GE’s Return to Credibility Advances a Step

GE’s Return to Credibility Advances a Step

(Bloomberg Opinion) -- When it comes to General Electric Co. and its mammoth turnaround, I've long felt that a recovery in its bedrock business and financials won't mean as much without a corresponding correction to the misguided priorities and cultural arrogance that led to its difficulties in the first place. So it’s good to see the company making some progress in that area.

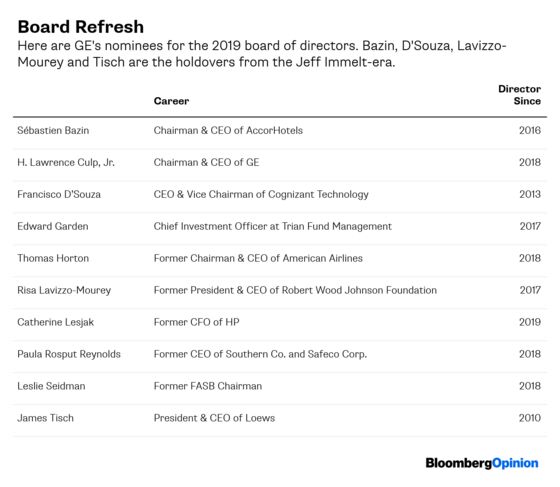

GE released its preliminary proxy filing late Friday and said its two longest-tenured directors – former ConocoPhillips CEO Jim Mulva and former Thomson Reuters Corp. deputy chairman Geoff Beattie – would retire. That leaves GE with only four directors appointed by former CEO Jeff Immelt and a total slate of 10 nominees, down from a board of 18 when Immelt retired. GE expects to continue to target 12 total directors, but it’s seeking permission from shareholders to change its articles of incorporation to lower the minimum board size to seven.

The rejiggering of the board comes amid CEO Larry Culp’s aggressive push to stabilize GE's struggling power unit and raise cash by slashing the once-sacred dividend and accelerating divestiture plans. His predecessor, John Flannery, had started the brush-clearing a year ago, but as was typical with his brief tenure, he failed to go far enough, walking a tenuous balance between respect for GE’s legacy and a need to demonstrate accountability. Culp isn’t playing those games.

I’ve been frustrated at times at what seems like a step backward for every step forward Culp takes in overhauling GE’s culture. But it’s clear he knows there needs to be change, and he’s trying. What’s perhaps more encouraging than the literal remodeling of the board are GE’s efforts to be rigorous and transparent about how it evaluates directors.

I was particularly struck by additional detail on the review of directors’ effectiveness and new language that called for ensuring a board “with high personal integrity and character” and “diversity of thought.” And while GE recommends investors vote against a proposal to separate the CEO and chairman jobs, the company ever so slightly changed its defense of the leadership structure, emphasizing a desire for Culp to bear responsibility for his turnaround strategy and pointing to Flannery's ouster as evidence that the reconstituted board isn't afraid to do its job. GE continues to evaluate the appropriateness of this leadership structure. Culp was briefly lead director last year and was succeeded in that role by former American Airlines CEO Tom Horton upon his appointment as CEO.

Culp’s attempt to bolster the board’s accountability complements GE’s December announcement that it would consider replacing KPMG as its auditor. A key test of GE’s pivot to transparency and accountability will come later this week as the company delivers its much-anticipated outlook for 2019. Cutting down the number of adjustments in its earnings numbers – particularly the impact from restructuring – would send a strong message, as would providing cash-flow details on a per-unit basis.

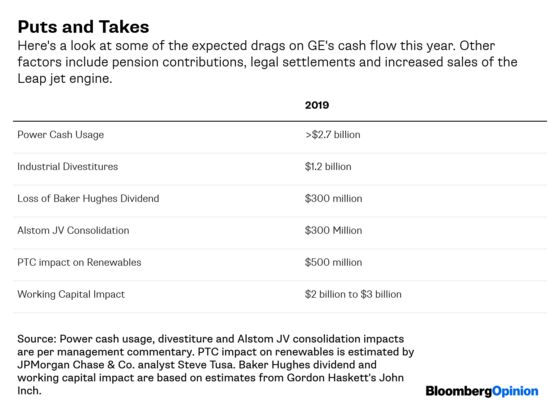

We already know that cash flow for the industrial businesses will be negative in 2019 amid ongoing challenges in the power division and the unwinding of GE Capital support. Another factor is GE’s renewables business, which will be under pressure cash-wise. The implication that renewables made up a meaningful chunk of the $4.5 billion in industrial free cash flow that GE generated in 2018 suggests that the rock-star aviation division may not generate as much cash as previously thought. How forthright GE is about the state of all its businesses and the timeline for a recovery will say a lot.

This is before taking into account the prospect of increased investments for a potential Boeing Co. middle-market aircraft. The fate of that project remains a question mark and it arguably became even more uncertain after the second crash of a Boeing 737 MAX jet in five months.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.