GE Breakup Spurs Questions About Conglomerate Model’s Future

General Electric Co.’s breakup raises the question of how many remaining conglomerates will be able to avoid the same fate.

(Bloomberg) -- General Electric Co.’s breakup raises the question of how many remaining conglomerates will be able to avoid the same fate.

GE, an iconic business built over decades by executives such as Jack Welch, is set to be dismantled in Chief Executive Officer Larry Culp’s most dramatic move. The debate over the conglomerate structure casts a spotlight on businesses such as Warren Buffett’s Berkshire Hathaway Inc., which has spent years arguing why its particular brand of conglomerate works.

Conglomerates, once considered a way to bring multiple companies together to reap the benefits of synergies, size and breadth, have fallen out of favor. Buffett himself has conceded that conglomerates have “earned their terrible reputation” over the years, and GE’s Culp said Tuesday that focus is more beneficial than the often “illusory” benefit of synergies. The days of the traditional industrial conglomerate could be numbered even as technology behemoths increasingly adopt a somewhat similar complex model.

“I don’t know how many fundamentally industrial companies are going to continue to use this particular kind of structure,” said Kathryn Rudie Harrigan, Columbia Business School’s Henry R. Kravis professor of business leadership. “Because it sort of begs the question of what, if anything, is added by putting them all in the same corporate family.”

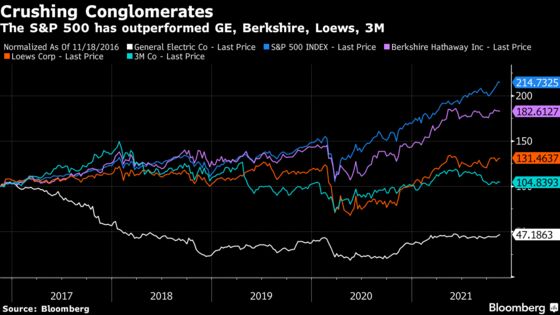

Over the past five years, investors have been less enthusiastic about some conglomerates than the broader market. GE, notably, has lost 51% in that timespan, while Berkshire has risen 90%, holding company Loews Corp. has gained 34% and industrial and consumer-goods giant 3M Co. has increased just 6.4%. The S&P 500, meanwhile, has soared 117%.

Some breakups have benefited the remaining businesses. Famously, Culp’s alma mater, Danaher Corp., has split off businesses in recent years. Its stock has outperformed the broader market over the past five years, climbing 273%.

“We believe the pendulum is still swinging towards the ‘urge to demerge’ trend,” RBC Capital Markets’ Deane Dray said in a note to clients Tuesday. “GE’s announcement today could embolden the boards of several other multi-industry companies to move ahead on more aggressive portfolio simplification moves, including Emerson, Roper Technologies and 3M.”

GE rose 2.7% Tuesday after the breakup plans were announced. Its shares gained 29% this year through Tuesday.

Some conglomerate heads have staunchly defended their companies’ complex setups. Buffett wrote in an annual letter earlier this year that conglomerates have received a bad reputation because they’ve overpaid for mediocre businesses, with some businesses even using “imaginative” accounting maneuvers. Still, Berkshire’s 91-year-old CEO argued that his Omaha, Nebraska-based business differs from the “prototype” conglomerate, partly because it controls some businesses and owns non-controlling stakes in others.

Loews CEO James Tisch, who has called his company -- which owns hotels, an insurer and even some energy operations -- “unabashedly a conglomerate,” has argued that he thinks the business can create the most value by being in multiple industries.

Berkshire, for its part, has been somewhat insulated from activist calls for a breakup partly because Buffett remains at the helm. But he disclosed earlier this year that his successor would likely be a key deputy, Greg Abel, if and when he steps down -- a reminder to investors that he’ll one day have to pass the reins. Part of the key to Berkshire’s ability to remain a conglomerate has been its decentralized management style, said David Kass of the University of Maryland.

“The managers at Berkshire have almost complete independence in running their businesses. They don’t have to go through the red tape of corporate headquarters as GE has and most companies do,” said Kass, a professor of finance at the university’s Robert H. Smith School of Business. “As long as Buffett is there, the structure will stay the same. And after Warren Buffett is no longer there, it will probably be Greg Abel running the company, they’ve already pledged to maintain the culture.”

Many companies have naturally drifted toward wanting to integrate operations as they seek to gain scale and efficiency, said Omar Aguilar, a senior managing director and co-leader of the enterprise transformation practice at FTI Consulting Inc. But one of the keys to a conglomerate’s survival is whether they can keep increasing their earnings, he said.

“If they continue growing,” Aguilar said, “I think they’re OK.”

Even if some industrial conglomerates continue to break up, there’s also a trend of tech giants expanding into various but distinct industries, and thus developing a conglomerate-like model, said Harrigan of Columbia University. Amazon.com Inc., for example, has moved beyond e-commerce into health care and grocery stores. The company benefits because it’s often targeting the same customer in its variety of businesses, she said.

“For internet-enabled companies, those that are successful will probably end up becoming very complex by diversification,” she said. “They can get terrific customer-based synergies.”

©2021 Bloomberg L.P.