Frontier Creditors Prod Telecom to Overhaul Its Debt

Frontier Creditors Prod Telecom to Overhaul Its Debt

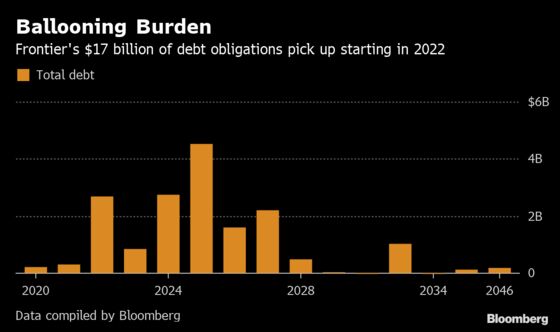

(Bloomberg) -- Talks are heating up between Frontier Communications Corp. and its creditors over a potential restructuring of its $17 billion debt load.

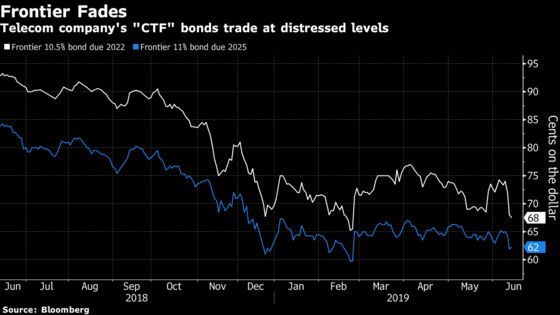

Advisers for three groups of creditors have held informal discussions with Frontier ahead of $2.7 billion of debt maturities in 2022, according to people with knowledge of the matter. Those notes trade at deeply distressed levels, and the company has signaled it may be ready for a more official process by adding board members with turnaround experience.

No formal proposals have been submitted so far, and Frontier hasn’t indicated what it plans to do yet, said the people, who asked not to be identified because the talks are private.

A group including Elliott Management Corp., Apollo Global Management LLC, Franklin Resources Inc. and Capital Group Cos. had proposed swapping their unsecured debt into new secured notes in an out-of-court transaction, with some members also favoring a Chapter 11 bankruptcy filing, the people said. The other creditor groups prefer a bankruptcy filing, in part to avoid seeing their holdings pushed down in priority through a debt swap, according to the people.

The group including Elliott, Apollo, Franklin and Capital Group holds about 60% of so-called CTF unsecured bonds maturing in 2022 and 2025, according to some of the people. Some creditors in that group are believed by market participants to have sold credit-default swaps insuring against a Frontier default. That would skew their interests against a Chapter 11 filing. A second group of creditors holds “legacy,” or non-CTF, bonds, and a third group of creditors owns a mix of CTF and legacy bonds, the people said.

A spokesman for Norwalk, Connecticut-based Frontier declined to comment. Representatives for Elliott, Apollo and Franklin declined to comment, while a spokesman for Capital Group didn’t immediately respond to a request for comment.

Frontier shares fell as much as 13%, and traded down 5 cents at $1.47 a share as of 1:27 p.m. in New York. They’re down more than 37% this year.

Still Time

Frontier still has time to negotiate with creditors and it also will benefit from a recent $1.4 billion asset sale, which gives it cash to address small short-term maturities. The company has publicly said that it will be able to stabilize its wireline business through cost cutting while retaining customers in its broadband internet unit. It also generates positive free cash flow.

The CTF notes are trading at levels indicating a higher likelihood of default, with the 2022 securities yielding about 26% on Friday. Credit-default swaps are pricing in a 90% chance of default within five years, according to data from CMA.

Frontier fed speculation that it may be willing to consider reworking its debt or a Chapter 11 filing after the addition of new directors with substantial restructuring experience, including Mohsin Y. Meghji, founder of M-III Partners, who currently serves as chief restructuring officer of Sears Holdings Corp. Those directors joined the board after Robert A. Schriesheim was added in December. Schriesheim’s biography cites his former role in raising capital for Sears and current post on the board of Houlihan Lokey Inc., which specializes in turnarounds.

Revenue and profit are dropping in Frontier’s traditional wireline telephone business as more customers defect to wireless services, and its broadband internet unit faces steep competition from cable companies. Frontier ranks as the biggest issuer among deeply distressed-debt borrowers -- those with yields topping 20% -- despite efforts by Chief Executive Officer Dan McCarthy to turn around the business.

The CTF moniker stems from bonds Frontier issued after its $10.5 billion purchase of California, Texas and Florida systems from Verizon Communications Inc. in a deal that McCarthy said in 2015 would boost revenue and free cash flow, as well as help retain customers. Instead the CTF bonds, which make up the bulk of Frontier’s $2.7 billion 2022 maturity wall, pushed up leverage and failed to halt the company’s decline.

“They’ve been lucky enough to put off the day of reckoning as a result of the asset sale, but they haven’t been able to fix the business, which is still extremely over-leveraged,” said George Schultze, founder and CEO of Schultze Asset Management in New York. He has a short position on Frontier stock.

Frontier is getting advice from Kirkland & Ellis and Evercore, according to the people. The CTF bondholder group, which includes its 10.5% notes due 2022 and 11% notes due 2025, are working with Akin Gump and Ducera. A crossover group holding legacy and CTF bonds has tapped Milbank and PJT Partners, and a group holding mostly legacy notes, which includes GoldenTree Asset Management LP, is getting advice from Willkie Farr & Gallagher and Houlihan Lokey, the people said.

Representatives for those firms declined to comment or didn’t respond to messages.

Frontier’s board is wary of a restructuring transaction that might trigger litigation from creditors, such as a debt swap that leaves certain holders out, the people said. Distressed investor Jason Mudrick said on Bloomberg TV that Frontier had been exploring a transaction that would have rolled up the nearest maturities into the senior paper, but decided to do a more comprehensive restructuring because of what happened to Windstream Holdings Inc.

Its wireline peer collapsed into bankruptcy this year after losing a litigation fight against Aurelius Capital Management LP tied to a spinoff and subsequent bond swaps. Mudrick has a short position on Frontier.

A key question facing creditors is how much capacity Frontier has to issue new secured debt, which could be used to swap and extend existing unsecured debt, a transaction that could shore up its solvency. Under the investment grade-style bond covenants governing its legacy bonds, Frontier may have as much as $12 billion of secured debt capacity, according to Covenant Review.

S&P Global Ratings, which rates Frontier at CCC+ with a negative outlook, said the company’s recent asset sale is positive but doesn’t really change the overall picture.

“The longer-term trajectory of the business would suggest that eventually it would have to file for Chapter 11, but they could do a series of debt exchanges in the near term,” S&P analyst Allyn Arden said.

--With assistance from Claire Boston.

To contact the reporters on this story: Allison McNeely in New York at amcneely@bloomberg.net;Katherine Doherty in New York at kdoherty23@bloomberg.net

To contact the editors responsible for this story: Rick Green at rgreen18@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.