Where Ford and Jaguar Lead, the Rest Will Surely Follow

(Bloomberg Opinion) -- With Ford Motor Co. warning of thousands of European job cuts on Thursday, and Jaguar Land Rover expected to do similar, you’d be forgiven for thinking the global economy is mired in recession. (It isn’t).

While auto sales have deteriorated sharply in the once-lucrative Chinese market, the chief reason for sagging sales in Europe has been production troubles caused by new emissions tests. Indeed, until recently European carmakers were reporting very decent levels of profitability in the region as consumers there gorged on cheap credit.

Economic activity has slowed recently in the euro zone, and Brexit could make things a whole lot worse, but anticipated GDP growth of about 1.6 percent this year is hardly a disaster for the currency union. So what gives? Business historians may look back on this period as the moment that carmakers finally got real about the epochal challenges for their industry.

The remarkably rapid shift from diesel to petrol and from saloons (sedans to my U.S. readers) to SUVs; the burden of investing in electric and autonomous technology; not to mention local trade tensions and currency swings (thanks Brexiters!). These are all forcing carmakers to make hard decisions to preserve cash.

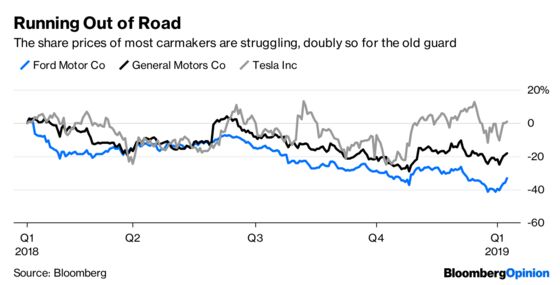

The auto industry has arguably been too slow to face this reality. General Motors Co. tolerated losses in Europe for more than a decade before finally admitting defeat in 2017. Ford has been even more leaden-footed, unwisely letting its European workforce creep higher since since 2012.

Some hesitancy is understandable, though. Ford would be foolish to abandon its successful commercial vehicles franchise, for example. Plus, anyone who’s tried to lay off workers or close a car plant in Europe knows it’s not a decision to take lightly. Politicians and unions often make life miserable for executives, and with good cause. When car plants close, that means the loss of well-paid, skilled jobs – often never to return.

Indeed, the sad truth is that today’s staff cuts are probably just the start for the industry. At some point over the next decade, automakers will have to dramatically slim down their workforces to reflect the fact that electric cars are much less complicated to make and that battery production will be outsourced (possibly to Asia).

Analysts at Credit Suisse say the industry may need 18 per cent fewer workers, while Germany’s Ifo institute, an economic research body, has warned that more than 600,000 German are at risk because of the demise of the combustion engine. Some jobs will be lost via retirement and natural attrition, and automakers will doubtless do their best to find something else for displaced workers. But with car-sharing and ride-hailing on the increase, it’s hard to characterize building vehicles as a growth industry anymore.

Of course, it’s still possible to make money selling cars, as Ferrari’s galloping share price has underscored. Ford lacks the premium brands that generate higher margins because it sold a bunch of them a decade ago, including Jaguar and Land Rover.

But in view of all these headwinds, it’s incredible that Britain is recklessly making things even more difficult for the industry by trying to crash out of an enormously beneficial single market and customs union and forcing automakers to develop costly contingency plans – both in the U.K. and elsewhere. Technological change is a reasonable cause of job losses, political self-harm is not.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Bryant is a Bloomberg Opinion columnist covering industrial companies. He previously worked for the Financial Times.

©2019 Bloomberg L.P.