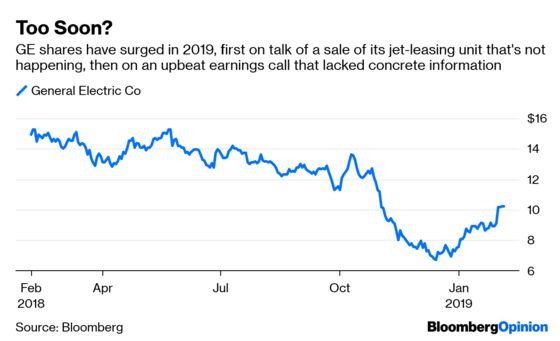

(Bloomberg Opinion) -- General Electric Co.’s $57 million jobs penalty in France is the latest reminder that turning around its struggling power unit will be neither quick nor cheap.

The beleaguered industrial conglomerate will have to pay France 50 million euros ($57 million) after falling short on hiring commitments it made to help secure regulatory approval of its $10 billion purchase of Alstom SA’s energy asset in 2015. It pledged to create 1,000 jobs, but so far has added a net of just 25 positions over the past three years. GE is investing in its renewable-energy operations in France, but its failure to hit this jobs target isn’t surprising. The Alstom deal ballooned GE’s gas turbine operations just as demand was starting to falter, forcing the company to spend billions to rein in an overabundance of capacity. “We were late to embrace the realities of the secular and cyclical pressures in the business,” CEO Larry Culp said on the company’s latest earnings call last week. “We have to resize our cost structure, our capital expenses, and our supply chains to this new reality now.”

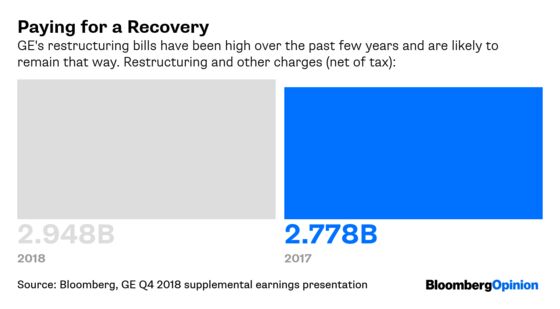

GE’s industrial cash flow is likely to decline significantly in 2019 — perhaps even dipping into negative territory — after taking into account the impact from divestitures of $20 billion in industrial assets, the expected ongoing wind-down of its stake in Baker Hughes, and an initial public offering of its health-care business. The prospect of a cash burn at GE Capital darkens the picture further. Beyond that, it seems likely that GE will need aggressive restructuring over multiple years to get its power unit functioning at a more sustainable capacity. The agreement with the French government reflects one of GE’s biggest hurdles on this front: It’s just not that easy to close large factories and fire loads of people, especially in Europe. That will likely temper any cash-flow recovery in the power unit, which reported a $2.7 billion outflow last year.

GE’s agreement with France is a necessary step in its attempt to move on from the disastrous Alstom deal that drove the preponderance of its $22 billion goodwill write-down last year. It’s tempting to view this kind of incremental progress as a turning point, but GE still has a very long way to go.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.