officer in October, replacing John Flannery after just 14 months. Culp must still face up to a weakened outlook for earnings per share, Tusa said.

“We are skeptical around calls for a bottom until management resets EPS expectations that are closer to free cash flow, something we believe they haven’t done for almost 20 years,”’ he said.

Cutting Estimates

Tusa cut his estimate of GE’s 2019 earnings by more than half to 35 cents a share. That’s well below the 86-cent average of analyst estimates compiled by Bloomberg. For 2020, he predicts a profit of 41 cents, compared with the 97-cent average.

GE’s third-quarter earnings, reported last week, missed analysts’ estimates. The company chopped its quarterly dividend to a penny a share from 12 cents. It also revealed a probe into its accounting by the U.S. Justice Department as well as an expanded investigation by the Securities and Exchange Commission.

Tusa warned of a potential “tipping point” for leverage at GE Capital, the company’s financial arm. Considering GE’s expected free cash flow generation and net proceeds from remaining asset sales through 2020, there remains a gap of about $66 billion needed to get the company back to a normal leverage level, he estimated.

Financial Risk

The third-quarter report was the first since Culp took the reins. The filing and comments by executives changed in important ways compared with the previous quarter, Tusa said.

“Most notably, the 10-Q did not show references to $15 billion of cash on the balance sheet by year-end or to $25 billion in industrial debt reduction,” Tusa said.

In another contrast, there was no specific reference to generating $25 billion by reducing the assets at GE Capital. That stoked concern that the unit’s asset value was overstated, said Tusa, who warned earlier this year of underappreciated risk in the finance business. GE Capital is now losing about $1.5 billion annually, with a cash burn of $3 billion, he said.

Tusa’s concerns were echoed by Bloomberg Intelligence analyst Joel Levington, who said the filings contained comments about “on- and off-balance-sheet liabilities, contingencies, lawsuits and liquidity items, which, taken together, reinforce our concerns about GE’s credit risk.”

--With assistance from Sophie Caronello and Natasha Rausch.

To contact the reporters on this story: Esha Dey in New York at edey@bloomberg.net;Joshua Fineman in New York at jfineman@bloomberg.net

To contact the editors responsible for this story: Brendan Case at bcase4@bloomberg.net, ;Catherine Larkin at clarkin4@bloomberg.net, Tony Robinson

©2018 Bloomberg L.P.