Blown-Up Trades at Heart of French Banks Erase $1.5 Billion

French Banks’ Love for Complex Products Blows Up in Virus Mayhem

(Bloomberg) -- A key money maker for French investment banks has blown up just as they prepare to deal with the fallout from the coronavirus crisis.

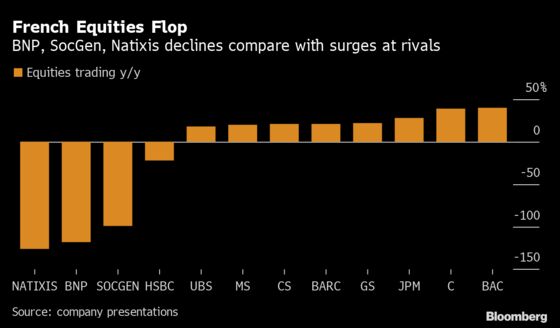

BNP Paribas SA, Societe Generale SA and Natixis SA all saw revenue from equities trading wiped out in the first quarter by heavy losses on complex derivatives, an area of traditional strength. Most of their rivals navigated the market panic more successfully in the wake of the outbreak, posting double-digits gains from the same business.

The result in Paris was a slump of 1.4 billion euros ($1.5 billion) in equities revenue that overshadowed a strong performance in fixed-income trading. At a time when lenders have to set aside billions to prepare for defaults by borrowers ruined in the unprecedented lockdowns, at least one of the French firms indicated it will take a closer look at whether the derivatives business is still worth the risk.

“We can’t say in the medium run we can be happy with what we generated by equity derivatives,” Francois Riahi, the chief executive officer of Natixis, said on a call after being asked whether the bank would consider exiting the business. “But we aren’t going to make decisions based on just this. We are going to review what we want to do and don’t want to do in the future.”

One of the reasons for French banks’ equities-trading disaster is that they pursue structured products -- multi-layered securities that get increasingly difficult to manage when markets fluctuate -- over other equity-derivatives businesses that saw record volumes in the first quarter. Their traders were battered even further when corporations began canceling their dividends, key components in many of their complicated deals.

Equities-trading revenue at Natixis tumbled 126%, the smallest of the three banks said late Wednesday. BNP Paribas slumped to its worst result in equities since at least 2014 and SocGen saw the poorest performance since the 2008 financial crisis.

The results contrast with gains across Wall Street banks, led by Bank of America Corp. Equity-derivative traders at JPMorgan Chase & Co. brought in about $1.5 billion of revenue, at least twice what they normally do, Bloomberg reported.

French banks missed out on these gains because they are relatively small players in businesses such as flow-equity derivatives, which include options linked to the S&P 500. Demand for these products surged to records in the chaotic first quarter as investors rushed to protect their holdings and wager on soaring market volatility.

Spokeswomen for BNP Paribas and SocGen in London declined to comment. A spokesman for Natixis in Paris also didn’t comment.

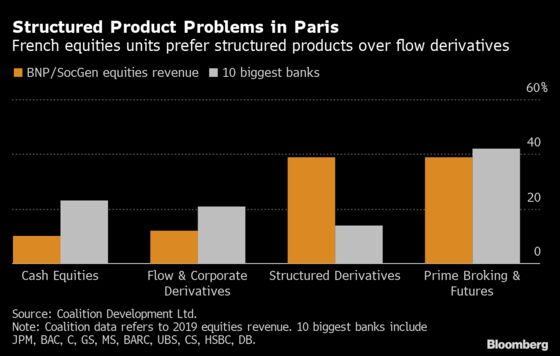

BNP Paribas and SocGen got just 12% of their combined stock revenue in 2019 from flow and corporate equity derivatives, little more than half of what their 10 biggest rivals got, according to data from Coalition Development Ltd. By contrast, they got 39% from structured products, almost three times as much as their competitors.

The French banks are among the biggest players in the market for structured products, complex securities that are typically linked to the performance of a stock or an index of shares. A popular example is the autocallable, which pays an attractive coupon as long as the underlying stocks don’t fall below a preset amount.

The products are popular with high net-worth clients and are also sold to retail investors in Japan and South Korea. But their complexity makes them fraught with danger for the banks that arrange them. Natixis lost hundreds of millions of dollars when trades linked to Korean autocallables went awry in late 2018, losses that attracted scrutiny from the European Central Bank.

Banks that arrange structured products enter into a series of offsetting transactions to protect themselves from losses. Yet this becomes increasingly costly when markets become volatile. All three lenders cited hedging costs as a key factor explaining the trading results.

Traders at the French banks typically use derivatives linked to dividends as part of their efforts to hedge, according to Eric Barthe, head of financial engineering at Anova Partners in Zurich. This strategy was upended when corporations began canceling payments to shareholders, some in response to requests from regulators, he said.

“Hedging them is a complex job and can be costly when the quantitative models the banks use fail to predict reality,” said Barthe, who recently analyzed the losses. “What we have seen on dividends this year is typically something most models would not have captured.”

SocGen, BNP Paribas and Natixis lost more than half-a-billion euros combined from the canceling of dividends, accounting for about 40% of the decline in equities-trading revenue from a year ago. On a May 5 call with analysts, BNP Paribas Chief Operating Officer Philippe Bordenave said this was “a very isolated one-off loss.”

‘Brutal Reduction’

“We went through extraordinary dislocations of the market in the second half of March,” SocGen Chief Executive Officer Frederic Oudea said in an interview on Bloomberg TV. There was “this brutal reduction -- sometimes going to zero -- of dividends.”

For the CEOs of all three banks, the losses are an embarrassing setback because they hit a core business that they have defended for a long time. Oudea just restructured the investment bank, emphasizing SocGen’s traditional strength in equities and related derivatives after exiting or refocusing some fixed-income trading and cutting jobs. The firm is now amending its business model and looking to develop products that are less complex and easier to manage, a person familiar with the matter said.

BNP had been burnt by derivatives before, when its traders were flummoxed by sharp market moves in late 2018 and a series of U.S. trades that went awry and lost tens of millions of dollars. CEO Jean-Laurent Bonnafe has since sought to bolster the equities unit, agreeing last year agreed to take over Deutsche Bank AG’s prime brokerage clients to add market share.

At Natixis, the first quarter ended a brief respite for CEO Riahi, who had been trying to draw a line under a series of missteps since taking over in June 2018, including the losses on Korean securities, a liquidity scare at its H2O Asset Management subsidiary and oversight problems.

“The lesson is that there’s always another risk lurking around the corner,” said Benjamin Clerget, a former equity-derivatives trader at SocGen and ex-fund manager at Banco BTG Pactual SA’s hedge-fund arm. “Bank models incorrectly showed there was no risk.”

©2020 Bloomberg L.P.