(Bloomberg Opinion) -- Well, that isn’t a good sign.

General Electric Co. said Friday it's postponing the release of its third-quarter earnings by a few days to give new CEO Larry Culp more time to complete "initial business reviews and site visits." Culp, the former CEO of Danaher Corp., was installed in the top job last week following the surprise ouster of John Flannery. I struggle to understand why Culp needs to make site visits to ably report numbers for a quarter that ended before he became CEO unless there are more troubling issues at play here.

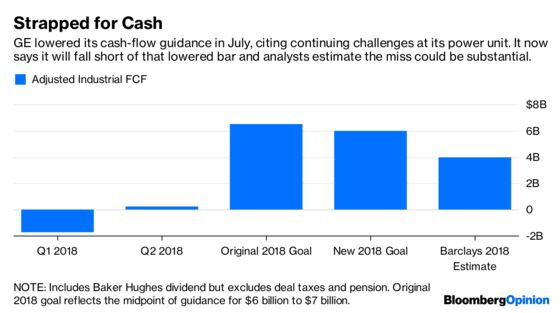

GE tried to push a fair amount of bad news out the door with Flannery: In conjunction with the CEO change, the company warned it would miss its 2018 earnings and cash-flow guidance and would have to write down nearly all of the $23 billion in goodwill at its troubled power unit. But GE offered scant details about those massive financial blows. That fueled fears that the power problems ran deep and spurred fresh worries about GE's accounting and internal controls. As recently as the second quarter, GE conducted an impairment test on the goodwill it's now writing down and didn't find a problem. The delay of the earnings report will only deepen those concerns.

GE's earnings update will now come out on Tuesday, Oct. 30, compared with a previously scheduled date of Thursday, Oct. 25, that was in itself an anomaly (GE has traditionally released results on the third Friday of the month). Here's what to watch for when the company does finally report:

- EARNINGS RESET: We know GE will miss its guidance, but the magnitude of the shortfall could be meaningful. The average analyst estimate pegs GE's 2018 adjusted earnings per share at about 90 cents (compared with guidance of $1 to $1.07), while Barclays Plc analyst Julian Mitchell says GE's industrial businesses could bring in just $4 billion of free cash flow (compared with GE's $6 billion outlook as of July). It's also possible Culp may use the cut to do a deeper cleanup of GE's reporting metrics, which are still too heavily adjusted and don’t reflect the actual state of the company's business.

- DIVIDEND CUT: Flannery had said GE would re-evaluate its dividend once it completes a planned separation of its health-care business, and that the overall payout would likely be lower. GE's earnings shortfall and looming credit-rating cuts likely speed up that timeline and will force Culp to take a much bigger ax to the dividend. UBS Group AG analyst Steven Winoker says at least a 90 percent cut to the current 48-cent annual payout may be warranted.

- EQUITY INJECTION: A dividend cut alone isn’t enough to shore up GE's balance sheet, particularly amid questions of whether the industrial parent will need to inject more capital into its finance arm. GE disclosed a $15 billion reserve shortfall at a legacy insurance business in January and said in June it will make a $3 billion capital contribution to GE Capital, after previously saying it wouldn't need to do so. An equity raise could give GE some breathing room and would allow Culp to contemplate changes to the company's breakup plan, which currently entails spinning off health care, shrinking GE Capital and selling its stake in the Baker Hughes energy business.

- RETHINKING GE's RETHINK: I've long argued that GE needs to be more focused, but I've been wary of the dynamic that's created by GE's breakup plan. The health-care business is stable and cash-generative, and parting with it will make GE dependent on power and aviation divisions that are more susceptible to economic downturns. One alternative is to keep the core imaging business and instead sell the life-sciences arm, a fast-growing unit that could fetch as much as $20 billion. Recall that Culp's old company Danaher reportedly expressed interest in GE's life-sciences business. A sale of jet-lessor GECAS is another option that should be explored.

- POWER TECHNOLOGY PROBLEMS: GE shares plunged in September after disclosing an oxidation issue with its flagship H-frame gas turbines. While the company has said the problem was overblown and it’s already rolling out a fix, JPMorgan Chase & Co. analyst Steve Tusa this week laid out a number of other reported shortfalls in product quality. All new industrial equipment will have teething issues, but regardless of how serious these problems actually end up being, they cost money and time to fix, both of which GE Power has very little of.

I appreciate that GE is a complicated company with complicated problems, but part of the run-up in its stock price following Culp's appointment is based on a perception that he's already well-versed on GE's challenges after serving on the board for the past six months and will be able to hit the ground running. I've been skeptical of that narrative, given how much worse off GE is than Danaher ever was, but more importantly, how endemic and interconnected some of the company's challenges are.

The earnings report delay should be a reminder that Culp's got a long, tough road ahead of him.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.