The Long-Anticipated New York Area Housing Slump Has Officially Arrived

Stringent tax laws and higher rates cause slump in sale of the houses in New York.

(Bloomberg) -- The tales of housing malaise stretch across metro New York.

A Long Island home sat idle on the market until both its price and taxes were slashed. Buyers in Connecticut are asking to rent houses before purchasing them. Hoboken brokers lament their slow business.

Now, the growing consensus is prices are headed in one direction: down.

From the high-rises of Manhattan to the city’s manicured suburbs, homebuyers are pulling back as they reel from a triple whammy of costly hits. First, it was years of unrelenting price gains, followed by a federal cap on state and local property-tax deductions. Then came a surge in mortgage rates, making purchases even more expensive.

“Brokers ask me, ‘When is it going to get better?”’ said Greg Heym, chief economist of Terra Holdings, which owns brokerages Halstead and Brown Harris Stevens. “‘Better’ for this market, in this area, is lower prices.”

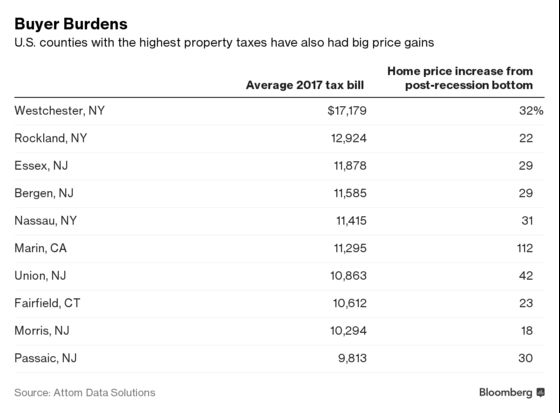

Home sales are slowing across the U.S. after a multiyear boom marked by frenzied deals, fueled by historically low borrowing costs. So far, values in most of the country haven’t fallen -- but the rate of appreciation is slipping, particularly in the New York area. Prices in the 12 counties that include and surround New York City rose 4 percent in the third quarter from a year earlier, compared with a 4.8 price increase across the U.S., according to Attom Data Solutions.

New York may be worse off because of the new tax law, which sets a $10,000 limit on deductions for state and local levies, hitting the tri-state region particularly hard. Of the 10 U.S. counties with the highest tax burden, nine are in New York, New Jersey or Connecticut, Attom data show.

“Housing in general has quite a few headwinds right now, but the New York area is feeling the brunt of the headwinds,” said Daren Blomquist, Attom’s senior vice president. “Counties with the slowest appreciation are the ones that tend to have the highest prices and the highest taxes.”

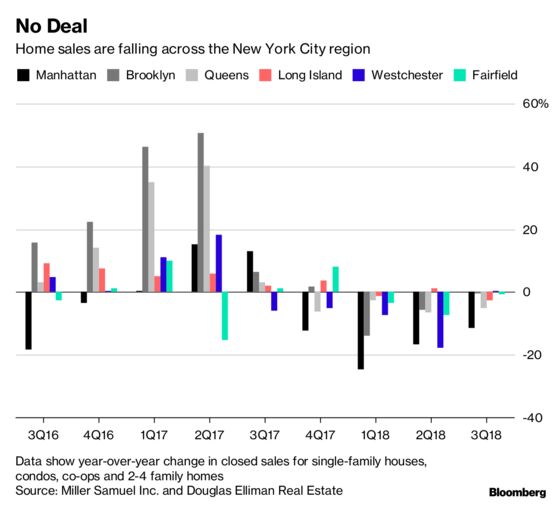

In New York’s affluent Westchester County, No. 1 on Attom’s list of high-tax areas, single-family home sales fell for a fifth straight quarter in the three months through September, according to appraiser Miller Samuel Inc. and brokerage Douglas Elliman Estate. Purchases slumped for two of the last three quarters in the Long Island suburbs, which include Nassau County, with the fifth-highest tax burden in the country.

New Jersey’s Bergen County -- No. 4 -- had a 6 percent drop in third-quarter sales contracts from a year earlier, according to Otteau Group Inc., which tracks real estate transactions and prices.

Tax Appeal

Buyers, who once accepted high property taxes as the price of living in suburbs with great school districts, are starting to push back.

“One of the first questions buyers ask is, ‘Have the owners grieved their taxes?”’ said Matthew Lenner, a broker with Keller Williams in Long Island, referring to a formal appeals process with the county’s assessment office.

Last month, Lenner relisted a four-bedroom home in Plainview that had lingered on the market, with a different agency, since June 2017. He cut the price of the 10-year-old house to $899,999 from its original $969,000, and worked with the owners to file an appeal to the property’s $28,500 annual tax bill.

They succeeded. The listing notes that the tax will be reduced by 20 percent starting next school year, and Lenner said the home is drawing more interest.

In New Jersey, many buyers appeared to brush off the new tax law, and sales remained strong until September, when mortgage rates shot higher, said Jeffrey Otteau, president of the valuation company that bears his name. The decline in purchasing power means prices will inevitably have to adjust, he said.

“Sellers have gotten greedy,” he said. “It’s easier to say ‘blame tax reform’ than to say ‘we need to take an honest look at the price you expect to get for your house.’ Sellers don’t get it.”

Buyers, finding themselves with the upper hand, are getting creative with deals. John Engel, a broker with Halstead in Connecticut’s Fairfield County, said house hunters are asking to ease into their purchase by renting their future home first. He had three separate clients in New Canaan this year who set up lease arrangements with sellers, offering a 10 percent down payment on a home, with a promise to eventually buy it or forfeit the cash.

“It’s not a market without risk,” Engel said. “With the current volatility, buyers want to, No. 1, get some comfort with the market, and No. 2, get some comfort with the neighborhood.”

Closed deals for single-family homes in New Canaan were down 15 percent in the year through Nov. 30, according to a Halstead report.

‘So Slow’

Closer to Manhattan, the slowdown is palpable, said Sharon Shahinian, a Halstead broker in Hoboken, the New Jersey town across the Hudson River that’s popular with millennials and young families.

“All the agents are saying to each other, ‘Are you busy?’” Shahinian said. “Someone will say, ‘Oh my God, it’s so slow, and someone else will say, ‘I’m glad it’s not just me.”

The buyers who are around are finding deals. In August, Shahinian listed a two-bedroom condo at Hoboken’s Maxwell Place for $1.25 million, and found a possible taker for the seventh-floor unit pretty quickly. But then a similarly sized penthouse at the building came on the market for $1.275 million. The buyer purchased that unit instead -- at nearly the same price as the lower-floor condo. Shahinian’s listing ultimately sold for $1.23 million.

“It’s a great time for buyers, so it’s not all doom and gloom,” Shahinian said. “But you have to manage sellers’ expectations that what they could have gotten two years ago, a year and a half ago, they can’t get now.”

To contact the reporter on this story: Oshrat Carmiel in New York at ocarmiel1@bloomberg.net

To contact the editors responsible for this story: Debarati Roy at droy5@bloomberg.net, Kara Wetzel, Christine Maurus

©2018 Bloomberg L.P.