Forget the President. Senate May Matter More for Markets

Forget the President. Senate Races Could Matter More for Markets

(Bloomberg) -- While many investors are zeroing in on the U.S. presidential election in November, a trickier political equation could be even more important in determining winners and losers in markets: which party controls the Senate.

Many political analysts at this point expect the Democratic Party to remain the majority in the House of Representatives regardless of who wins the presidential race. Control of the Senate is harder to predict. Of the 100 seats, 35 are up for election this year and Republicans will be defending 23 of them -- with their three-seat majority in the balance.

A Senate majority likely brings the power to block or advance the next president’s agenda, making it the “ultimate policy arbiter of 2021,” as Cowen & Co. analyst Chris Krueger puts it.

That was underlined with Friday’s death at 87 of Ruth Bader Ginsburg, the liberal Supreme Court justice, and Senate Majority Leader Mitch McConnell’s promise to hold a vote on a new court pick by President Donald Trump.

And buckle up for a potential nail-biter: Like the presidential race, poll watchers are concerned the makeup of the Senate may not be known for some time after the vote on Nov. 3.

Below are some of the scenarios analysts are dissecting to determine how control of the Senate could have an impact on financial markets.

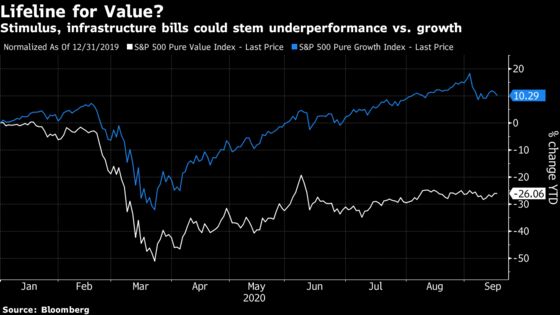

Stimulus, Infrastructure

The elections could break a political logjam that has prevented passage of another fiscal stimulus package to combat the economic effects of the Covid-19 pandemic.

Should Democrats control the White House, House and Senate, analyst Henrietta Treyz of investment adviser Veda Partners envisions a $2 trillion package that would extend additional unemployment payments while also providing aid to schools, state governments, health-care providers and families. It could be coupled with a jobs-creating program targeted at infrastructure, focused on clean energy.

“This will be entirely deficit financed because it will be ‘stimulus,’” she said, “i.e. targeted, temporary and, ideally, timely. No corporate tax increases would be associated with this bill and the goal would be to make it as non-controversial as possible so it could attract five or six Republican votes with the help of former Senator Joe Biden ushering those Republicans over to his side, the way he did with the American Recovery and Reinvestment Act in 2009.”

Greg Boutle, the U.S. head of equity and derivative strategy at BNP Paribas, said during a virtual presentation this week that investors should “focus on whether we get divided or unified government” and that potential higher tax rates following a sweep by the Democratic Party might be offset by fiscal spending. In that case, he said, value stocks tied to the fate of the economy may benefit.

However, if control of Congress and the White House remain split, policy logjams may be here to stay. That could be a threat to markets if January rolls around, unemployment is still elevated and lawmakers are no closer to a deal on stimulus measures.

In a worst-case scenario, investors may get a flash back to the crisis of 2011, in which a split Congress brought the U.S. to the brink of default and the nation lost its AAA credit rating from Standard & Poor’s. The S&P 500 lost almost 19% between early July and early October during the drama of that year.

Taxes

Many investors share a focus on how much of Trump’s tax cuts would remain under a hypothetical Biden administration. Biden said he would raise taxes on those who make more than $400,000 a year and push up the corporate tax rate to 28% from 21%.

The focus may be overblown, for a couple of reasons. For one thing, most of the Democratic challengers to Republican senators are moderates and deficit spending, rather than tax increases, would be a “major pillar” of a potential Biden administration, whether it’s accompanied by a slim majority or a minority in the Senate, Treyz wrote in a note.

“Given that the U.S. is likely to be in a recession and still dealing with fallout from Covid-19, there will not be votes in the Senate to raise taxes on individuals or corporations, even in the event Biden prioritizes a massive $2 trillion infrastructure package,” she said.

Also, tax increases don’t necessarily result in poor stock market performance, according to strategists Keith Lerner and Dylan Kase at SunTrust Advisory Services.

Counter-intuitively, markets on average actually have produced better returns and been more consistently positive in years in which taxes have risen, the SunTrust strategists wrote in a note. Despite relatively high tax rates in the 1950s, the U.S. stock market had its best-performing decade of the past 70 years, they wrote. And while the 2000s have seen the lowest average tax rates of the past 50 years, they have generated the worst stock market returns and economic growth in the modern era. The S&P 500 rose more than 30% in 2013, a year taxes were raised, they point out, and the index declined in 2018 despite Trump’s tax cuts.

Of course, the S&P 500’s 19% rally in 2017 was largely attributed to market optimism that Trump’s tax-cut plan would boost earnings in the following year. But the bottom line is it’s too simplistic to assume higher taxes automatically equate to lower markets, all else being equal.

Filibuster Rules

A Democratic majority theoretically could change the chamber’s filibuster rules, letting senators pass legislation by a simple majority rather than the 60 votes now required to end filibusters.

That would allow initiatives by Biden and other Democrats to go “sailing through both houses,” according to AGF Investments chief U.S. policy strategist Greg Valliere.

The resulting policy effects may be most notable for health-care and energy stocks.

Pharma and Health-Care

The pharmaceutical industry will care more about which party controls the Senate than who wins the White House, according to analysts at Bloomberg Intelligence.

For one thing, a Democrat-controlled Congress that eliminates the filibuster could approve Biden-backed legislation for the federal government to negotiate Medicare drug prices, potentially reducing spending on drugs by $448 billion over 10 years. Top-selling Medicare Part D drugs include Bristol-Myers’ Eliquis and Revlimid and AbbVie’s Humira and Imbruvica, according to BI.

Energy Sector

Energy policy provides one of the starkest contrasts between Trump and Biden. Biden’s platform includes day-one legislation that puts the U.S. on “an irreversible path to achieve economy-wide net-zero emissions no later than 2050,” whereas President Trump is likely to continue policies friendly to the fossil fuel industry.

The implications for the markets are pretty clear, at least at first glance: A Trump win could benefit oil and gas stocks, while a Biden victory could boost shares of clean energy companies. Yet, again, it comes down to the power of moderates. Even if a Biden victory is accompanied by a Democratic majority in the Senate, the moderates may keep his agenda in check and limit efforts to pass “transformative” climate and energy policy, Raymond James analysts led by Tavis McCourt wrote in a late-August note.

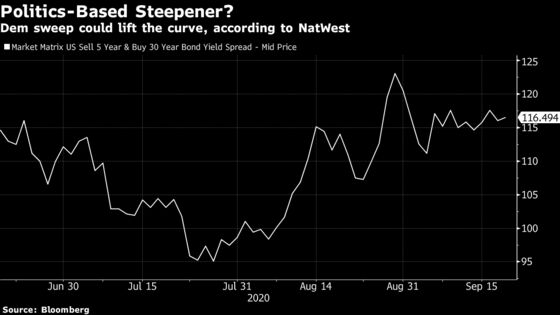

Treasuries, Dollar

Each possible mix of control in the Beltway provides a different cocktail of potential drivers for the Treasury market. Strategists at NatWest Markets laid out the various effects they expect in each scenario and the most likely outcome, to which they still only assign a 40% probability, is a win by Biden and Democratic control of the House and Senate. That, in their view, would lead to a steeper yield curve, higher inflation expectations and a weaker dollar amid increased spending on climate and infrastructure program and the enactment of Biden’s tax plan.

The next most-likely outcome, which NatWest pegs at a 30% chance, is a win by Trump and a split Congress. If the curve steepened in anticipation of a Democratic sweep, that would likely mean a re-flattening and be a positive for the dollar since Trump would be emboldened to continue his trade war and “America First” policies but reduce the chance for further tax cuts. A Biden win and a split Congress -- a 25% probability, according to NatWest -- could also see a corrective curve flattening, the strategists wrote.

Disputed Results

Much like with the presidential race, investors should brace for the possibility that Senate election results will be disputed and who controls the chamber in 2021 may not be immediately known after the elections.

This could potentially “heighten uncertainty and probably reduce growth,” according to BNP Paribas strategist Olivia Frieser. She noted that interest-rate volatility markets aren’t just pricing in Election Day turbulence. Rather, they seem to be bracing for an “election month.”

Should the outcome of any 2020 races be disputed all the way up to the Supreme Court, as happened in 2000, Ginsburg’s death leaves the court, for now, with eight sitting members and a potential 4-4 tie.

If McConnell can seat a new justice, it’s advantage GOP: the court’s 5-4 decision in 2000 sealed the disputed presidential election for Republican George W. Bush, over Ginburg’s dissent.

©2020 Bloomberg L.P.