Foreign-Local Tug of War Hangs Over Malaysia Debt

Foreign-Local Tug of War Hangs Over Malaysia Debt

(Bloomberg) -- Malaysia’s yield curve is trading near the steepest in almost four years amid wider fiscal deficit concerns. As demand from pension funds is expected to decline in 2021, any shift in the curve will hinge on appetite from global funds amid signs of a vaccine-aided growth recovery.

Malaysia’s bonds are the worst performers this quarter in Southeast Asia after the Philippines, offering a total return of 2.9% to dollar-based investors. The spread between the three- and 10-year Malaysian bonds stands at 82 basis points, near the four-year high of 90 basis points reached in October. While shorter-duration bonds have gained from reductions in benchmark rates, investors have shunned long-maturity bonds amid the expected decade-wide fiscal deficit in 2020 which is targeted at 6.0% of gross domestic product.

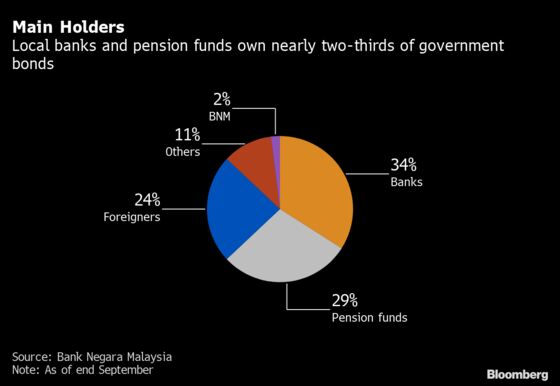

Onshore banks are the largest holders of Malaysian government bonds, holding nearly a third of all outstanding conventional and Islamic sovereign securities as of end-September, according to central bank data. The country’s public pension funds own close to 30% of the sovereign bonds, while global funds hold around a quarter.

Onshore banks

Bond demand from local lenders may dip next year if the central bank allows liquidity-easing measures to lapse. Banking liquidity has been boosted so far by the 100 basis points cut to the statutory reserve requirement, or SRR, in March, as well as the easing of regulations on SRR-compliant assets back in May, allowing banks to use government bonds to meet reserve requirements. The easing measure is set to expire in May 2021.

Pension funds

Appetite from the nation’s pension funds have been stable so far, but a continuation of that into the new year looks less certain in part due to measures that will have an impact on their cash flows. As part of the government’s stimulus efforts, the 2021 budget announced on Nov. 6 allowed more than 8 million Employee Provident Fund (EPF) members to tap their retirement funds, and raised the withdrawal limit to 10,000 ringgit ($2,460). The authorities also reduced members’ contributions to the state pension fund.

“EPF’s demand for Malaysian government bonds is likely to remain weak, and we expect its holdings to modestly decline in 2021,” according to Duncan Tan, a strategist at DBS Group Holdings Ltd. in Singapore. Supply-demand dynamics in the Malaysian bond market could turn slightly unfavorable in 2021, with issuance to remain elevated relative to the pre-Covid historical trend, he added.

Global funds

Malaysia has enjoyed net foreign bond inflows so far this year, while Indonesia and Thailand have suffered net withdrawals. Net foreign inflows has reached $2.7 billion year-to-date, but most of the global flows have so far benefited shorter-maturity bonds as investors positioned ahead of the central bank’s rate cuts. Effective deployment of vaccines coupled with fiscal revenue from higher oil prices could lead to a domestic growth recovery, reigniting interest in long-maturity bonds next year -- especially if the U.S. currency and global rates remain supportive of wider emerging-market assets.

“The silver lining is that the confluence of rising oil prices and vaccine roll out could materially ease pressures on government financing; and if the government is able to manage its borrowing plans -- timing and tenure -- then Malaysian bond markets could avert worsening pressures being feared,” said Vishnu Varathan, head of economics and strategy at Mizuho Bank Ltd. in Singapore.

While the budget shortfall is expected to narrow to 5.4% of GDP in 2021, helping alleviate concerns of an oversupply, demand from foreign investors will also play a major role in supporting a flatter sovereign curve next year.

What to Watch

- The Philippines balance-of-payment figures will be out next week

- Malaysia will release November inflation data on Wednesday, with the nation having experienced deflation since March

- Thailand will publish custom trade data on Wednesday, with the central bank deciding on the key rate on the same day

Note: Marcus Wong is an EM macro strategist who writes for Bloomberg. The observations he makes are his own and not intended as investment advice.

©2020 Bloomberg L.P.