GE Turnaround Inches Along With Forecast Boost as Max Risk Looms

General Electric gained after raising its outlook for the year as the long-suffering power division showed signs of improvement.

(Bloomberg) -- General Electric Co. raised its forecast amid signs of improvement in the long-suffering power business, even as issues in the jet-engine division posed a new threat to Chief Executive Officer Larry Culp’s turnaround plan.

The industrial businesses will generate as much as $1 billion in cash this year, up from the previous range of no more than zero, GE said Wednesday as it reported second-quarter earnings. The company adopted its more upbeat outlook despite headwinds from the grounding of Boeing Co.’s 737 Max.

“It is a sign of progress, a sign of stability,” Culp said in an interview, before sounding a note of caution. “We’re talking about a free cash outlook that could be negative. It’s still a little hard for us to jump up and down.”

The CEO’s modest optimism underscored the challenges still arrayed against GE, which has struggled with heavy debt and flagging demand for gas turbines. Since taking the helm in October, Culp has sought to cut costs, boost cash and regain investor support amid one of the worst slumps in GE’s 127-year history. On Wednesday, he shook up the executive ranks by announcing the departure of Chief Financial Officer Jamie Miller.

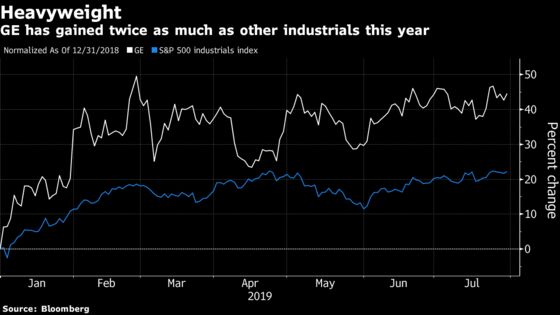

Investors needed time to digest the changes, bidding the shares up as much as 6.2% ahead of regular trading before a selloff dragged them down as much as 4.5%. GE was little changed at $10.52 at 2:47 p.m. in New York. A rout in 2017 and 2018 wiped out more than $200 billion in GE’s market value.

In the second quarter of this year, adjusted profit fell to 17 cents a share, topping the 12-cent average of analyst estimates compiled by Bloomberg. Free cash flow from the manufacturing units was minus $1 billion, at the high end of GE’s previous expectations.

“Things are turning,” said Nicholas Heymann, an analyst with William Blair & Co. While GE still has more work to do, especially in nursing the power business back to health, the latest moves suggest Culp is “comfortable in his own skin.”

Culp said GE is now “stable enough” to handle a C-suite shakeup. GE has started a search to replace Miller, who will stay on for now to smooth the changeover.

‘Iffy’ Operations

Orders in the gas-power operation climbed 27%, GE said in a statement. Still, sales for all of GE Power, which has struggled through a downturn in the gas-turbine market, fell 25% and profit plunged 71%.

The results contributed to a 26% decline in operating earnings from GE’s manufacturing units.

“The underlying operations were iffy,” said Scott Davis, an analyst with Melius Research. “It’s a turnaround, so maybe we shouldn’t have expected much, but by the same notion, I thought we’d see some operational improvements on the margin line.”

737 Max

GE flagged the 737 Max crisis as an ongoing issue. Boeing’s top-selling jet has been grounded since March after a pair of crashes killed 346 people. GE, through a joint venture with Safran SA, makes the plane’s engines.

The production backup will generate a cash headwind of $400 million a quarter as long as the plane remains out of service, Culp said.

Second-quarter profit declined 6.1% in GE Aviation, as the company also faced higher costs related to its effort to certify a new engine for Boeing’s 777X. The planemaker said last week that the first flight of that wide-body jet would be pushed to next year due to issues with the engine.

GE’s adjusted profit this year will be 55 cents to 65 cents a share, up a nickel from the prior range, the company said. The outlook adjustment was due in part to “improvements at power, lower restructuring and interest, higher earnings and better visibility at the half,” Culp said in the statement.

The forecast failed to impress Steve Tusa, an analyst at JPMorgan Chase & Co. who earned a reputation for prescience in recent years after emerging as the biggest GE bear on Wall Street. He questioned whether GE’s performance merited the improved outlook for this year, and recommended selling the shares into any gains.

“The underlying core fundamentals are actually a bit worse,” he said in a note to clients.

To contact the reporter on this story: Richard Clough in New York at rclough9@bloomberg.net

To contact the editors responsible for this story: Brendan Case at bcase4@bloomberg.net, Tony Robinson

©2019 Bloomberg L.P.